Back to corporate fundamentals?

With the upcoming earnings season, investor attention is shifting back to fundamentals. The first signals are constructive, with Q1 results starting on a solid footing and earnings expectations revised upward, led by Technology, Energy and Basic Materials. In a market dominated by geopolitical headlines, this renewed focus on profit growth helps explain the resilience of equities. Corporate fundamentals remain broadly supportive, even as the macro environment becomes more uncertain.

Within Technology, the contrast between infrastructure and applications remains central. With more than USD 700 billion expected to be invested by hyperscalers in AI infrastructure in 2026, visibility on demand remains strong. Order books are full, production capacity remains constrained and earnings revisions continue to move higher, supporting the AI infrastructure ecosystem.

On the software side, however, the narrative has shifted. The emergence of advanced AI agents has triggered a reassessment of business models, as these tools increasingly replicate tasks traditionally performed by SaaS and IT services providers. This has led to downward revisions in long-term growth and margin expectations, explaining the sector’s underperformance. That said, the repricing remains uneven: companies linked to data storage, processing, protection and cybersecurity are better positioned to absorb the disruption. At the same time, an additional source of risk is emerging. Potential IPOs in the second half of the year – from players such as Anthropic, OpenAI and SpaceX – could mobilise close to USD 4 trillion in capital, creating a significant absorption of liquidity and increasing competition for investor allocation. Beyond AI, interest rates and recession concerns continue to influence the Tech sector’s trajectory.

A shock settling in

What began as a geopolitical disruption is now settling into a more persistent phase. The conflict has entered its eighth week. A ceasefire has been announced, but no durable agreement has been reached, and the Strait of Hormuz remains only partially functional. The key issue is no longer the military timeline, but how long energy flows remain constrained. As long as shipping traffic is disrupted and production cannot fully normalise, the shock extends beyond market volatility and feeds directly into inflation, confidence and growth.

At the same time, the conflict has broadened. Damage to energy infrastructure in Saudi Arabia and Qatar confirms that the risk is no longer contained to Iran. Pressure is no longer limited to oil and gas: spillovers to sulphur, fertilisers and agricultural commodities are widening the inflation channel and amplifying the macro impact. This is already visible: energy prices remain elevated; inflation expectations have moved higher and financial conditions have tightened. Consumer confidence is weakening, corporate spending is becoming more cautious, and growth expectations are being revised lower. The shock is no longer prospective – it is underway.

Therefore, our base case remains more cautious than at the start of the year. The probability of a short-lived oil spike has declined, while a multi-month disruption has become more likely. In such a scenario, oil prices remain elevated for several months, growth slows and inflation rises before stabilising.

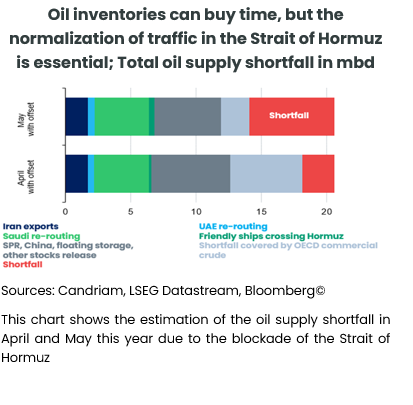

Oil inventories can buy time, but they cannot fully offset a sustained disruption. The April configuration shows that re-routing flows from Saudi Arabia and the UAE, combined with releases from strategic reserves and commercial stocks, can cover a significant share of lost Iranian exports, limiting the immediate shortfall. By May, however, the gap widens despite similar mitigation efforts: re-routing capacity and friendly shipping flows plateau, while reliance on inventories increases, leaving a more visible residual deficit. The persistence of a shortfall, even with coordinated stock releases, highlights that these buffers are temporary. Ultimately, only a normalization of traffic through the Strait of Hormuz can restore balance to global oil supply.

Markets are adjusting accordingly. Higher oil and higher yields leave less room for central banks to cushion the shock. Europe remains the most exposed among developed markets given its dependence on Middle Eastern energy. Japan faces similar pressures, while many emerging markets face higher import costs and weaker trade. The United States remains relatively more insulated, but not immune.

Policy under constraint

Central banks now face a more complex trade-off. The oil shock and rising inflation expectations limit their ability to ease policy, even as growth risks increase. In the United States, further easing is increasingly conditional on the evolution of energy prices. The Federal Reserve is unlikely to react to short-term spikes, but a prolonged increase would delay policy normalisation.

In Europe, the situation is more delicate. The ECB is no longer operating in a comfortable environment and must manage renewed inflation pressure linked to energy and LNG dynamics. Under a more persistent shock scenario, policy tightening cannot be excluded.

At the same time, Japan and Australia remain in tightening mode, reinforcing global policy divergence. The common feature is clear: policy flexibility is narrowing. Central banks are reacting to an external shock that they cannot control but must incorporate into their frameworks.

Portfolio positioning: neutral risk

Before the escalation, macro conditions remained broadly supportive. Growth was resilient, particularly in the United States, where private demand and investment continued to drive activity. Europe was stabilising, supported by domestic demand and fiscal measures, while China remained constrained but stable. However, macro fundamentals are no longer the primary driver of market performance. The dominant forces are now energy dynamics and policy expectations. Growth is no longer setting the direction of markets. Instead, markets are reacting to changes in inflation expectations and financial conditions and are increasingly focusing on corporate fundamentals.

Given the heightened uncertainty, we have contained overall portfolio risk and moved to a more balanced stance.

On equities, we are now broadly neutral across the geographical spectrum. The war in Iran has led to a decline in equity valuations in recent weeks. This is not yet a sufficient entry signal for us: we remain ready to re-engage with risky assets should the Strait of Hormuz reopen, oil stabilise toward USD80-85/barrel, and rate pressures ease. The United States remains relatively insulated thanks to domestic energy production and resilient demand. In addition, attractive Tech valuations represent a support for the stock market. This relatively better position is reflected in a somewhat higher valuation than the other regions. We hold a neutral stance on Europe, Japan and Emerging Markets, reflecting their higher sensitivity to energy prices and global trade dynamics.

In fixed income, we have reduced duration exposure, particularly in Europe where inflation sensitivity is higher. US Treasuries remain neutral. In credit, spreads have not widened sufficiently to create a broad opportunity set. We have adopted a more cautious stance overall and hold a neutral view on European and US Investment Grade. Our view on US High Yield remains slightly negative, reflecting deteriorating technicals and increased macro sensitivity. We retain a neutral view on Emerging Market debt, which remains supported by attractive (real) yields and carry, even in a more volatile environment.

Commodities and currencies: risk and protection

Higher commodity prices illustrate the dual nature of the current regime. They represent a clear macro risk, but also a source of portfolio protection.

A sustained increase in oil prices would weigh on growth and push inflation higher, tightening financial conditions. At the same time, commodities provide diversification benefits. Precious metals, particularly gold, remain a key allocation as a hedge against geopolitical risk and real rate volatility. We remain constructive on metals more broadly, supported by structural demand and their role in a more uncertain environment.

In currencies, we maintain long positions in commodity-linked currencies such as AUD, NOK and BRL. We remain underweight the US dollar, although less so than previously given the geopolitical backdrop, and maintain a long Japanese yen position for diversification.

Managing instability

The war in Iran has reshaped the macro environment within a matter of weeks. The combination of higher inflation, weaker expected growth and constrained policy responses is rare and challenging for markets.

The recent pause in military activity has provided some relief, but the underlying situation remains unresolved. The key variables are clear: the reopening of the Strait of Hormuz, the stabilisation of oil prices and the easing of pressure on interest rates. As discussed above, de-escalation in the Middle East has helped markets to shift back to fundamentals as the earnings season has started but a new escalation could be just around the corner.

Until more stable conditions are met, relative caution remains warranted. We have repositioned portfolios defensively and maintain flexibility to adjust as conditions evolve. In a regime defined by repeated shocks, success depends less on predicting outcomes and more on managing uncertainty. We remain prepared to act quickly in either scenario: further de-escalation, or a resumption of the war. In giving peace a chance, we prefer to be neutral since the outcome of the negotiations is uncertain.