European equities in Middle East turmoil

European equities have fallen significantly since our last Equity Committee held on 10 February, due to the start of the Middle East conflict on 28 February, which completely wiped out the gains recorded since the beginning of the year. So far, European equities have suffered more as a result of this crisis than those in the US, as Europe is one of the world’s largest energy importers.

European equities have fallen significantly since our last Equity Committee held on 10 February, due to the start of the Middle East conflict on 28 February, which completely wiped out the gains recorded since the beginning of the year. So far, European equities have suffered more as a result of this crisis than those in the US, as Europe is one of the world’s largest energy importers.

Cyclicals are the hardest hit

Since the last Committee, cyclical sectors have been particularly hard hit as the market has shifted into risk-off mode. The conflict has evolved into a direct shock to global energy infrastructure, causing oil prices to surge, which could lead to slower global growth and higher long-term interest rates. The sectors most affected have been Consumer Discretionary, Financials and Materials, while Industrials and Real Estate have shown greater resilience, although they remain in negative territory.

Conversely, defensive sectors have held up, particularly Energy, which was unsurprisingly the best performing sector (with stocks such as Shell and BP benefiting from higher oil prices), and Utilities, which was slightly positive during the period. However, Healthcare and Consumer Staples were less resilient than expected, which can be explained by specific headwinds for certain stocks that weighed on the performance of these sectors. Thus, Healthcare was penalised by Novo Nordisk, which was one of the worst contributors due to poor clinical results.

Communications was the second best performing sector, benefiting from favourable M&A prospects for the telecom segment in some countries. Lastly, IT recorded a slightly negative performance while outperforming the broader market.

Lower earnings expectations and valuation multiples

Given the current geopolitical crisis, European EPS growth expected for 2026 has been revised downwards, from +11.7% before to +10.6%[1]. Consumer Discretionary remains the sector with the highest expected growth (+67% thanks to favourable base effects), followed by Materials (+23%), IT (+14%) and Communication Services (+13%). The Energy sector is expected to see stable EPS growth in 2026 (which will likely be revised upwards), while Real Estate is the only sector for which earnings growth forecasts are negative[2].

Since the last Equity Committee, European valuation multiples have declined, with the 12-month forward P/E ratio now standing at 14.9x (down from 15.6x previously). IT and Industrials remain the most expensive sectors (27.1x and 21.2x respectively), while Financials and Energy are the cheapest (9.9x and 12.7x respectively). However, the Energy sector multiple has increased significantly, as it stood at 9.9x four weeks ago[3].

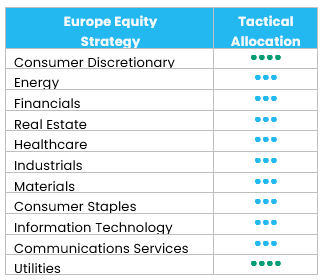

No change in sector grades

We maintain our sector grades.

At level 1, we keep our positive grade (+1) on:

- Consumer Discretionary, as luxury goods (50% of the sector) should benefit from stabilising revenue growth and a favourable outlook for 2026, while we are more cautious on automobiles (European OEMs under pressure due to Chinese competition).

- Utilities, given strong growth drivers (electrification and grid connections) and reasonable valuations.

We maintain our neutral stance on the other sectors, i.e. Energy (as current valuations are not attractive, following the recent re-rating), Materials (base chemicals cheap but still trending downwards; more positive trends in metals & mining), Industrials (structural growth in defence and electricals, but tight valuations), Consumer Staples (subdued volume growth), Healthcare (interesting valuations but prices impacted by tariffs), Financials (good visibility on 2026 EPS growth but consensual long), IT (positive trend for semiconductors but tight valuations, especially for equipment providers; more interesting valuations for software but AI disruption risks), Communication Services and Real Estate.

US equities: increased volatility

US equities have faced increased volatility over the past few weeks, with resilient economic data being weighed against rising geopolitical tensions, particularly in the Middle East. Energy price fluctuations and shifting policy expectations added to short-term market swings. Despite this, economic growth remains solid, and the Federal Reserve’s steady policy stance continues to anchor expectations. Overall, the broader market tone remains constructive, supported by resilient corporate fundamentals.

Geopolitical uncertainty sparks sector and style rotation

Oil prices rose sharply amid escalating tensions in the Middle East, adding some pressure to inflation expectations. At the same time, US policy signals remained unclear, increasing geopolitical uncertainty. Labour market data showed some moderation, pointing to a gradual normalisation in growth dynamics. In this environment of higher energy prices and mixed macro signals, investors adjusted positioning more selectively across sectors and styles.

US equities held up quite well, but recent performance highlighted a clear rotation beneath the surface of the broader market. Large caps were relatively resilient, while small caps experienced more pronounced weakness, reflecting greater sensitivity to macroeconomic uncertainty. From a style perspective, growth outperformed value. Similarly, cyclicals clearly underperformed, whereas defensives outperformed.

Sector performance was similarly differentiated. Among cyclicals, Industrials showed relative resilience, while Financials and Materials lagged. Within defensives, Utilities and Energy stood out with positive performances, supported by geopolitical developments. Consumer Staples and Healthcare also outperformed the broader market. Communication Services and Information Technology held up quite well, performing broadly in line with the wider market. Within Information Technology, hardware and semiconductors proved stable, while software remained under pressure.

Overall, the recent rotation reflects the markets’ recalibration to a more complex macroeconomic backdrop. As growth remains resilient and inflation and geopolitical risks re-emerge, investors are shifting towards sectors and styles with stronger earnings visibility and more defensive characteristics.

Strong earnings season

As the earnings season draws to a close, the overall picture remains constructive. About 73% of S&P 500 companies exceeded earnings estimates, underscoring the resilience of corporate profitability. The S&P 500 delivered 14% year-on-year earnings growth, marking another quarter of solid expansion. Information Technology led the way, with earnings growth of roughly 33%, reinforcing its central role in driving overall profit momentum, according to FactSet[4].

Building on these fourth-quarter results, forward expectations remain supportive. 12-month forward earnings growth stands at 15.8%[5], underpinned by resilient revisions and continued strength in Information Technology, alongside meaningful contributions from Financials and Communication Services. Profit growth therefore remains a key pillar of the current market environment.

US equities are trading at around 21 times 12-month forward earnings[6]. While this is above long-term averages, it remains justified by solid earnings momentum. Importantly, the recent moderation in the P/E multiple reflects macro-driven volatility and heightened geopolitical uncertainty, rather than deterioration in underlying earnings fundamentals.

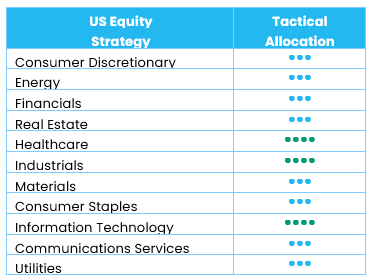

No changes in sector allocation

We maintain our current sector positioning and remain confident in our core convictions: Industrials, Healthcare and Information Technology.

- Industrials continue to benefit from reshoring dynamics, infrastructure spending and ongoing automation trends, with a clear preference for capital goods.

- Healthcare is supported by improved policy visibility, innovation-driven growth and attractive relative valuations, particularly within pharmaceuticals and biotechnology.

- In Information Technology, structural demand remains robust, especially in hardware and semiconductors linked to AI infrastructure and digital transformation.

Despite heightened geopolitical uncertainty and increased market dispersion, we see no need to adjust our overall positioning at this stage.

Emerging equities: outperforming developed markets

Emerging markets equities extended their advance in February, delivering another month of decisive outperformance against developed markets. Year-to-date, emerging equities have made the strongest start to a year since 2012 and underscored the breadth and momentum of the rally. Macro crosscurrents remained present. The US Supreme Court’s decision to strike down tariffs reintroduced uncertainty around the US tariff trajectory and unsettled previously negotiated trade arrangements.

Performance was once again led by technology. The dominant driver remained the AI-driven memory upcycle, increasingly perceived as a multi-year structural theme rather than a short-lived rebound, propelling semiconductor and hardware names across North Asia. Korea stood at the epicentre of this surge, supported not only by robust earnings revisions in technology but also by renewed optimism around corporate governance reform. Taiwan similarly benefited from resilient AI-related demand and strong export dynamics, reinforcing the region’s leverage to the global capex cycle.

Outlook and drivers

Emerging market macro remains constructive, supported by easing cycles, stable inflation and renewed inflows, creating a favourable environment that positions emerging equities for continued outperformance versus developed markets. Meanwhile, in the US, the Supreme Court’s decision curtails the scope for Trump’s emergency tariffs, introducing greater procedural discipline to US trade actions. While protectionist pressures persist, the ruling reduces policy uncertainty, supporting a constructive view on regional risk sentiment in emerging markets. Iran tensions have significantly increased volatility in the near term. There remains a wide range of possible outcomes. If oil prices remain high for longer, pressure would likely fall more heavily on select large net importers. On the other hand, some emerging markets, such as Brazil, could see relative support if commodity prices stay firm. A key swing factor for emerging equities could be the US dollar. At this stage, the underlying backdrop for emerging markets remains reasonably constructive, but we would frame this as a developing risk event rather than something to dismiss outright.

After an outsized, semiconductor-led run-up, Korea has become increasingly susceptible to headline risk, as crowded positioning amplifies even minor geopolitical developments into disproportionate de-risking episodes. While AI-driven demand for advanced memory and high-bandwidth chips continues to provide a robust structural underpinning, a prolonged conflict in Iran could trigger a reassessment of both energy costs and supply-chain resilience. Such a scenario could reprice risk premia across export-oriented sectors.

In the meantime, geopolitical tension highlights the importance of secure, scalable commodity supply, an environment that plays to South America’s strengths. The region’s abundant metals and oil reserves offer both hedge appeal and operating. With improving macro conditions in the region, South America is expected to benefit from both commodity and energy tailwinds.

Positioning update

We have reduced overall risk in a disciplined way, taking profits where positioning and technicals have become stretched, while keeping medium- and long-term convictions intact. The recent escalation in the Middle East has increased volatility and we continue to monitor its advance. Any potential signs of de-escalation emerging can serve as tactical opportunities once entry points and risk premia improve.

As a result, we downgraded Asia from overweight to neutral; within the region, we downgraded Korea and Taiwan from overweight to neutral among countries. We upgraded ASEAN (sub-region within Asia), a laggard region year-to-date and in the last 12 months.

As for sectors, we downgraded IT from overweight to neutral; within the sector, we downgraded semiconductors & equipment (sub-sector) and technology hardware & equipment (sub-sector) from overweight to neutral, and upgraded software & services (sub-sector) on the back of the previous large-scale sell-off. We upgraded consumer services (sub-sector) and retailing (sub-sector) within Consumer Discretionary from neutral to overweight. We upgraded media & entertainment (sub-sector) within Communication Services from neutral to overweight. Both upgrades are due to the positive news and potentially further recovery in consumption in China. We upgraded Utilities from underweight to neutral, as a defensive sector.

Regions

Asia: downgraded from overweight to neutral

We moved Asia to neutral primarily to reduce concentration in a region where performance has been heavily driven by a narrow set of high-beta technology exposures. In the current environment, geopolitical headlines and oil-driven inflation risks can quickly shift market regimes, making crowded risk-on positions more vulnerable to sharp mean reversion. Moving to neutral improves balance and resilience while preserving flexibility to re-engage if volatility subsides and the macro backdrop stabilises. An upgrade back to overweight would be warranted if de-escalation in the Middle East proves durable, oil tensions ease and risk appetite broadens—conditions that typically compress volatility and re-support Asia’s cyclical and technology-heavy leadership.

Korea: downgraded from overweight to neutral

Korea was tactically downgraded after an impressive run that left the market overbought, with price action outpacing near-term fundamentals and raising the probability of a technical pullback. This is a profit-taking decision rather than a negative fundamental call. Structural competitiveness and earnings momentum may remain supportive, but the market has become stretched and therefore more sensitive to headline volatilities. We would consider upgrading Korea again once technical conditions normalise, especially if de-escalation reduces the geopolitical risk premium and supports a rotation back into global cyclicality.

Taiwan: downgraded from overweight to neutral

We neutralised Taiwan to address its outsized concentration in Technology, which makes it highly effective in risk-on phases but disproportionately sensitive during risk-off drawdowns. With the local market’s performance tightly linked to the global semiconductor and hardware complex, the combination of elevated valuations, crowded positioning and higher headline risk argues for a more balanced stance. A re-upgrade would be justified if the correction resets expectations and improves forward return potential, with reduced geopolitical uncertainty.

ASEAN: upgraded from underweight to neutral

We neutralise the rating for ASEAN. It has been a clear laggard both year-to-date and in the last 12 months.

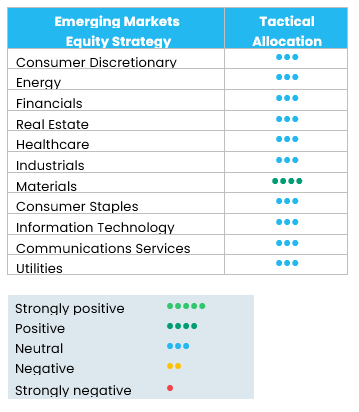

Sectors

Technology: downgraded from overweight to neutral

We downgraded Technology to neutral to reduce exposure to a sector that had become a core beta driver and, in part, a crowded trade. Fundamentals remain strong, but when valuations and positioning are extended, the sector becomes more sensitive to sudden shifts in discount rates, risk appetite and geopolitical shocks. Returning Technology to overweight would require a clearer macro path where easing geopolitical risks and oil-related inflation concerns support a lower volatility regime and more stable rate expectations. As a result, we downgraded semiconductors & equipment (sub-sector) and technology hardware & equipment (sub-sector) from overweight to neutral. In contrast, we upgraded software & services (sub-sector) to neutral because the sell-off has gone too far in the short term, creating a more balanced risk-reward profile.

Consumer Discretionary: upgrade of consumer services and retailing from neutral to overweight

Consumer services in China have been out of favour for an extended period, leaving sentiment and ownership unusually depressed. The earnings beat of JD.com is meaningful: it not only supports company-specific positive revisions but also provides a constructive read-across to the broader China retail complex. With positioning still light, even incremental positive news can generate outsized upside. Alibaba’s upcoming results are an important indicator to monitor. Equally, for retailing in China, constituents such as Meituan and Trip.com stand to benefit from potential stabilisation in China consumption expectations once earnings begin to confirm that the trough narrative is behind us.

Communication Services: upgrade of media & entertainment from neutral to overweight

The upgrade is triggered by the same “oversold/under-owned” opportunity set within China’s large-cap technology and internet ecosystem. The space has absorbed substantial de-risking over recent months. Much of the negativity is reflected in price and positioning. With Tencent’s results set to be released in the coming weeks, the risk-reward profile is increasingly attractive, particularly if earnings and guidance validate improving operating trends and reinforce the case for a re-rating from depressed levels.

Utilities: upgraded from underweight to neutral

We neutralise Utilities as a deliberate step to improve portfolio defensiveness.

[1] Sources: Refinitiv, Bloomberg©, as of 6 March 2026

[2] Sources: Refinitiv, Bloomberg©, as of 6 March 2026

[3] Sources: Refinitiv, Bloomberg©, as of 6 March 2026

[4] Source: FactSet as of 6 March 2026

[5] Sources: Refinitiv, Bloomberg©, as of 6 March 2026

[6] Source: FactSet as of 6 March 2026