European equities: Technology defies a slight decline in European equities

European equities have experienced a slight contraction since the last Equity Committee in April, amid several macroeconomic headwinds. The collapse of Middle East ceasefire talks renewed geopolitical concerns and disrupted supply chains. At the same time, eurozone inflation unexpectedly rose to 3.0%[1], prompting a more hawkish stance from the European Central Bank that forced investors to price in upcoming interest rate hikes. Against this backdrop, the Information Technology sector delivered a strong performance, increasingly matching the Energy sector’s performance since the start of the year[2].

Information Technology led the way

Since the last Committee, Information Technology has been by far the best-performing sector[3]. The sector was supported by semiconductors, which benefited from better-than-expected Q1 earnings, accelerating capex from hyperscalers and rising orders from several end-markets, including automotive and industrials. By contrast, software and IT services continued to suffer from concerns over potential AI disruption.

Aside from IT, only one sector delivered a positive performance over the period: Materials, which improved slightly thanks to metals & mining stocks. These benefited from surges in copper, aluminium and iron ore spot prices.

All other sectors declined over the period, with no clear dispersion between cyclicals and defensives.

Among cyclical sectors, Consumer Discretionary and Real Estate were the worst performers, weighed down by a damaging combination of rising consumer inflation and a sharp increase in long-term interest rates. Financials and Industrials proved more resilient, although they still ended the period in negative territory.

Within defensive sectors, Healthcare significantly underperformed due to unfavourable sector rotation. Energy also underperformed due to a sharp drop in crude oil prices triggered by a fragile pause in hostilities in the Middle East. Consumer Staples and Utilities were also in negative territory, albeit to a lesser extent.

In terms of market capitalisation, performance has broadened. Small caps have outperformed both mid and large caps since the last committee, benefiting from compelling valuations and their domestic profile.

Positive earnings revisions for IT and energy

European EPS are expected to grow by 12% in 2026, according to Bloomberg data as at 8 May 2026. Consumer Discretionary remains the sector with the highest expected growth, at 55%, thanks to favourable base effects. This is followed by Materials at 29% and Communication Services at 20%. Healthcare and Consumer Staples are the sectors with the lower expected EPS growth, at 3% each[4].

Since the last Equity Committee, European valuation multiples have remain stable, with the 12-month forward P/E ratio still standing at 15.3x. IT and industrials remain the most expensive sectors, trading at 32.7x and 23.5x respectively, while Energy and Financials remain the cheapest, at 8.8x and 11.1x respectively, according to Bloomberg data as at 8 May 2026.

Earnings estimates for 2027 stand at +9% at MSI Europe level, with 51% of earnings revisions positive over one month. Revisions have been most positive for IT (56%) and Energy (54%)[5].

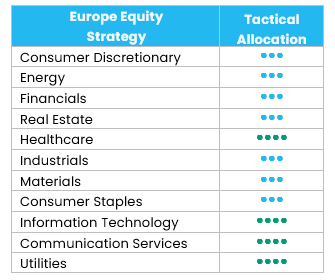

European Healthcare sector upgraded to +1

We upgraded the European Healthcare sector to +1 from neutral, to align it with the rating assigned to the Pharmaceuticals, Biotechnology & Life Sciences subsector (which represents 89% of the European healthcare index). This also brings the rating in line with our US rating. We have kept the other grades unchanged.

US equities: Robust earnings support the market

Technology leads rebound

US equities performed strongly over the past month, with the MSCI USA gaining over 6%[6] since our last Equity Committee, underpinned by resilient macroeconomic data and a robust earnings season. While geopolitical risks, particularly in the Middle East, remain in focus, investors placed greater emphasis on fundamentals.

Beneath the surface, performance dynamics have been more nuanced. Cyclical sectors lagged the broader market. Financials stood out as the main underperformer, reflecting heightened inflation fears and ongoing pressure from the interest rate environment. Defensives were also a mix bag, with Healthcare and Utilities in particular underperforming the broader market. This pattern suggests a shift in market positioning.

Information Technology benefited from the market rotation and was the key market performance driver. The sector has delivered strong earnings, fuelled by persistent demand linked to artificial intelligence and ongoing data centre investments. Analysts have continued to revise their earnings estimates upwards, especially for semiconductors and technology hardware. Recent earnings releases have once again confirmed the strength of the AI ecosystem, reinforcing confidence in the sustainability of these trends.

From a style perspective, the market has remained relatively balanced overall, but recent weeks have seen a clearer shift back towards growth. Market participation has broadened compared to earlier in the year, with both large- and small-cap segments contributing to the upside.

Overall, market leadership is rotating back towards US technology, reflecting a more constructive and risk-on mindset, as investors increasingly re-engage with structural growth themes.

Strong earnings season

This renewed focus on growth and earnings momentum naturally shifts attention towards the underlying fundamentals supporting the market, particularly the strength of the current earnings cycle. The earnings backdrop remains strong, supported by solid growth and positive revisions. Notably, 83% of S&P 500 companies that have reported beat earnings estimates, with earnings growth of 23% year-on-year, surprising positively by 18%, according to JP Morgan[7].

Building on these first-quarter results, forward expectations remain supportive. US equities are expected to deliver 12-month forward earnings growth of 22%, highlighting the strength of the current earnings cycle. Information Technology remains the key driver of earnings growth, with significantly stronger dynamics than the broader market[8].

In this context, US equities trade at 22 times 12-month forward price-to-earnings[9], above long-term averages but supported by strong earnings growth. Information Technology appears more expensive in absolute terms, but relative to the five-year average, the sector still compelling, as the recent expansion in earnings has outpaced price performance.

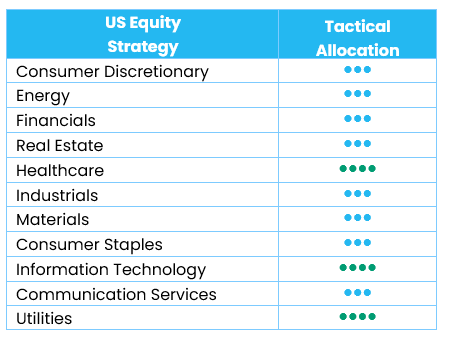

Sub-sector positioning adjustments

We maintain our current sector positioning and remain confident in our core convictions: Healthcare, Utilities and Information Technology.

Healthcare is supported by improved policy visibility, innovation-driven growth and positive relative valuations, particularly within Pharmaceuticals and Biotechnology.

Utilities benefit from strong visibility on demand growth, supported by structural drivers such as electrification and rising AI-related power consumption. Earnings growth is expected to reach the low double digits over the next 12 months, while valuations remain reasonable.

Within Information Technology, structural demand remains robust, especially in hardware and semiconductors linked to AI infrastructure and digital transformation.

Within Financials, we downgraded insurance to -1 from neutral. While first-quarter results were strong, underwriting performance benefited from a favourable catastrophe-loss comparison base, making current profitability levels difficult to sustain. Pricing dynamics in both personal auto and property insurance are starting to soften, while casualty reserve adequacy remains a tail risk given persistent social inflation and litigation pressures. Although higher investment income remains supportive, we do not believe it will be sufficient to offset weakening underwriting discipline. The downgrade of insurance doesn't change our neutral stance on the overall Financial sector.

Emerging equities: Powerful recovery

Emerging market equities staged a powerful recovery in April 2026. The asset class advanced markedly over the month, with benchmark indices not only recouping prior losses but reaching new all-time highs[10], supported by a broad-based resurgence in investor risk appetite and a meaningful improvement in geopolitical expectations.

The primary catalyst for this rebound was a shift in the geopolitical narrative surrounding the Middle East, where the announcement of a temporary ceasefire between the US and Iran significantly reduced near-term tail risks. While no definitive resolution has yet been achieved, the mere re-engagement in high-level diplomatic dialogue was sufficient to prompt markets to price in a higher probability of an eventual normalization in energy flows, particularly through the Strait of Hormuz. This recalibration of geopolitical risk triggered a pronounced risk-on rotation.

Performance within emerging markets was notably concentrated in North Asia, where technology-heavy markets led the rally. Korea and Taiwan delivered strong returns[11], underpinned by robust first-quarter earnings and increasingly optimistic forward guidance across the semiconductor and broader AI supply chain ecosystem. Continued capital expenditure commitments from global hyperscalers reinforced confidence in the durability of the technology cycle, prompting substantial upward revisions to earnings expectations and supporting a re-rating across the sector.

Beyond Asia, gains were more measured but remained positive across most regions. Latin America and CEEMEA markets participated in the recovery to a lesser extent, reflecting a combination of domestic factors and residual sensitivity to commodity price volatility.

For commodities, Brent crude declined by 3.7%. Gold and silver decreased by 1.1% and 1.8% respectively. US yields finished the month at 4.40%[12].

Outlook and drivers

A defining feature in April was the market’s growing ability to look through geopolitical stress. The Iran-related shock initially triggered risk reduction, higher energy prices and a repricing of central bank expectations. The subsequent recovery in EM highlighted underlying resilience, suggesting that investors are increasingly distinguishing between transient macro disruptions and more durable earnings trends. This shift is particularly important for EMs, where sensitivity to global liquidity and external shocks has historically amplified market moves. At the same time, April reinforced the importance of earnings as the primary anchor for performance. Despite heightened uncertainty, 2026 earnings expectations continued to trend higher across regions. This resilience supports the view that underlying demand, particularly in technology, remains intact. Meanwhile, EMs continue to trade at a meaningful discount to developed markets, leaving room for re-rating as macro visibility improves.

The strength of the AI and semiconductor ecosystem remains a central pillar of the EM investment case. Taiwan and Korea remain deeply embedded in the global AI supply chain through semiconductors, memory, foundry capacity and hardware infrastructure. This positions EMs as direct beneficiaries of one of the most powerful secular growth themes globally. AI-related capital expenditure continues to expand, and semiconductor demand remains robust, which can provide a durable earnings anchor.

China has been a stabilising force during the ongoing tensions. In this context, the announced plan for a high-level US visit to China in May takes on particular significance. Any progress towards improving bilateral relations and efforts stabilising the situation in the Middle East could reinforce confidence in China’s external outlook and, by extension, support sentiment across EMs.

Overall, for EMs, the combination of structural growth exposure, cyclical leverage, valuation support and relatively light investor positioning presents a compelling case for reallocation. In an environment defined by geopolitical uncertainty but resilient fundamentals, EMs are not only weathering shocks more effectively, but are gradually positioning themselves as key contributors to a broadening and more balanced global equity cycle.

Positioning update

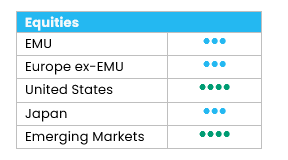

No rating change during the period. Region-wise, we maintain an overweight view on Korea and Taiwan, for the strength of their technology. Sector-wise, we maintain an overweight view on Technology. We are neutral on the Energy and Materials sectors, monitoring potential opportunities.

Regions

Korea: Overweight

We maintain an overweight on Korea, supported by strong positive earnings revisions for key index heavyweights, notably Samsung Electronics and SK Hynix. The revision trajectory remains among the strongest in emerging markets, consistent with Korea’s leverage to memory and broader semiconductor dynamics.

Taiwan: Overweight

We keep Taiwan overweight on the back of sustained earnings momentum in the technology complex. Taiwan remains central to the global semiconductor supply chain, and its index composition is strongly geared toward tech, making it a direct beneficiary of positive revision cycles and supportive industry demand.

China: Neutral

We remain neutral on China as earnings revisions continue to lag, and valuations sit broadly in line with historical averages. Within China, our preference remains skewed towards onshore exposure (A shares) rather than Hong Kong listings, as it offers relatively higher technology representation and typically greater sensitivity to domestic policy support. Geopolitically, the Trump–Xi meeting appears to have reduced near-term tail risks and supports the view that the peak in bilateral tensions may be behind us. Structural competition is expected to persist over the long run, which reinforces the need to stay selective and disciplined.

India: Neutral

We stay neutral on India as the market has underperformed, yet valuations remain above historical averages, leaving less valuation support at a time when earnings momentum has softened. We continue to recognise the durability of India’s long-term structural story. Short-term risks include still-stretched valuations, geopolitical noise and the uncertainty around global tariff dynamics, which could affect sentiment and external-facing sectors.

Sectors

Energy: Neutral

We remain neutral on Energy overall, with a more constructive posture in standard strategy, while waiting for greater visibility on the path towards normalisation around Hormuz-related risks. The sector’s near-term direction remains highly sensitive to geopolitical outcomes and crude price volatility, which argues for patience and selectivity rather than an outright directional call. In our ESG strategy, we continue to emphasise renewables exposure, seeing the growing demand for energy diversification.

Materials: Neutral

We hold Materials at neutral, balancing supportive structural demand for certain metals against headwinds from a strong dollar and heavy investor positioning, particularly in precious metals. Within the space, we continue to identify selective opportunities in industrial and energy transition-linked metals such as aluminium, copper and nickel, where idiosyncratic supply-demand dynamics can still create attractive setups.

Retailing: Overweight

We keep Consumer Discretionary neutral at sector level, but maintain an overweight in retailing, which is dominated by China exposure and trades at comparatively low valuation levels. The investment case is supported by more rational competitive behaviour, which could unlock better profitability and a potential re-rating. However, we acknowledge that this process may take time to materialise.

Technology: Overweight

We maintain an overweight in Technology, supported by strong earnings revisions and a constructive news flow across the supply chain. Technology continues to offer the clearest combination of earnings momentum and thematic durability within emerging markets, and it is reinforced by our regional overweight in Korea and Taiwan, where the revision cycle remains particularly supportive.

[1] Source: Eurostat, April 2026

[2] : Sources: MSCI IT: +24.5% YTD (vs +28.7% for MSCI Energy) – 30 April 2026

[3] All performances relate to the MSCI Europe Index and its sub-segments – 30 April 2026

[4] Source: Bloomberg - 8 May 2026

[5] Source: Bloomberg - 8 May 2026

[6] Source: Bloomberg - 8 May 2026

[7] Source: JP Morgan – 1 May 2026

[8] Source: Bloomberg - 8 May 2026

[9] Source: Bloomberg - 8 May 2026

[10] Source: MSCI Emerging Markets Index (Net Return): +12.67% - April 2026

[11] Sources: MSCI Korea: +38.2% and MSCI Taiwan: +26.2%

[12] Source: Bloomberg as of 1st May 2026.