As the percentage of vaccinated people keeps increasing, we are getting closer to a return to our normal previous lives, or something close to it. Investors are keeping their ears close to the rail line coming from the Fed and closely monitoring the smoke signals from Washington to gain a better grasp of inflation expectations, which, for most of the investing community and business operators, is only a theoretical concept to be found in history books.

Equity market performances were dispersed during the month. Emerging markets, Southern Europe and commodity producers such as Canada and Norway outperformed, while technology, biotechnology and Taiwanese equities were among the worst performers. In the US, materials, energy and financials outperformed consumer discretionary and technology in a context where recovery and inflation took the higher ground.

Inflation expectations led mid-to-long-term Treasuries to tighten by around 0.10% during the first half of the month. Yields eased back to early-month levels following dovish statements by the Fed. While fixed income remained relatively calm, moves were stronger for the US dollar, which decreased in value by 1% to 3% versus the Real, the Mexican peso, the Rupee and the Renminbi, to name but a few. Precious and industrial metals were among the best-performing commodity futures.

The HFRX Global Hedge Fund EUR returned +0.31% during the month.

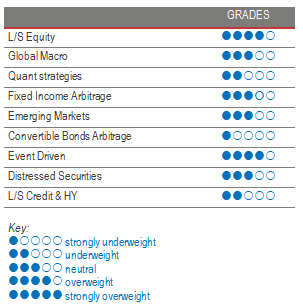

Long Short Equity

On average, Long-Short Equity indices were positive for the month, although there was a fair amount of dispersion across styles. Value-bias strategies outperformed managers focusing on growth. Sector specialists in technology and biotechnology, areas with a high representation of growth names at high multiples, were among the most challenged strategies during the month. Generalists, who do not want to take a firm stand on the Growth-versus-Value debate, have adopted a rather barbell positioning, not only buying good-value businesses that are benefiting from the recovery, but also selectively buying growth-business models whose share price has underperformed the market since the beginning of the year. Gross and net exposure levels remain relatively stable for the moment. Long Short Equity is a strategy that is diverse and rich in terms of thematics and style, and possesses several tools to face different market environments.

Global Macro

Across macro strategies, although performance was dispersed, it tilted towards a positive average. As the big market moves associated with the recovery have largely played out, investment risk levels have come down and managers are now focusing rather on relative-value trades and expect more modest directional-price changes. This type of market environment, less beneficial to directional discretionary macro managers, levelled the field with systematic macro strategies. Long positions on commodities and Emerging Market currencies versus the Dollar were additive to performance. Performance generation on equity indices was more challenging, due to short market moves. Developed Market fixed income had a muted performance contribution, trading range-bound and looking for a direction as the markets attempted to forecast the direction of rates. We continue to favour discretionary opportunistic managers who can draw on their analytical skills and experience to generate profits from selective opportunities worldwide.

Quant strategies

May was another strong month for Quantitative Strategies. Trend models contributed to performance, driving returns mainly from long positions in commodities and equity indices. Statistical arbitrage strategies were, on average, also additive to performance, generating positive returns across the different factors. Sophisticated Multi-Strategy funds continue to be better positioned to navigate different market environments and post interesting returns, as they are less dependent on any specific model.

Fixed Income Arbitrage

Despite 10-year US rates plateauing around 1.60%, the healthy dynamic for basis trading was overshadowed by (a) technical aspects (temporary exclusion of Treasuries from the Supplementary Leverage Ratio (SLR) calculation), (b) some profit-taking on steepeners and (c) the directional positioning. On the European side, the ongoing market dynamics supported good P&L generation. Going forward, the environment will be driven by technicals, central bank intervention and inflation uncertainty (while the reopening is gaining momentum), which could all weigh on the strategy, despite a healthier environment. The main difference compared to April is that, despite the odds increasing about the inflation outcome, interest-rate volatility is dropping.

Emerging markets

May was a strong month for Emerging Market managers. The recovery narrative and an increasingly balanced positioning between cyclicals and the digital economy was supportive of riskier assets. Emerging Markets fixed income, an appealing asset class to investors by the higher yields they offer versus other regions, was supported by range-bound trading in Developed Market sovereign fixed income, more specifically in US Treasuries. Emerging Market currencies also benefited from a strong market for commodities and a declining dollar. China equities, a strong performer last year partially due to a relatively quick recovery from the COVID crisis, have remained relatively muted this year. The crackdown by the central government on some large companies and tighter monetary management by the People’s Bank of China have helped take some of the steam out of the system. Emerging Markets are an appealing investing ground for investors seeking decent-yielding fixed income assets. Although EM fundamental managers reckon the space is an interesting option in a zero-rate world, considering the fragility of fundamentals, they usually adopt a very selective approach. Caution is required, due to the higher sensitivity of the asset class to investor flows and liquidity.

Risk arbitrage – Event-driven

Event Driven strategies continued to perform well during May and have among the best risk-adjusted returns since the beginning of the year. Deal volumes remain healthy and average deal spreads present an interesting low double-digit annualized return. Managers believe this may be one of the most interesting strategies for 2021, as the equity markets might have priced in most of the recovery and periods of higher volatility may lie ahead as the market juggles with two contradictory forces: optimism for the future, on the one hand, and some good level of bubbles in the market (fed by generous liquidity injections), on the other. Merger-deal activity is expected to continue in the near future. Interest rates, although rising, remain low in absolute terms, corporations have cut costs and issued debt and equity not only to face the crisis, but also to be ready to snap up strategic assets. The activity is driven by the need to restructure in stressed sectors like energy and travel, the willingness for consolidation in healthcare, financials and telecom, and the need to adapt to today’s new reality by externally acquiring technologies that would take too much time or money to develop, like in the semiconductor space.

Distressed

Stressed and distressed strategies did well during the month, benefiting from idiosyncratic profitable trades and a positive risk-on sentiment. The last 12 months have been, on average, the highest performance period since the Great Financial Crisis (GFC) of 2008. The COVID crisis, managers believe, although very different by its origins and its impact, will be a source of opportunity for years to come. During the GFC, the market dealt with a financing crisis following the collapse of major financial institutions; the current financial landscape is characterized by relatively sound financial institutions but where bank financing, by force of regulation, has been replaced by support from non-banking financial institutions like hedge funds. The opportunity-set is hence wide and varied. We favour experienced and diversified strategies to avoid having to face extreme volatility swings. It is not going to be easy but this is the environment and opportunity-set these managers have been waiting on for the last decade.

Long short credit & High yield

Following the market crash at the end of the first quarter of 2020, hedge funds have opportunistically loaded on IG and HY credit at very wide spreads. Managers that were able to go into offensive mode were aggressively buying on the market or making off-the-market block trades, whereas other managers, unable to meet margin calls, needed to quickly cut risk. Since then, spreads have completely reversed to pre-COVID levels. Multi-strategy managers have significantly reduced exposure to credit and high yield, as current valuations present limited expected gains and a negative risk-return asymmetry.