Europe’s strategic autonomy: emerging reality or political mirage?

Why Europe’s autonomy agenda is becoming a powerful catalyst for new investment cycles and sector-level opportunities.

Europe is confronted with significant change. After five decades of steady globalisation and open trade, global integration is slowing — and in some areas, reversing. In 2024, former ECB chief Mario Draghi underscored the urgent need to strengthen Europe’s economic competitiveness, setting out more than 300 recommendations across key industries. The report[1] highlighted three central priorities: closing the innovation gap to reignite growth and address declining productivity amid demographic shifts; reducing strategic dependencies; and safeguarding the interests and well-being of European citizens.

In response, European strategic autonomy has emerged as a defining priority, with Europe seeking greater independence in policy, security and economic decision-making.

Strategic autonomy underpins Europe’s ability to protect its interests in an increasingly uncertain world. Geopolitical tension, technological disruption and economic interdependence have exposed vulnerabilities — from energy dependence and fragmented defence capabilities to reliance on foreign technology and critical raw materials. At its core, it is Europe’s capacity to act independently in defence, foreign policy, the economy and technology, without undue reliance on external powers.

China’s growing assertiveness, the unpredictability of U.S. foreign policy, and the Russia–Ukraine war have underscored the urgency of a more self-reliant Europe. These developments have laid bare how dependent the EU still is on NATO and the United States for its defence and security.

The EU’s heavy reliance on Russian gas[2] emerged as a key vulnerability following the outbreak of the Russia–Ukraine conflict. This shock has highlighted the strategic necessity of greater control over Europe’s energy production and distribution — accelerating the shift toward renewables, diversified imports, a more resilient grid and the reconsideration of nuclear energy within a balanced energy mix.

Europe continues to trail the United States and China in critical technologies such as semiconductors, artificial intelligence, and cloud computing, creating economic and security risks. Achieving strategic autonomy requires Europe to secure its digital infrastructure, safeguard data, and maintain control over their essential technological capabilities. Rapid technological change is simultaneously creating new opportunities and new dependencies, exposing structural vulnerabilities across defence, energy, technology and supply chains.

The COVID-19 pandemic exposed the fragility of global supply chains, especially in pharmaceuticals, medical equipment, and semiconductors. Between 60% and 80% of active pharmaceutical ingredients are produced outside the EU[3], while roughly 60% of Europe’s energy[4] and most critical raw materials — such as rare earths and permanent magnets — are imported. Repatriating or diversifying production and sourcing is now seen as vital to Europe’s long-term resilience and strategic autonomy.

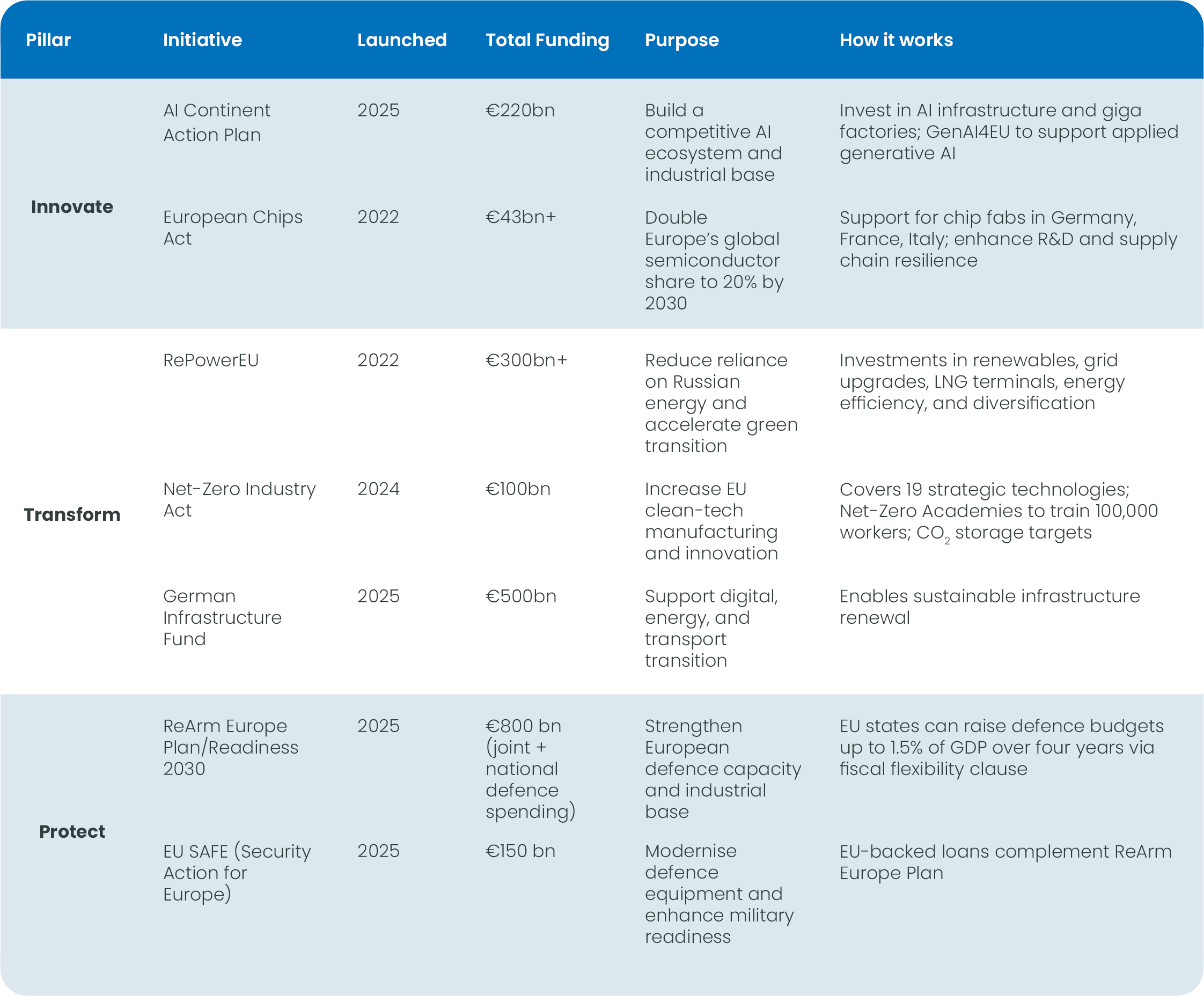

Europe’s “awakening” triggered a wave of strategic initiatives and policy actions to foster and finance the continent’s strategic autonomy whilst preserving its core values. Progress remains uneven: sectors such as transport, energy grid, critical raw materials and defence are moving ahead driven by political urgency.

While the Draghi report estimates that Europe will require an additional EUR 750-800 bn in annual investment[5] (around 4.5% of 2023 EU GDP) from both the public and private sectors, several ambitious proposals have already been launched, signalling a shift from a market-driven approach to a more strategic industrial policy:

Source: European Union: ReArm Europe Plan/Readiness 2030

The scale of required investments across sectors is large, pointing to the importance of both public and private funding, and is already starting to create clear opportunities for investors. European equities remain reasonably priced versus many of their US counterparts. They also offer a broad mix of sectors, many of which stand to benefit from long-term policy support in areas like energy, defence and technology.

We have already seen strong gains in companies linked to Germany and in aerospace and defence. At current prices these stocks are no longer cheap, but these sectors are still not widely held by investors. Combined with solid growth in sales and earnings, this makes defence a theme that may be hard to ignore in the coming years.

Looking ahead, these trends may favour more cyclical and domestic European companies, and those that give access to key technologies:

By focusing on Europe’s emerging strategic themes, investors can position their portfolios for a transformation that may shape the region’s next growth cycle.

Obtenga información más rápidamente con un solo clic