A shock best understood through three dimensions

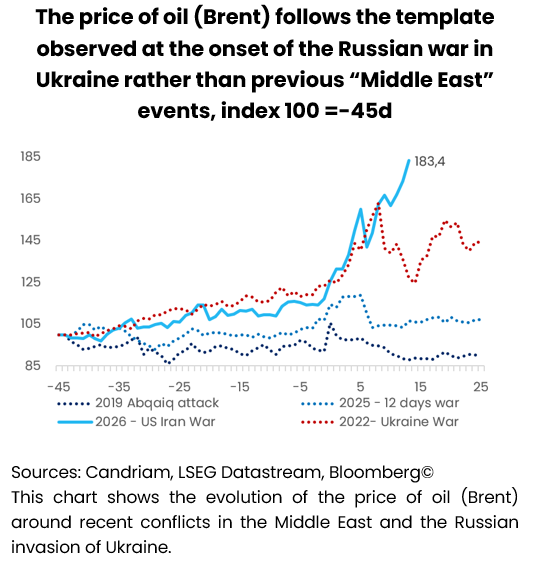

The most immediate impact of the war has been the disruption of energy and logistics flows across the Middle East. Shipping lanes and air traffic have been affected, and the Strait of Hormuz has become the focal point of investor attention. Given its central role in global oil and LNG supply, any sustained disruption immediately feeds into energy price expectations.

At this stage, the key question is therefore how the shock evolves. We frame the situation through three dimensions: duration, diffusion and depth.

Duration will determine whether the shock remains transitory or becomes embedded in the macro environment. The length of the conflict itself matters, but more importantly, we must consider the duration of the effective closure of the Strait of Hormuz and the speed at which energy production and logistics infrastructure can be restored. A short-lived disruption would likely be confined to market volatility. A prolonged disruption would feed directly into inflation and growth expectations.

Diffusion captures the extent to which the conflict spreads. A scenario in which tensions remain largely contained to Iran, with no further escalation in its retaliation, would have a different market impact than one involving broader regional contagion. Additional damage to oil and LNG infrastructure would amplify the shock, while spillovers to other commodities such as wheat or fertilisers would extend the inflation impulse beyond energy.

Depth reflects the scale of the shock on the wider economy. Markets are already reacting through energy forward curves and rising inflation expectations. The key variables to monitor are the reaction functions of central banks as inflation risks re-emerge, as well as the impact on consumer confidence, corporate spending and ultimately on GDP growth. The deeper the shock, the more likely it is to alter policy trajectories and financial conditions.

The European predicament

Oil and gas prices have moved sharply higher, reflecting fears of prolonged supply constraints and infrastructure damage. Shipping costs have surged, amplifying supply-chain frictions and reinforcing the inflation impulse. The European predicament is defined by a structural trap: while economies have reduced gas consumption, this shift reflects a painful erosion of the industrial base rather than a move towards true resilience.

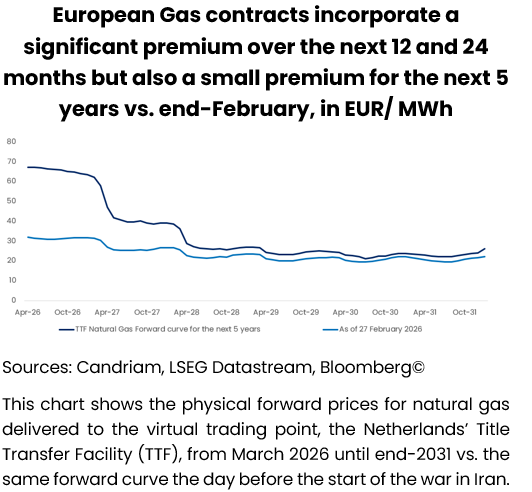

Specifically, European economies remain highly vulnerable to gas price dynamics, as illustrated by the persistent premium embedded in forward contracts. The Title Transfer Facility (TTF) contract curve, the European reference for the price of natural gas, shows additional premiums of EUR 20 and EUR 15 over the next 12 and 24 months compared to end-February levels, signalling that markets expect elevated energy costs to persist.

This is particularly critical for Europe’s industrial base, where sectors such as chemicals and steel remain structurally exposed to gas prices. Despite some adjustment through efficiency gains and demand destruction, gas consumption remains well below pre-2022 levels, reflecting curtailed production rather than true resilience. With energy costs still significantly higher than in competing regions such as the US, European industry faces an ongoing competitiveness gap, weighing on output, investment decisions and, ultimately, growth prospects.

Central banks navigating policy ambiguity

Beyond commodities, energy shocks act as a drag on growth by eroding purchasing power and weakening confidence. At the same time, they complicate the inflation outlook, particularly at a time when central banks were approaching a more balanced policy stance. The longer the disruption persists, the greater the risk that the macro mix shifts towards a stagflationary configuration. Against this backdrop, the focus shifts to central banks. Markets expect them to keep rates on hold in the near term, but the guidance they provide will be critical.

The challenge is that inflation dynamics are once again being driven by external energy factors rather than domestic demand. In the United States, the rise in gasoline prices to 3.84USD/gal has already begun to weigh on consumer sentiment. While inflation had been moderating, the energy shock introduces renewed upside risks. This places the Federal Reserve in a complex position. Further easing now appears conditional on the evolution of energy prices. Inflation credibility is not the issue; rather, it is the uncertainty around how persistent the shock will be and how it feeds into expectations.

In Europe, the situation is more sensitive still. As shown above, the region’s exposure to imported energy, particularly LNG, makes it vulnerable to renewed inflation pressure. The ECB is no longer “in a good place” and may need to manage inflation expectations more actively.

Meanwhile, the Bank of Japan and the Reserve Bank of Australia remain in tightening mode, reflecting domestic dynamics that differ from those in other developed markets. This divergence reinforces the complexity of the global policy landscape.

Macro conditions remain supportive, but secondary

Before the outbreak of the conflict, macro conditions remained broadly supportive. Growth was resilient, particularly in the United States, where private domestic demand and investment continued to drive activity. Europe too showed signs of stabilisation, supported by improving domestic demand and fiscal measures, while China remained more constrained, with structural challenges limiting its growth momentum despite policy support.

However, in the current environment, macro fundamentals are no longer the dominant driver of market performance. Instead, geopolitical developments and their impact on energy and inflation are shaping the outlook more directly. A sustained increase in oil prices would weigh on growth and push inflation higher, potentially delaying monetary easing and tightening financial conditions. A prolonged disruption to energy flows could amplify these effects and shift the macro balance towards stagflation.

Portfolio positioning: reducing risk amid heightened uncertainty

Given the escalation of the conflict and the uncertainty surrounding its duration, diffusion and depth, we have reduced overall portfolio risk and moved to a more balanced stance across asset classes.

On equities, we are now broadly neutral, with a slight overweight in the United States. We have downgraded Europe, Japan and Emerging Markets to neutral, reflecting their higher sensitivity to energy prices and global trade dynamics.

In fixed income, we have reduced overall exposure, while maintaining a modest overweight in core European duration, albeit at a lower level than previously. Credit markets have shown resilience, but spreads remain tight. In this context, we favour a selective, quality-biased approach rather than broad risk-taking. We have moved European Investment Grade to neutral and taken a slightly negative stance on US High Yield, where the risk-reward profile has deteriorated. We retain an overweight in Emerging Market debt, both in hard and local currency, supported by attractive yields and carry.

In currencies, we remain underweight US dollar, though less so than previously given the renewed geopolitical demand. We maintain long positions in commodity-linked currencies such as AUD, NOK and BRL, as well as a long Japanese yen position for diversification.

Overall, the portfolio reflects a more cautious navigation through the current environment, with reduced directional risk and a greater emphasis on carry, diversification and resilience.

Looking ahead

Financial markets remain dominated by geopolitical developments and their macro implications. How the war in Iran evolves will determine whether it remains a source of volatility or becomes a more persistent economic shock.

The framework of duration, diffusion and depth provides a structured way to assess this evolution. It highlights the key variables investors should monitor and underscores the conditional nature of the current outlook.

Until greater clarity emerges, a disciplined and selective approach to portfolio construction remains essential. In a world where energy, geopolitics and policy are increasingly intertwined, central banks and their reaction functions will remain firmly at the centre of market attention.