Although European long term interest rates eased overall in 2019, they have steepened since September. The causes for the downturn last year were largely commented on, including political uncertainties and trade fears and more particularly the accommodating policies adopted by the central banks.

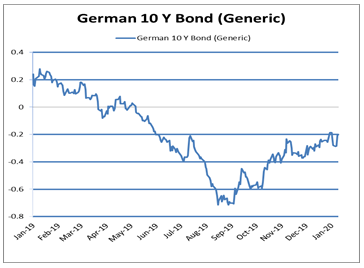

Over the past few weeks, we have nonetheless underweighted our portfolios in core European bonds, chiefly Germany and France. The current level of German 10-year yields, at around -0.20%, has triggered interest among chartists and raised questions with regard to potential trends over the next few weeks.

As demonstrated in chart 1, generic German 10-year bonds are yielding 0.35% below their level at the start of the year and close to the level recorded in July. It is interesting to note that the low point occurred a few days before the ECB meeting which decided to cut refinancing rates and relaunch quantitative easing, accompanied by a tiering system.

Let us analyse 2019 therefore in two periods with regard to the low point, i.e. before 12 September and after this date.

Analysis 1: Long term rates reflecting growth and inflation outlook

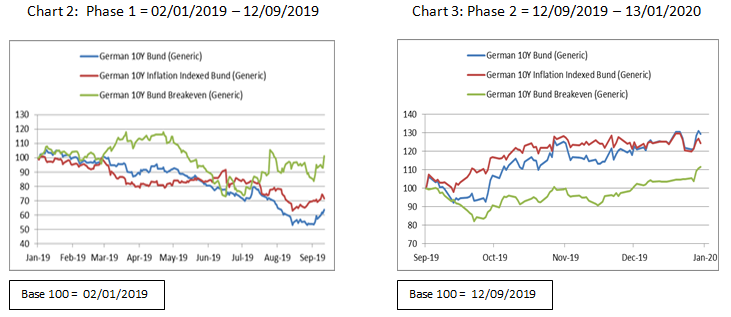

Several types of analysis can be applied. The most common method however is to break down the generic bond rate by comparing its yields with the generic inflation indexed 10-year rate and the so-called 10-year breakeven rate which represents the influence of inflation.

During the first phase (chart 2),relatively strong divergence can be observed between factors accounting for the variations in German bonds. Inflation indexed bonds eased in parallel with sovereign generic bonds. Given that these types of bonds are supposed to provide protection against inflation, pricing tensions cannot therefore theoretically affect them. Fluctuations observed would therefore be considered to be due chiefly to lower growth outlook.

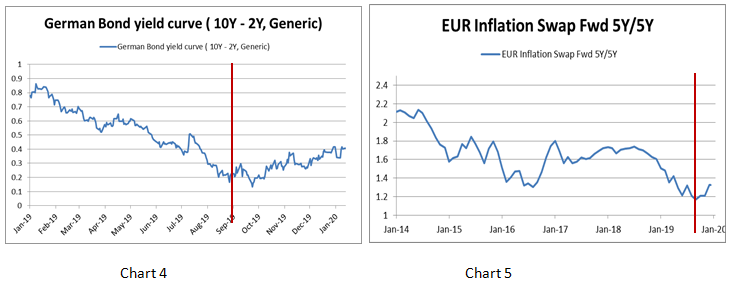

During the second phase (chart 3) on the other hand, inflation indexed bond yields steepened. An increase in breakeven bond yields was also observed due to a rise in the oil price which had a significant impact on the inflation comparison base. It is also interesting to note in the chart below that the yield curve began to steepen during phase 2 (chart 4). Tiering and the consequent rise in short term rates would therefore not have sufficient influence to account for tensions among long term rates.

Analysis 2: Long term rates reflect long term bond investor appetite

It may also be useful to use a term spread analysis. This variable is defined as the compensation required by investors in return for holding a long term bond, rather than shorter term maturities which are renewed at their term. It may account for fluctuations in the yield curve and therefore investor appetite for long term bonds. Recent studies have demonstrated a high level of correlation (90%) between downgrades in investor inflation outlook and the term spread in Europe [1]. Chart 5 above reflects a steady decline from mid-2014 onwards followed by a sharp downturn in in 2019. Outlook has begun to improve slightly since September 2019 apparently underpinned by rising oil prices and the resulting impact on the comparison base. This increase may therefore contribute to interest rate tensions as reflected recently among breakeven bonds.

Analysis 3: Long term rates, resulting from monetary policy

Quantitative easing implemented by the ECB is clearly one factor accounting for the level of long term rates in Europe and Germany. Its influence must be viewed in the perspective of the rules governing buybacks implemented by the central banks, along with issue volumes and their timetable. The Bundesbank owns almost 33% of issues, which is close to the ceiling level set under the current rules and will therefore be limited in the scope of its forthcoming acquisitions. Although net issues in Germany this year are negative (-54 billion euros), the issuance timetable demonstrates that there will be a heavy supply of bonds during the first quarter (+ 51 billion euros).

Favourable economic environment

Growth outlook has improved sharply since the end of August - early September as reflected in chart 6 and has continued to increase over the past few weeks.

As such, with regard to the comparison base impact of the oil price increase on inflationary outlook, combined with the Q1 issuance timetable and expected economic forecasts in Europe which continue to surprise positively, we are maintaining our short duration positioning within our portfolios.

[1] Unicredit, Rates outlook, N°74, 04/11/2019