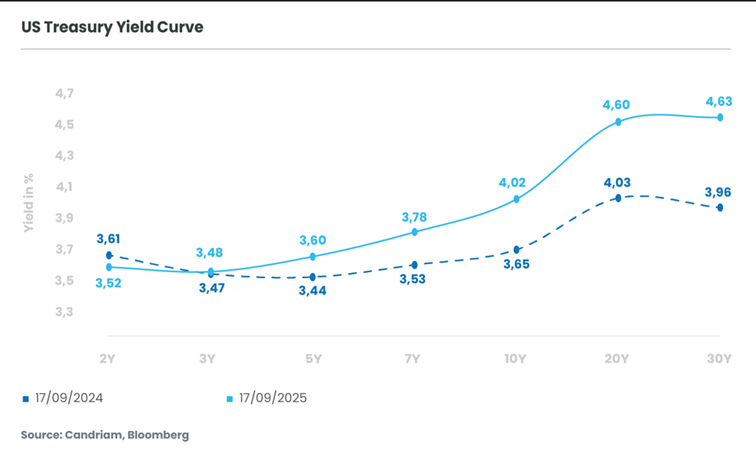

Tariffs, Trade, and Tension

All considered, the probability of steepening has increased markedly. Tariff rates, though somewhat lower than feared in April, are now being implemented and will likely exert a structural drag on corporate margins and global trade flows. The US economy must now traverse a narrow corridor between resilient growth and contained inflation if the Fed is to be shielded from political interference, and equity markets to avoid instability. Additional progress on the China trade front, following recent deals with Japan and the EU, could bolster global growth expectations and rekindle inflationary pressures. Such a scenario would add upward pressure on long yields precisely when the Fed’s policy options remain one-sided. The structural imbalance between fiscal expansion and constrained monetary flexibility argues strongly for a steeper US curve.

Europe’s Anchored Front-End and Pressured Long-End

In Europe, the trajectory is shaped less by political pressure and more by fundamentals. Inflation dynamics are decisively downward: weak demand conditions across much of the region, compounded by China’s disinflationary impulse, have anchored expectations. Even Germany’s fiscal stimulus is unlikely to trigger sustained price pressures. With growth prospects subdued, demand-driven inflation is improbable, meaning the ECB is unlikely to tighten. Instead, it is poised either to hold or to ease further, ensuring the short end remains well-anchored, if not lower. Yet, pressures are building at the long end. Sovereign debt issuance continues to rise across core European markets. Technical factors are also involved: regulatory changes which provide incentives for Dutch pension funds to reduce duration exposure are generating structural outflows from the long end of the curve. The combination of subdued short-end rates and long-end supply pressure is thus primed to generate a steepening across European curves, albeit at lower nominal levels than in the US.

Tactical Rate Opportunities

The transition to steeper curves carries profound implications for rate markets. In the US, steepening will likely take the form of a bull-steepening — driven more by front-end yields collapsing on the expectation of rate cuts than by an aggressive sell-off at the long end. This creates opportunities for investors to position in the 2- to 5-year segment, where yields remain elevated but are poised to benefit most directly from policy easing. At the long end, caution is warranted: persistent fiscal deficits, elevated Treasury supply, and lingering inflation uncertainty leave 10- and 30-year yields vulnerable to repricing. In Europe, a similar dynamic emerges: the short end anchored by an accommodative ECB, but the long end exposed to rising issuance and technical outflows. Investors may find relative value in holding intermediate maturities in the 5Y – 7Y range, while maintaining a defensive stance on the far end of the curve.