Last week in a nutshell

- The odds of a Fed rate cut in March have been erased by the hawkish tone of Chairman Powell and the unexpected addition of 353K nonfarm payrolls to the US economy.

- The euro zone economy stabilised in Q4 2023, avoiding a predicted recession, while preliminary figures for the headline inflation eased.

- The US earnings season continued with mixed results. The “Magnificent 7” were pulled by Meta and Amazon, while some small US Banks showed weaknesses on deteriorating commercial real estate loans.

- The 2024 Democratic nominating contest for the presidential election kicked off in South Carolina. Joe Biden won the state.

What’s next?

- The Fed will release its quarterly Senior Loan Officer Opinion Survey. The document helps assess lending standards to households and businesses.

- Final Services and Manufacturing PMI are due for key countries as well as industrial production for Germany, Italy and Spain.

- The euro zone will release PPI figures and Consumer Inflation Expectations as well as retail sales, as investors are trying to gauge the ECB’s initial rate cut timing.

- The earnings seasons continues with releases stemming from Disney, Eli Lilly, L’Oréal, PepsiCo, McDonald’s and the French luxury design house, Hermes.

Investment convictions

Core scenario

- Inflation gave way and is set to fall rapidly below 3% in both the US and the euro zone, and is no longer a primary concern for investors. The growth / inflation mix is thereby finally returning to “familiar” territory although the start of the year could be somewhat bumpy.

- A soft-landing/ongoing disinflation scenario in the United States remains our most likely scenario, implying no rush for the Central bank to deliver monetary support. We don’t expect the first monetary easing before the end of H1 2024, still leaving room for disappointments compared to current market pricing.

- 2024 should bring better visibility with a narrowing economic growth gap between countries while most central banks have restored room for manoeuvre.

- In China, economic activity has shown some fragile signs of stabilisation (4% GDP growth expected in 2024) while the evolution of prices remain deflationary.

Risks

- Geopolitical risks to the outlook for global growth remain tilted to the downside as developments in the Red Sea unfold. An upward reversal in the price of Oil, US yields or the US dollar are key variables to watch.

- A risk would be a stickier inflation path than expected which could force central banks to reverse course.

- Similarly, financial stability risks could return as a result of the steepest monetary tightening of the past four decades and the tightening in financial conditions.

- While uncertainty remains on the timing and on the conditions of the start of monetary easing, an upside risk would be an earlier exit from central banks’ restrictive monetary policy.

Cross asset strategy

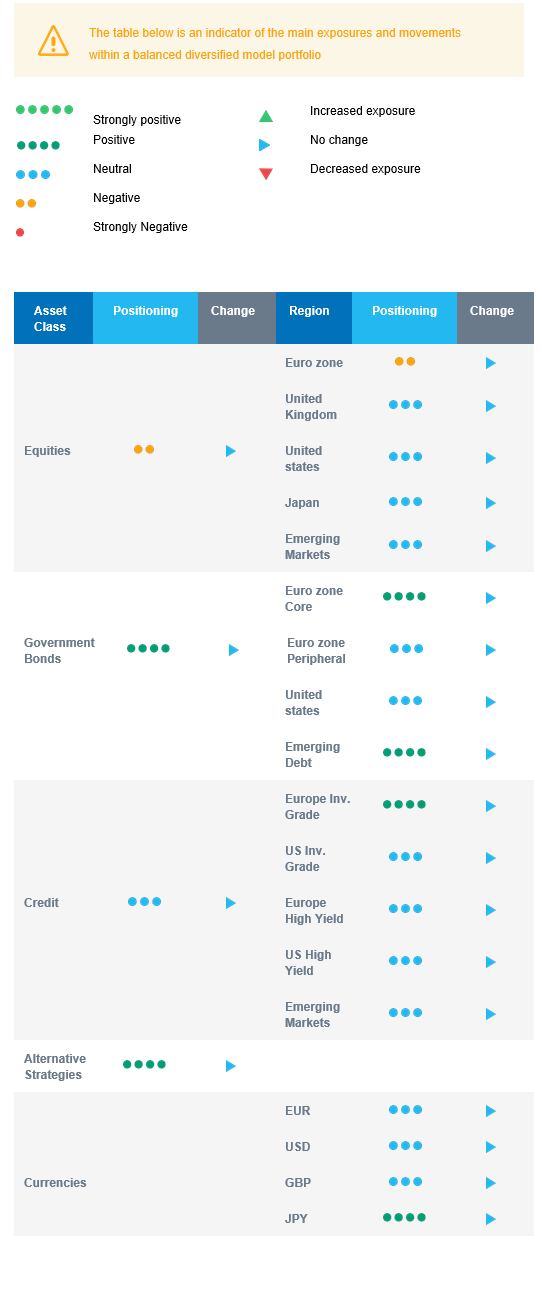

- Our asset allocation shows a relative preference for bonds over equities as the equity risk premium is currently insufficient to encourage investors to reweight the asset class.

- We have the following investment convictions:

- We expect limited equity upside, and are currently slightly underweight on equities pending a better risk/reward and clearer signals on when to increase our exposure. We have a cautious view on euro zone equities and are neutral on other regions.

- We look for specific themes within Equities. Among them, we like Technology / AI and look for opportunities in beaten down stocks in small and mid-caps or within the clean energy segment. We also remain buyers of late-cycle sectors like Health Care and Consumer Staples.

- In the fixed income allocation:

- We focus on high-quality credit as sources of carry.

- We also buy core European government bonds with the objective to benefit from the carry in a context of slowing economic activity and cooling inflation.

- We remain exposed to emerging countries’ debt to benefit from the attractive carry.

- We still hold a long position in the Japanese Yen albeit after some profit taking and have exposure to some commodities, including gold, as both are good hedges in a risk-off environment.

- We expect Alternative investments to perform well as they present some decorrelation from traditional assets.

Our Positioning

Our strategy takes into account that sentiment has turned bullish, imbalances have risen and financial markets are calling into question Fed interest rate cuts as early as March. With equities becoming relatively less attractive, we look for specific themes within this asset class. In terms of sectors, we are constructive on the Technology, Health Care and Consumer Staples sectors. Within regional equities, we are underweight euro zone and have a relative preference for US equities. We remain neutral Emerging markets and Japanese equities. We maintain a long European bond duration and a neutral US duration. Our focus is also on credit bringing carry, i.e., investment grade and emerging debt.