Last week in a nutshell

- H1 2022 ended on a sour note: it was the stock market’s worst first-half since 1970. The trigger is a combination of unexpected shocks: rampant inflation, sharp monetary tightening, a new Covid-19 outbreak in China and the war in Ukraine.

- In the US, consumer confidence took a hit and fell to a 16-month low as consumers expect weaker economic growth in the second half of the year.

- In the Euro Zone, consumer price inflation reached 8.6%, a new record high in June. This is the last reading before the expected first ECB rate hike since 2011, later this month.

- As China partially relaxed its Covid-19 containment measures, the manufacturing sector paused thanks to alleviated pricing pressures, a boost to exports and a shortening of supplier delivery times.

What’s next?

- Final June PMI for key countries are due for publication. In the US, last week’s Manufacturing ISM data revealed shrinking orders as consumer spending is slowing down and inventories are piling up.

- Amid recession fears and persistent inflation pressures, the US job report will give insight into the robustness of the labour market. In view of the weekly initial jobless claims since the month of March, a softening is expected.

- The US Federal Reserve Bank and the European Central Bank are due to publish meeting minutes giving insight into the magnitude and pace of rate hikes amid the challenging context of tightening in an economic slowdown , credit spreads are widening and stock prices are falling.

- The expected softening in the Euro Area retail sales should give details on the evolution of consumption as rising prices started to weigh on consumers' affordability and confidence.

Investment convictions

Core scenario

- While the market environment still appears constrained by deteriorating fundamentals, markets have been shaken by the latest announcements by the Federal Reserve.

- Facing multi-decade high inflation, the Fed started its hiking cycle in March and plans to add further giant steps to its funds rate by end-July and continue tightening thereafter. In our best-case scenario, the Fed succeeds in soft landing the economy. As a result, we expect the rise in the US 10Y yields to fade.

- Inflation is also at highs in the euro zone, hitting businesses, consumers, and ECB policymakers alike. The ECB pre-announced an initial rate hike for the month of July, and markets expect the announcement of new tools for periphery bond “fragmentation”.

- Facing high inflation, central bank policy tools have triggered a sharp tightening in financial conditions while the global economic slowdown is now well underway. The war in Ukraine and the COVID-19-related lockdowns in China weigh on confidence and activity. The latter should pick up during H2 in China as stimulus measures kick-in.

- The reasons for a balanced allocation have therefore not changed in recent weeks: The risks we previously outlined are starting to materialize and are now part of the scenario as the economy prepares for landing, whether it be soft or hard.

Risks

- The war in Ukraine is pushing upwards commodity prices in general and prices for energy in particular and continues to add to market uncertainties. European gas prices are at the mercy of flows staying open.

- A brutal, faster-than-anticipated rate tightening - if inflationary pressures increase further or simply persist at current levels- could jeopardize any soft landing.

- Other countries may face the Bank of England (BoE) stagflation dilemma: Even as the growth outlook deteriorates sharply, signs of upward pressure on inflation expectations, near-term wage and price setting behaviours remain.

- As visible in China, COVID-19 and its variants underline the risk of a stop-and-go in economic restrictions.

Recent actions in the asset allocation strategy

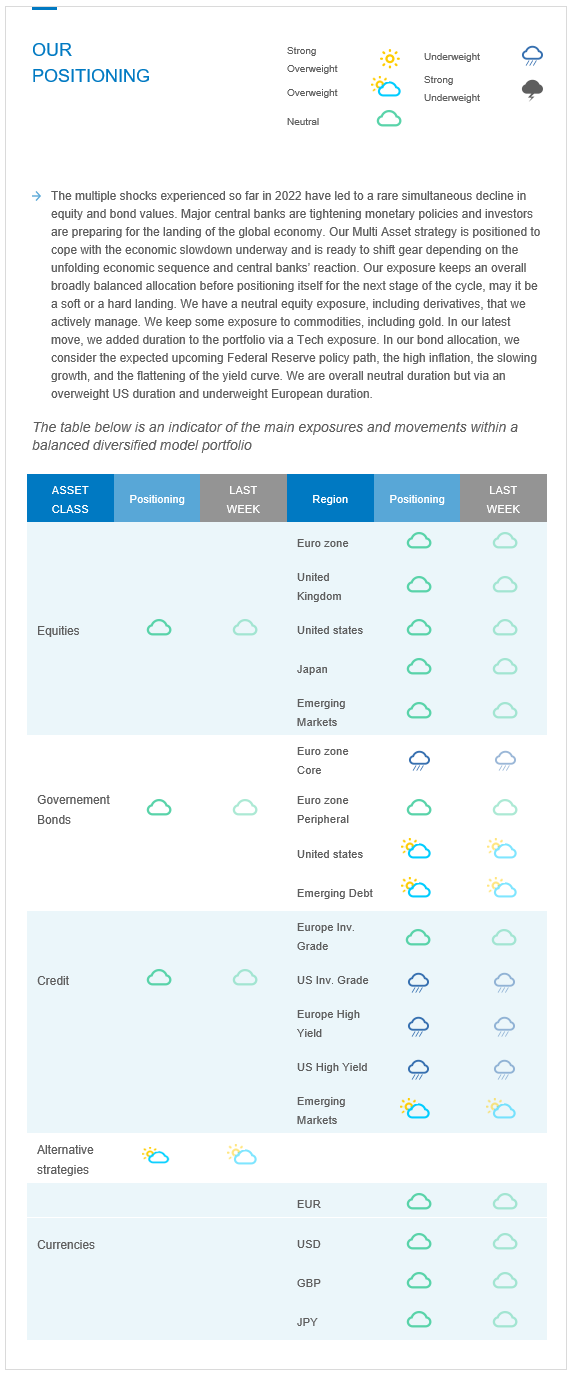

The multiple shocks experienced so far in 2022 have led to a rare simultaneous decline in equity and bond values. Major central banks are tightening monetary policies and investors are preparing for the landing of the global economy. Our Multi Asset strategy is positioned to cope with the economic slowdown underway and is ready to shift gear depending on the unfolding economic sequence and central banks’ reaction. Our exposure keeps an overall broadly balanced allocation before positioning itself for the next stage of the cycle, may it be a soft or a hard landing. We have a neutral equity exposure, including derivatives, that we actively manage. We keep some exposure to commodities, including gold. In our latest move, we added duration to the portfolio via a Tech exposure. In our bond allocation, we consider the expected upcoming Federal Reserve policy path, the high inflation, the slowing growth, and the flattening of the yield curve. We are overall neutral duration but via an overweight US duration and underweight European duration.

Cross asset strategy

- Our multi-asset strategy is staying agile. Our current positioning stays more tactical than usual and can be adapted quickly in this highly volatile context:

- Neutral euro zone equities, with a preference for the Consumer Staples sector, and with a derivative strategy in place to catch the asymmetric upside potential.

- Neutral UK equities, resilient segments, and global exposure

- Neutral US equities, with an actively-managed derivative strategy, as we remain attentive to the Fed’s forward guidance.

- Neutral Emerging markets, because our assessment indicates an improvement, especially in China, both on the COVID-19 / lockdown and stimulus fronts during H2.

- Neutral Japanese equities, as accommodative central bank, and cyclical sector exposure act as opposite forces for investor attractiveness.

- With some exposure to commodities, including gold.

- In terms of sectors, we added “long duration” assets, i.e. tech names, as we expect less headwinds from bond yields. We added exposure to the European and US tech sectors, with a preference for software companies, less cyclical and less depending on consumer confidence, over semiconductors, that are more dependent on the consumer’s behaviour.

- In the fixed income universe, we acknowledge downward revisions in growth, highs in inflation expectations and strong central bank rhetoric regarding the willingness to tighten and fight inflation. We are neutral duration but with nuances:

- We are overweight US duration after buying longer-dated bonds and selling shorter maturity notes while we are still slightly underweight euro zone duration via French bonds.

- We continue to diversify and source the carry via emerging debt.

- In our long-term thematics and trends allocation: While keeping a wide spectrum of long-term convictions, we will favour Climate Action (linked to the energy shift) and keep Health Care, Innovation, Demographic Evolution and Consumption.

- In our currency strategy, we are positive on commodity currencies:

- We are long CAD.