April was dominated by the interaction between resilient global activity and a renewed energy shock linked to the Middle East conflict and impaired traffic through the Strait of Hormuz. Global manufacturing PMIs improved across several developed and emerging economies, but the IMF and OECD trimmed 2026 growth forecasts and highlighted downside scenarios. In the US, private domestic demand remained firm, supported by AI-related investment, while consumption resilience increasingly relied on a lower saving rate and faced pressure from tariffs, slower income growth and higher gasoline prices. In the eurozone, the energy shock was already visible in softer activity, weaker services and declining consumer confidence, although manufacturing held up partly because of front-loading. China’s early-2026 rebound remained uneven, led by exports and financial services rather than domestic demand.

Risk assets recovered strongly during the month led by Korean, Japanese and US equities and AI-related sectors. US Technology indices recorded one of its best months since 2002, while US earnings’ results were notably resilient with strong beat rates and positive revisions supporting broader equity sentiment. European equities lagged, reflecting weaker macro surprises. Energy and defensive sectors such as healthcare, staples and utilities underperformed during the month technology, consumer discretionary, industrials and financials. Hedge funds reduced gross exposure to global equities, particularly in the US, while still participating in crowded long-short winners. The Momentum Equity Long Short spread had one of its highest monthly returns ever. US and European sovereign yields stabilized after increasing by 30 to 40 bps[2] at the back end of the curve. The Euro 10-year trades at around 3% while American issues ended the month of April at around 4.31%[3]. Corporate credit rallied significantly with the risk-on move.

The HFRX Global Hedge Fund EUR Index was up +2.72% over the month.

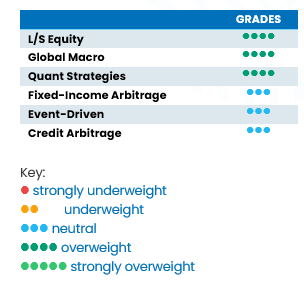

L/S Equity

April was a strong recovery month for long-short equities, led by the rebound in US technology, AI beneficiaries and earnings momentum. HFRX Equity Hedge gained +5.43%, with fundamental growth up +8.74% and value up +4.16%. Managers benefited from stronger US earnings, a double-digit positive return for Nasdaq and renewed appetite for AI-capex exposed names. Positioning was not aggressively risk-on: Morgan Stanley Prime Broker data showed hedge funds reducing global gross exposure and later trimming AI beneficiaries despite positive performance. The near-term outlook remains constructive for stock-pickers but crowding in semiconductors and sensitivity to energy-driven macro shocks argue for disciplined net exposure. Long-Short Equity strategies are well positioned to be beneficiaries of increased dispersion across sectors offering a supportive backdrop for active stock selection.

Global Macro

Global macro recovered in April after March’s energy and rates shock. Macro indices gained low single-digits, driven mainly by systematic trend-following, while dollar weakness and mixed commodity move created cross-asset opportunities. The macro backdrop was still complex: oil remained elevated due to impaired Hormuz traffic, the Fed signalled patience, and the ECB moved closer to a potential hike as energy inflation rose. Positioning likely shifted from March’s defensive posture toward more selective FX, rates and commodity trades. The outlook is positive for nimble managers, as policy divergence, geopolitics and energy volatility should keep dispersion high.

Quant Strategies

Quantitative strategies were generally positive, helped by stronger trend signals, equity momentum, and high single-name dispersion. On average, Quantitative Directional significantly outperformed returning mid to high single-digit positive returns, while equity market neutral returns were more muted. This seems to indicate that directional and trend models benefited more than pure factor-neutral approaches. Positioning stayed systematic but likely leaned into equity momentum, weaker dollar trends and AI-related leadership. Morgan Stanley noted dispersion across S&P 500 names remained elevated, supporting alpha opportunities. The outlook remains favourable if volatility stays orderly, and dispersion persists, but factor reversals remain the main risk.

Fixed Income

Fixed-income arbitrage and relative-value strategies benefited from calmer rates markets after March’s volatility. On average, strategies were up low single digits. Performance drivers included stabilizing government yields, tighter risk premia and better liquidity conditions. Managers likely maintained moderate leverage, focusing on curve, swap-spread and cross-market relative-value trades rather than large duration bets. The outlook is selective: policy uncertainty remains high, with the Fed expected to stay patient and the ECB considering hikes, but stable yield ranges should support carry and convergence trades if funding conditions remain contained.

Event Driven

Event-driven strategies participated in the April rebound but as expected, more moderately than equity hedge strategies. Special situations strategies outperformed pure merger arbitrage due to their higher levels of directionality. Equity market strength, improving sentiment and continued M&A activity helped spreads, while stronger earnings supported catalyst-driven equities. Positioning likely remained selective, with managers favouring announced deals, balance-sheet strength and idiosyncratic catalysts over highly levered or macro-sensitive situations. The short-term outlook is balanced: volatility creates entry points, but geopolitical risk might limit upside. However, for the longer-term, the opportunity set is expected to improve with more deals coming to market contributing spreads to stabilize.

Credit Arbitrage

Credit arbitrage was resilient in April as risk appetite improved and yield demand supported spreads. Performance was driven by carry, security selection and better liquidity rather than broad spread compression. Positioning likely favoured higher-quality credit, liquid relative value and selective shorts in vulnerable sectors. The outlook is cautiously constructive, but elevated issuance, AI-related financing needs and private-credit weakness argue against excessive spread beta.

[1] Reference to Morgan Stanley US Momentum: MSZZMOMO

[2] Source: Factset – 30.04.2026

[3] Source: Factset – 30.04.2026