Last week in a nutshell

- In the euro zone, bond and equity markets welcomed both the weaker-than-expected preliminary inflation data for December.

- In China, the composite PMI rose – for the first time since June – to 48.3 in December from 47.0 in the previous month.

- The US economy added 223K new jobs in December, the unemployment rate fell to 3.5% and hourly earnings fell to 4.6% YoY.

- The latest FOMC minutes focused on the need to retain flexibility and optionality, emphasising the central banks’ resolve to achieve its price-stability goal.

What’s next?

- Both the US CPI and the real estate market index will help assess the next US Federal Reserve Bank’s move. While there is a growing strain on home affordability keeping prospective homebuyers out of the market, consumer price inflation has yet to converge towards the Fed’s expectations.

- Central banks will be in the spotlight as we begin the week with the Riksbank's International Symposium on Central Bank Independence. Topics on the agenda include climate, payments, mandates and global policy coordination. The ECB's economic bulletin will also be published.

- China is open again to tourists with a negative COVID-19 test. Mandatory quarantine and daily flights limits are removed. The country will also release data on new loans and the economic activity, including the balance of trade.

- The University of Michigan will release January estimates of survey data on US Consumer Sentiment and Inflation Expectations, a first glance at how consumers view prospects for their own financial situation and the general economy at the start of the year.

Investment convictions

Core scenario

- Our current economic scenario encompasses a deceleration in inflation and economic growth but without a severe recession and we do not expect to see a lower market low than the one seen last October.

- We see equity markets moving within a fairly broad range: limited to the upside by the actions of central banks, which will ensure that financial conditions do not ease too quickly if the economy is holding up well and supported by a faster monetary policy pivot if the economy is too hard hit. Hence, we have a constructive positioning - i.e., overweight equities - but with a controlled risk budget.

- We expect emerging market and US assets to outperform as valuation has become more attractive while Asia keeps superior long-term growth prospects vs. developed markets.

- Regarding bonds, the carry that was reconstituted by the rise in yields in 2022 seems attractive for us. The deceleration in inflation should lead to a drop in volatility on bonds, allowing for an easing of volatility on other asset classes.

- Central banks are slowing the pace in monetary tightening, aiming for a final target rate to be reached in 2023. As inflation expectations continue to decline and bottlenecks are easing, the focus is shifting towards growth while maintaining financial stability.

- In this environment, we expect the positive correlation between equities and bonds to decline and Alternative investments to perform well.

Risks

- Among the upside risks, we note that the Chinese re-opening in 2023 would be a substantial support for the global economy.

- Further, unseasonably warm temperatures have recently pushed natural gas prices lower, mitigating the negative impact of the energy crisis.

- Overall, inflation declines and a rise in growth at some point in 2023 is limiting the market downside. But we know that the central banks anti-inflation stance is also capping the upside potential for risky assets.

- Downside risks would be a monetary policy error via over-tightening in the US or in the euro zone.

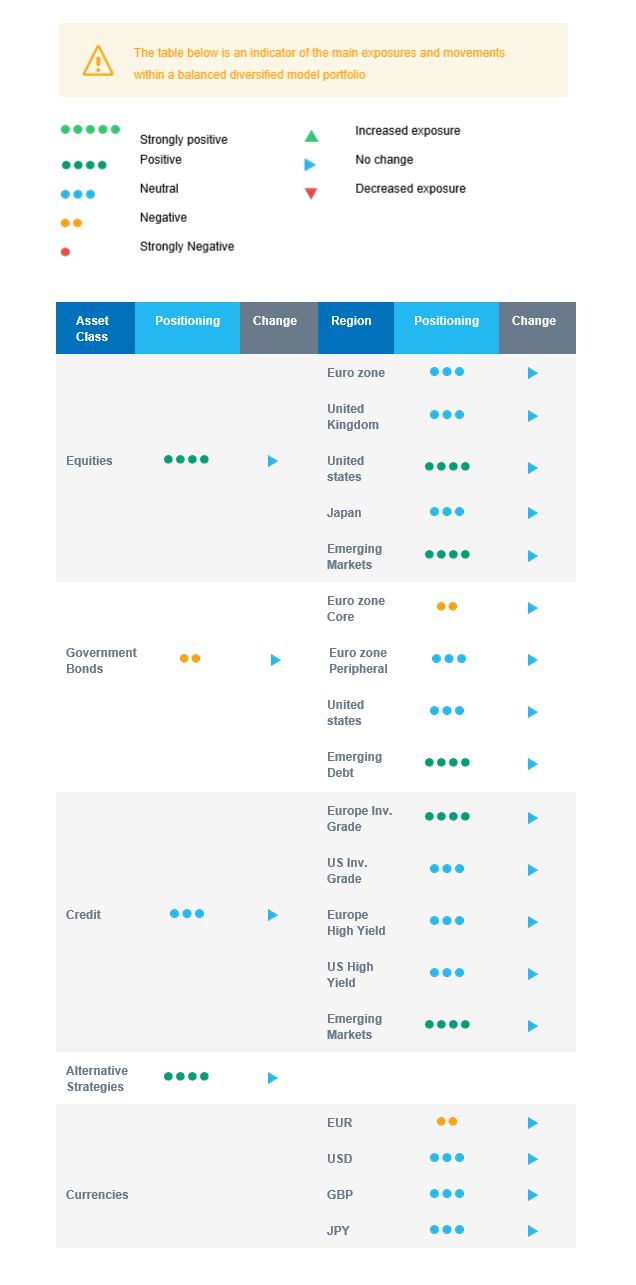

Cross asset strategy

- Our multi-asset strategy has remained constructive and overweight equities on attractive price levels since October. It is nimble and can be adapted quickly. We sold some USD vs EUR and took partial profit on our US equity exposure. We currently have few strong regional convictions:

- Neutral euro zone equities.

- Neutral UK equities, resilient sector composition and global exposure.

- Overweight US equities, as our soft-landing scenario is unfolding.

- Overweight Emerging markets, as valuation has become attractive and there is room for a catch-up vs. developed markets.

- Neutral Japanese equities, as accommodative central bank, and cyclical sector exposure usually act as opposite forces for investor attractiveness.

- Positive on sectors, such as healthcare, consumer staples and the less cyclical segments of the technology sector.

- Positive on some commodities, including gold.

- In the fixed income universe, we have a slight short duration positioning via core Europe.

- We continue to diversify into European investment grade credit and source the carry via emerging debt and global high yield debt.

- In our long-term thematics and trends allocation: We favour investment themes linked to the energy transition and keep Health Care, Tech and Innovation in our long-term convictions.

- In our currency strategy, we diversify outside the euro zone and are long CAD.

Our Positioning

Our current positioning is overweight equities with a preference for Emerging markets and the US. On the fixed income side, we keep a slight short portfolio duration via EU core bonds. We have a constructive view on credit, including high yield. The latter looks attractive with a sufficient buffer for defaults. We remain allocated to commodity currencies via the CAD.