Last week in a nutshell

- The downturn in euro zone business activity accelerated as the Composite Purchasing Managers' Index (PMI) indicated the bloc entered the last quarter of the year on the back foot.

- Data stemming from US initial and continuing jobless claims confirmed the Federal Reserve statement that US labour market conditions are going through softening, but remain at historically tight levels.

- Further in the US, consumer sentiment cooled again as credit concerns seem unlikely to abate anytime soon.

- China’s consumer and producer price indexes declined by 0.2% and 2.6% YoY in October as deflationary pressures in the world’s second largest economy persist.

What’s next?

- US inflation will be in the spotlight with the publication of key figures, such as core inflation rate, CPI and PPI.

- Industrial production and trade balance releases for several countries, including the US and China, will shed some light on which sectors have been the most sensitive to rising interest rates and falling demand.

- Preliminary GDP growth rates of key regions and countries, including the euro zone, will be released as investors try to gauge the ongoing regional diverging trends.

- On the geopolitical front, US President Joe Biden will meet his Chinese counterpart, Xi Jinping, at the APEC Summit in San Francisco for the first conversation between the two leaders in a year.

Investment convictions

Core scenario

- The desynchronisation growth continues. The US economy is on a softening trend as well as inflation, backing the last Federal Reserve bank’s decision to pause monetary tightening and keep interest rate high for long.

- In Europe, growth is likely to remain lacklustre for most of next year, while disinflation accelerates.

- In China, economic activity and the evolution of prices have shown some timid signs of stabilisation.

- The perception of a softer bias from developed countries’ central banks has finally led to a downward repricing in bond yields. Meanwhile, China’s likelihood to export deflation to the world is fading only slowly.

- The increase in real rates has been a headwind for equity valuations during Q3 and last month while the deceleration of economic growth will weigh on profits.

Risks

- A renewed temporary overshoot in longer-dated bond yields would present a risk for fixed income holdings and duration-sensitive equities.

- The steepest monetary tightening of the past four decades has led to significant tightening in financial conditions. Financial stability risks could return.

- US inflation needs a credible Federal Reserve as inflation breakeven anticipations have not decreased yet while the European Central Bank must be mindful of the peripheral countries.

- Risks to the outlook for global growth remain tilted to the downside as geopolitical developments unfold.

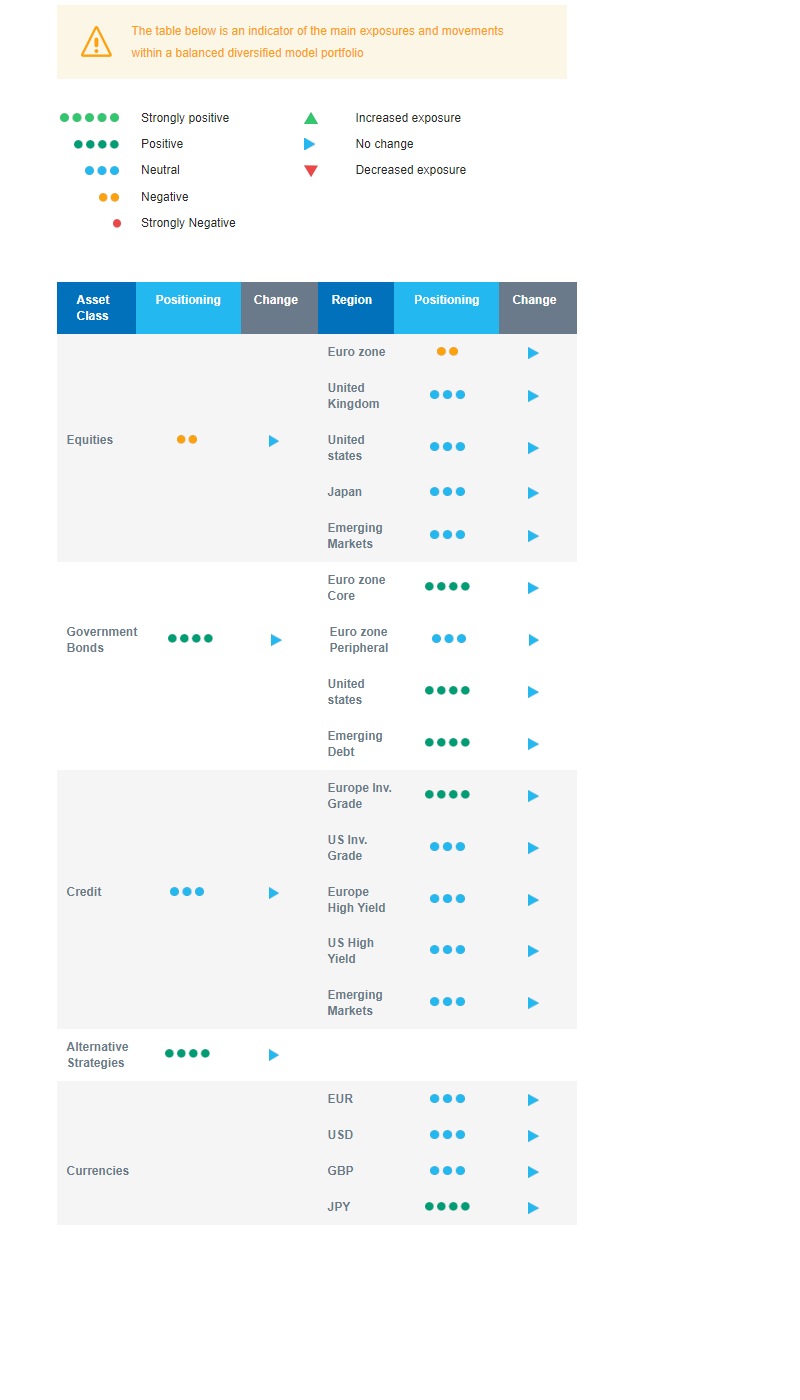

Cross asset strategy

- Our asset allocation is cautious. We expect a deceleration of economic growth which will weigh on corporate profits amid restrictive monetary policies in most of the developed countries.

- We have the following investment convictions:

- We are overall slightly underweight equities.

- In terms of regional allocation, we are underweight euro zone equities, as the likelihood of a contraction in activity has increased.

- We are neutral US, Japan and Emerging markets. The latter are vulnerable to the pressure from US rates and the headwind of the USD.

- We keep a preference for defensive, late-cycle, sectors.

- In the fixed income allocation:

- We focus on high-quality credit as sources of carry.

- We also buy core European and American government bonds. The commitment on price stability via restrictive ECB and Fed policies has driven long-term yields to attractive buying levels while the growth/inflation couple (i.e. nominal growth) eases.

- We remain exposed to emerging countries’ debt to benefit from the attractive carry.

- We hold a long position in the Japanese Yen and have exposure to some commodities, including gold, as both are good hedges in a risk-off environment.

- We expect Alternative investments to perform well as they present some decorrelation from traditional assets.

Our Positioning

While several risks have materialised this Autumn, there is relief as tail risks have receded, i.e. no overshooting in US yields, US dollar and oil. Nevertheless, our current positioning remains cautious as the deceleration of economic growth will weigh on profits. In our defensive allocation, we maintain a slight underweight positioning on equities and a long bond duration. Regionally, we are underweight euro zone equity and neutral on Japan, Emerging markets, and the US. In terms of sectors, our “late cycle” asset allocation strategy is axed around defensive sectors. In the fixed income bucket, our focus is on credit that brings carry, i.e., investment grade and emerging debt. Global growth should remain sluggish in 2024.