Last week in a nutshell

- China’s economy expanded by 4.9% YoY in Q3, beating forecasts and nearing the official annual target of around 5%. Doubts about a sustained stimulus persist.

- The US 10Y yield neared 5% while Fed Chair Jerome Powell noted that inflation was still too high and that a sustainable return to the 2% inflation goal was likely to lead to a period of below-trend growth.

- On the geopolitical front, intense diplomatic efforts sought to mitigate concerns that Israel’s war with Hamas would spark a bigger conflict in the energy-producing Middle East.

- Most of the big US banks came out with better-than-expected Q3 earnings, citing ongoing business trends in favourable terms amid headwinds.

What’s next?

- The meeting of the European Central Bank will be in the spotlight. The broad consensus is calling for a standby, but oil prices and labour market strength keep upside risks to inflation alive.

- Flash PMI’s from the US, Japan and Europe will be published as investors carefully monitor the 50-mark threshold between contraction and expansion for manufacturing and services activity.

- In the US, a series of data covering first estimates of the GDP growth rate, core personal consumer expenditure deflator, real consumer spending and real estate will be published.

- The Q3 2023 earnings season continues. Microsoft, Amazon, Facebook, and Alphabet are some of the weeks’ highlights.

Investment convictions

Core scenario

- In terms of economic growth, we expect the US to avoid a recession providing that long-term rates do not remain too long at the current level. In Europe, growth is likely to remain lacklustre for most of next year, and the likelihood of a recession is increasing in the region. In China, economic activity and the evolution of prices have shown some timid signs of cyclical stabilisation.

- The resilience in both inflation and labour markets and the persistent hawkish bias of developed countries’ central banks have led to an upward repricing in bond yields. Meanwhile, China’s likelihood to export deflation to the world is fading only slowly.

- The markets’ response of higher long-term bond yields indicates a shift from recent trends: the yield curves do not invert further anymore as investors re-asses upward the premium for holding long-term yields.

- In summary, the increase in real rates is a headwind for equity valuations while the deceleration of economic growth will weigh on profits. Risks to the outlook for global growth remain tilted to the downside as geopolitical developments unfold.

Risks

- A temporary overshoot in longer-dated bond yields present a risk for fixed income holdings and duration-sensitive equities.

- The steepest monetary tightening of the past four decades has led to significant tightening in financial conditions. Financial stability risks could return.

- A stickier inflation path than already expected could force central banks to hike even more, which implies that the growth outlook is tilted to the downside.

- Besides geopolitical tensions on several fronts, which imply rising uncertainty and vulnerabilities, as well as a potential increase in oil prices, the US elections of November 2024 are looming fast.

Cross asset strategy

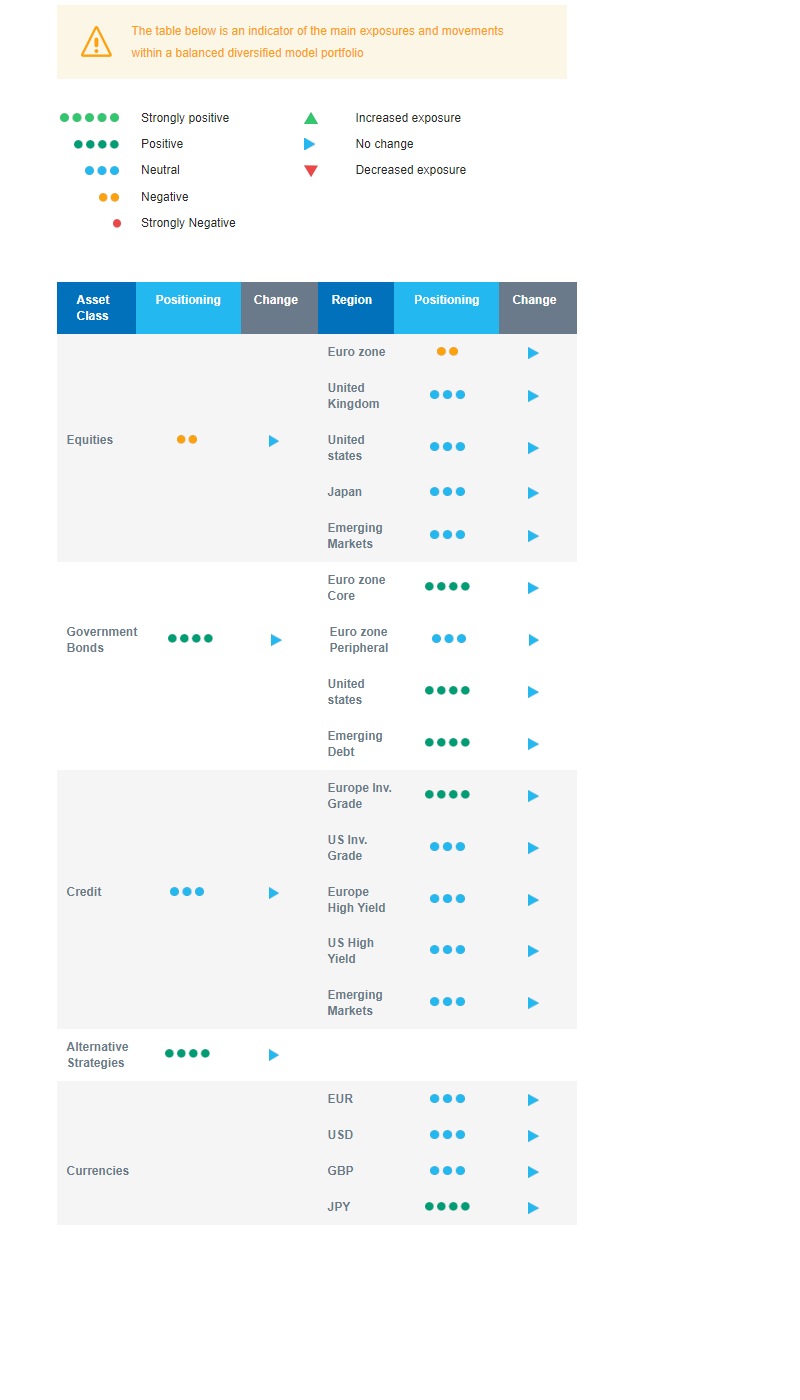

- Our asset allocation has turned more cautious as several risks have started to materialise. We expect a deceleration of economic growth which will weigh on corporate profits amid restrictive monetary policies in most of the developed countries.

- We have the following investment convictions:

- We are overall underweight equities and while market sentiment is less stretched, it is too early to buy back equities.

- We are underweight euro zone equities, as the likelihood of a contraction in activity has increased.

- We are neutral US, Japan and Emerging markets. The latter are vulnerable to the increasing pressure from US rates and the headwind of the USD.

- We keep a preference for defensive, late-cycle, sectors.

- In the fixed income allocation:

- We focus on high-quality credit as sources of carry.

- We also buy core European and American government bonds. The commitment on price stability via a hawkish ECB policy has driven long-term yields to attractive buying levels while the growth/inflation couple (i.e. nominal growth) eases.

- We remain exposed to emerging countries’ debt to benefit from the attractive carry.

- We hold a long position in the Japanese Yen and have exposure to some commodities, including gold as both are good hedges in a risk-off environment.

- We expect Alternative investments to perform well as they have some decorrelation from traditional assets.

Our Positioning

Our positioning has turned more cautious as several risks have started to materialise. The increase in real rates is a headwind for equities while the deceleration of economic growth will weigh on profits, leading us to adopt a defensive allocation, including an underweight positioning on equities and a long bond duration. We are underweight euro zone equity. We are neutral on Japan, Emerging markets, and the US. In terms of sectors, our “late cycle” asset allocation strategy is axed around defensive sectors. In the fixed income bucket, our focus is on credit that brings carry, i.e., investment grade and emerging debt while being more cautious on high yield. Global growth should remain sluggish in 2024 but the risk appears tilted to the downside as geopolitical developments unfold.