Oncology innovation fuels growth

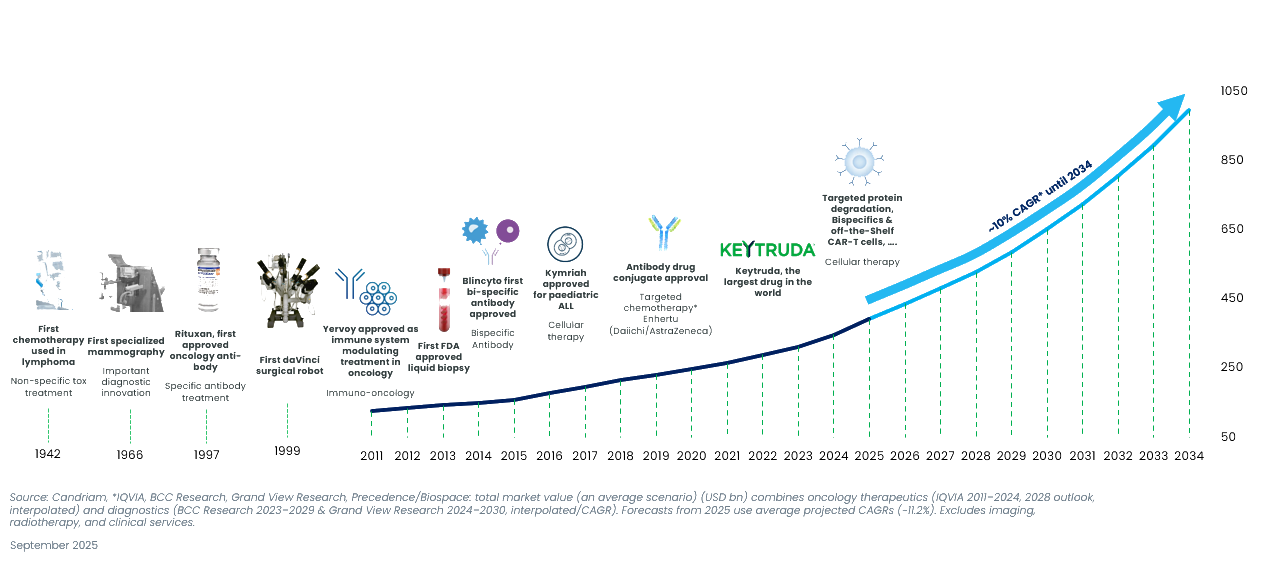

Despite notable improvements in cancer survival on the back of earlier diagnosis and advances in treatment, there remains a high unmet medical need. The future looks bright as innovation continues to improve patient outcomes. Several key trends, such as genome sequencing, biomanufacturing, liquid biopsies, and artificial intelligence, may lead to new breakthroughs. That continuing innovation fuels growth. The global oncology market (therapeutics and diagnostics) is expected to achieve double-digit annual growth from this year through 2034[1].

Global oncology market (in $ bn)

At the core of innovation and deal-making

Oncology has firmly established itself as the largest and most dynamic therapeutic area, with around 40% of the 8,325 drugs in clinical development at the end of 2024 targeting cancer[2]. The field is expected to deliver sustained double-digit growth over the coming decade, making it a prime strategic priority for healthcare companies. This focus extends beyond R&D into corporate activity, with roughly half of all M&A deals in the sector directed toward oncology[3]. Looking ahead, there is ample headroom for further consolidation: more than $400 billion in revenues are at risk from loss of exclusivity between 2025 and 2033 (Jefferies, September 2024), while the pharmaceutical industry collectively holds about $400 billion in cash (Jefferies, August 2024), providing both the incentive and the means to pursue transformative transactions.

Against this backdrop, our team has successfully positioned the portfolio in innovative, smaller companies that were later acquired by larger industry players. This demonstrates our ability to identify early-stage leaders at the forefront of oncology innovation and deal-making. Of course, many other M&A transactions have taken place in oncology in which we were not invested. The chart below highlights the transactions where our strategy directly benefited from this strong M&A activity.