Global macro conditions remained broadly constructive in February, although the backdrop was increasingly shaped by policy uncertainty and a more uneven regional growth mix. In the US, activity remained resilient, supported by solid private demand and continued AI-related investment. In the euro area, the picture improved modestly: February composite PMI rose to 51.9 and manufacturing returned to expansion at 50.8, suggesting that the long industrial downturn may be bottoming out, helped in part by stronger German order momentum. At the time of writing, the war in Iran is having devastating consequences for people across the Middle East and will cause economic pain worldwide through the disruption of energy supply chains. Market conditions may look very different to those seen at the start of the year.

Global macro conditions remained broadly constructive in February, although the backdrop was increasingly shaped by policy uncertainty and a more uneven regional growth mix. In the US, activity remained resilient, supported by solid private demand and continued AI-related investment. In the euro area, the picture improved modestly: February composite PMI rose to 51.9 and manufacturing returned to expansion at 50.8, suggesting that the long industrial downturn may be bottoming out, helped in part by stronger German order momentum. At the time of writing, the war in Iran is having devastating consequences for people across the Middle East and will cause economic pain worldwide through the disruption of energy supply chains. Market conditions may look very different to those seen at the start of the year.

Risk assets generally advanced in February, although leadership remained outside the US with stronger equity index returns in Europe and Asia. Equities were supported by improving market breadth and a rotation away from crowded US mega-cap growth into cyclicals, value-oriented segments and selected non-US markets. In Europe, industrials and energy-linked exposures remained well supported, while software and other growth-heavy segments lagged. Fixed income benefited from yields easing 20 to 30 bps in the US and Europe for 5yr and 10yr maturities. For credit, IG and HY spreads widened slightly, but remained resilient.

Commodities were mixed. Gold remained a crowded positioning theme, while oil and gas had not yet become the dominant macro shock they would later become in March.

The HFRX Global Hedge Fund EUR Index was up, at +0.30% over the month.

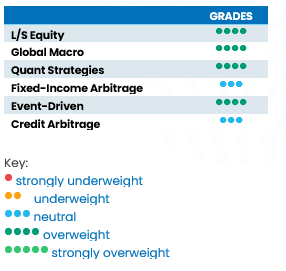

L/S Equity

February was a good month for Long-Short Equities. Directional strategies outperformed market neutral and lower net strategies as the spread between the most-owned longs and shorts was negative, particularly in Europe. Overall, however, strategies focusing on Asia and Europe outperformed more mixed results from US-focused managers. Risk management is key, as an unpredictable market environment could compress risk appetite and trigger further deleveraging. Nonetheless, Long-Short Equity strategies remain well positioned to benefit from increased dispersion across sectors, offering a supportive environment for active stock selection.

Global Macro

Global macro strategies performed well in February and have been among the best-performing strategies since the start of the year. Most performance drivers had also been present in the previous month, with returns generated by long positions in Developed Market bonds, precious metals and Asian equities, along with short US dollar exposure and selective sector positions such as cyclicals. The outlook for the strategy remains attractive, with cross-asset divergence, country growth paths and policy divergence. However crowding and geopolitical crises can reverse profitable trades, as was the case at the start of March with the outbreak of war in Iran. Given that geopolitical risk premia can fade very quickly, macro strategies will need to strike a careful balance between pursuing opportunities and portfolio hedging.

Quant Strategies

Quant strategies in February broadly mirrored the pattern seen in January. Systematic trend followers outperformed more diversified multi-strategy quantitative programmes. On average, trend-following strategies benefited from positive contributions across all asset classes, with equities and commodities making the largest contribution. Quant equity strategies continued to face challenging conditions, however, due to factor rotation and the unwinding of crowded positions. We believe that elevated macro uncertainty and uneven regional growth continue to create fertile ground for models capturing dispersion, reinforcing quants’ role as resilient portfolio diversifiers.

Fixed Income

After a strong start in January, Fixed Income arbitrage delivered a modestly positive month in February, delivering low single-digit returns on average. Positioning was likely centred on curve, swap-spread and sovereign-basis relative-value trades rather than large directional bets. The US, UK, Europe and Japan remained the key focus for our managers. The trading environment was mixed: inflation remained sticky enough to keep central banks cautious, yet not strong enough to shut down expectations of eventual easing, while geopolitical developments at month-end added a further layer of rates volatility.

Event Driven

Event-driven returns in February were dispersed with average performance ranging from slightly negative to slightly positive depending on the index or prime broker platform. Deal selection was critical, with returns driven by specific deal-spread behaviour rather than a collapse in deal activity or significant industry-wide deal-spread widening. Overall, the environment should remain favourable, with several structural and cyclical factors underpinning continued activity.

Credit Arbitrage

Credit arbitrage benefited from tight spreads and strong demand for carry, although the asymmetry of “tight risk premia” became a more visible constraint. News flow in early 2026 highlighted historically compressed IG/HY spreads, raising concerns that compensation for downside risk was shrinking. Managers favour higher-quality carry, alongside targeted idiosyncratic trades rather than broad beta exposure. In the near-term, carry should remain supportive, while the strategy’s edge will depend on security selection and liquidity management if a macro shock forces a rapid, non-linear widening from very tight starting levels.