A Practical Framework for Fixed Income Investors

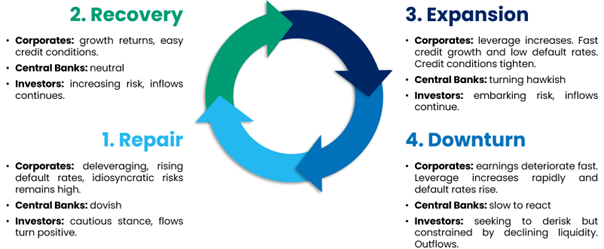

If you ask a fixed income investor to describe the credit cycle, most will readily cite its four familiar phases: Repair, Recovery, Expansion and Downturn. Knowing the terminology is straightforward. The more relevant question is: why does it matter for portfolio outcomes?

Credit cycles are a primary driver of returns in fixed income. Yet they are often misdiagnosed, oversimplified, or identified only in hindsight. While precise timing is inherently uncertain, transitions between phases tend to exhibit recurring patterns in credit spreads, issuance dynamics, leverage trends, and liquidity conditions.

;

;