During the month of October, the market wobbled between hope and fear. The first half of the month saw markets – supported by global PMIs moving further into expansion territory and positive consumer confidence – continue their journey upwards. This bullish momentum reversed during the second part of the month with the rapid rise of COVID-19 infections in Europe and the negative impact that new lockdown measures could have in an already-fragile economic situation.

During the month of October, the market wobbled between hope and fear. The first half of the month saw markets – supported by global PMIs moving further into expansion territory and positive consumer confidence – continue their journey upwards. This bullish momentum reversed during the second part of the month with the rapid rise of COVID-19 infections in Europe and the negative impact that new lockdown measures could have in an already-fragile economic situation.

Most equity markets were down for the month. European equity indices declined the most, due to newly announced social distancing measures to contain the virus spread. The Dax and the Euro Stoxx 50 declined by -9.44% and -7.37% respectively. Other major European and US equity indices declined between -2% and -5%. Asia outperformed, with equity indices from India, Hong Kong and China returning positive low single digits. At sector level, US utilities outperformed, with the election of pro-renewables Joe Biden seeming to gain more traction.

Sovereign and corporate debt yields remained stable during the period. Interesting to note, however, that Argentinian sovereign bonds declined 25% shortly after the restructuring.

The HFRX Global Hedge Fund EUR declined -0.26% during the month.

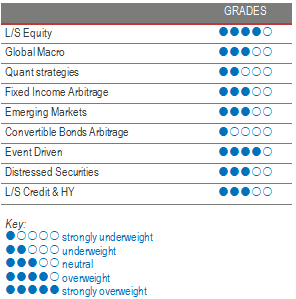

Long Short Equity

Long Short Equity funds had a good month relative to long-only indices. As markets reversed during the second part of the month, hedge funds, which, on average, followed the move, captured only 30% of the downside. Alpha generation – led by North America- and Asia-focused strategies’ long books – remains strong. Technology and Communication Services have been the biggest contributors to returns. Looking back, going into the US election, LS Equity strategies tended to add risk. This year’s behaviour was different, since managers started the pre-election period with gross and net exposures at decade-high levels. Considering the strategy’s on-average good performances and already high-risk exposure, funds would not be expected to take on much more risk until the end of the year. For the last 3 months, there has been some kind of rotation from the Technology, Communication Services and Consumer Discretionary sectors into cyclicals, with managers partially trimming their winning investment and positioning their portfolio for the recovery phase. As we write, Value and cyclicals have had an incredible rally, following positive news on the vaccine being developed by Pfizer and BioNTech. Although diversification has, this year, not paid as well as full investment in technology or Growth thematics, LS Equity as a strategy is very rich and diverse in terms of styles, and possesses several tools to face varied market environments.

Global Macro

On average, Global Macro strategies did not do well during the month. Among the macro indices, the Macro Commodity index was the only one to finish the month on positive ground. Although discretionary strategies lost money this month, they continue to outperform Systematic Macro. Long investments in sovereign or quasi-sovereign fixed income in Argentina and Puerto Rico, receiving front-end rates in Brazil, and long EM currencies versus the US dollar, were among the month’s biggest negative drivers. Nonetheless, this year offered many opportunities across the globe, making it one of the best years in terms of performance since the last financial crisis. Several high-conviction managers are posting double-digit returns year-to-date. In this sentiment-driven environment, we tend to favour discretionary opportunistic fund managers who can draw on their analytical skills and experience to generate profits from selective opportunities worldwide. The stabilisation of the market and increased visibility in macro-economic data should lead to better performances from systematic strategies with expected lower realized volatility levels than those posted by the more concentrated discretionary managers.

Quant strategies

Performances were not very good during the period. Trend-followers tended to lose money on long positions in equities and US treasuries. Yields for the back end of the US curve increased by around 20bps. Nor did Systematic Equity Market Neutral Strategies do very well, due to sector and style rotations, going into the US elections. Some Multi-Strategy Quantitative Strategies were able to print better performance results thanks to a more diverse array of models. 2020 has not been a good vintage for quants. Throughout the year, models have had difficulties dealing with the violent and rapid increase in market volatility and asset correlations.

Fixed Income Arbitrage

Fixed Income Relative Value having had one of its most spectacular months in history in March 2020 has highlighted the need to be invested in managers with strong set-ups (secured-term repo lines with high-quality counterparts and longstanding relationships). At the end of March, our managers took advantage of the dislocation within the US basis to post historical positive returns from what has been a once-in-a-decade opportunity. Like other RV trades, if spreads have been wider than they were pre-crisis up to July, they are now slowly reverting to their lows on the back of ongoing central bank rhetoric, poor GDP numbers and very low realized volatility. However, potential inflation scares or stronger US growth could trigger change without notice. As such, we are reviewing potential candidates that could benefit from such an environment.

Emerging markets

The opportunity set in Emerging Markets Fixed Income is characterized by an attractive yield, since, despite a strong summer in terms of performance, the asset class has substantially underperformed Developed Markets since the start of the crisis. It is also a highly idiosyncratic investing ground, since, on top of the macro-economic situation of each country, the political situation within each region is very different, leading to a wide set of long and short opportunities. The macro outlook remains extremely foggy for Emerging Markets, however, with Fundamental managers stressing that, in a zero-rate world, Emerging Markets is the only alternative to invest in yielding fixed income. The high sovereign issuance during this year (+40% relative to 2019) has been well received. Considering the fragility of fundamentals, managers usually adopt a very selective approach. Trades are mainly implemented by investments in fixed income, credit and currencies, where the fear-led pricing of risk is creating massive dislocations and opportunities by ignoring the fundamentals specific to each region. Nonetheless, caution is required, due to the higher sensitivity of the asset class to investor flows and liquidity.

Risk arbitrage – Event-driven

The strategy performed well during the month of October. Some important pre-March deals like the acquisition of Tiffany’s by LVMH made money. To be able to close the deal, Tiffany’s board agreed to grant a small discount on the acquisition price. Managers tended to add to this deal after it was cleared by the EU Commission. Merger deals picked up more significantly during the 3rd quarter of the year. Some managers think the pace might remain quite high over the following months because a Biden Administration might lead to tougher regulatory scrutiny or a different tax regulation. Nonetheless, this scenario is not yet reflected in deal spreads. Also interesting to note is that current trends in merger activity are not specifically linked to a particular administration. The industry is expecting an important deal flow from the Healthcare and Telecom sector consolidation and from the Energy sector restructuring. That said, in terms of performance, merger deals are not the best performance contributors of the year for Event-Driven strategies but rather capital market transactions initiated after March. Soft catalysts and credit books tend to be the best p&l generators in multi-strategy funds. As we progress towards a healthcare solution to this crisis, Event-Driven will have many opportunities to deploy capital, as corporations adapt and restructure to the new reality.

Distressed

During the year, the opportunity set in Distressed has had more dealings with distressed sellers than with distressed assets. Complex and less liquid instruments sold off and are yet to recover pre-crisis levels. Some distressed managers have focused on snapping quality assets like Legacy RMBS from levered investors who needed liquidity at any cost. This beta trade has largely played out. High-yield spreads are stable but corporate defaults are rising. During the month of October, Mallinckrodt, CBL Properties and Pacific Drilling were among the largest defaults. The opportunity-set is widening and getting bigger by the day but it is going to be a tough battle as corporations are trying to pile on further debt to navigate the crisis, opening up battle lines with existing creditors for current collateral. We favour experienced and diversified strategies to avoid having to face extreme volatility swings. It is not going to be easy but this is the environment and opportunity-set these managers have been waiting for this past decade.

Long short credit & High yield

Credit spreads for Investment-Grade and High-Yield markets reached extreme levels unseen since the crisis of 2008. The market was also highly affected by the lack of liquidity, prompting the ECB and the Fed to step up their IG debt-purchasing programmes. The Fed also decided to include High Yield in its buying programmes to smooth the high amount of Investment-Grade fallen angels downgraded to High Yield. Rating agencies forecasted that the amount of fallen-angel debt could reach $700 billion in the US, probably too big to be absorbed by the HY market smoothly. Investment Grade and short-term High-Yield issue spreads reacted very quickly to liquidity injections, especially in the US. According to the managers we track, while this move in higher-quality issues was widely expected, there are still many opportunities in High Yield but also in the cross-asset relative value trades (long bond vs short equity) and intra-asset RV trades (long bonds and long protection) generated by the market dislocations. Contrary to 4Q 2018, opportunities offered in credit will take longer to be arbitraged, leaving time for investors to review their allocations.