Last week in a nutshell

- In the US, long-term inflation expectations declined while consumer sentiment improved to its highest reading since mid-2021.

- In the euro zone too, consumers seemed increasingly confident as employment expectations remained essentially stable.

- Britain's economy slipped into a mild recession last year, prompting PM Rishi Sunak to reassure voters before the next general election.

- Senior Japanese policymakers fuelled expectations of currency intervention after the Japanese yen fell to a 34-low against the US dollar.

What’s next?

- Investors will focus on preliminary inflation data for March in the euro zone. Ongoing disinflation and positive surprises on economic growth, a goldilocks environment may emerge.

- Manufacturing and services PMIs will put the level of activity in developed vs developing countries back in the spotlight.

- In the US, the highlight will be the US job report, with ISM indices also released.

- The Reserve Bank of India will meet. With inflation near the upper band of the 2%-6% target, a rate cut is not expected.

Investment convictions

Core scenario

- Supported by central banks’ rhetoric on pending rate cuts, the goldilocks environment characterised by positive growth surprises and negative inflation surprises is spilling into the euro zone.

- A soft-landing/ongoing disinflation scenario in the United States remains our most likely scenario, implying no rush for the Fed to deliver monetary support. We expect the first monetary easing in June.

- 2024 should bring better visibility with a narrowing economic growth gap between countries while most central banks have restored room for manoeuvre.

- In China, economic activity has shown some fragile signs of stabilisation while the evolution of prices remain deflationary.

Risks

- Geopolitical risks to the outlook for global growth remain tilted to the downside as developments in the Red Sea unfold and the war in Ukraine continues. An upward reversal in the price of Oil, US yields or the US dollar are key variables to watch.

- A risk would be a stickier inflation path than expected which could force central banks to reverse dovish rhetoric. In our understanding, it would take more than just the bumpy data registered at the start of the year.

- Beyond commercial real estate exposures, financial stability risks could return as a result of the steepest monetary tightening of the past four decades.

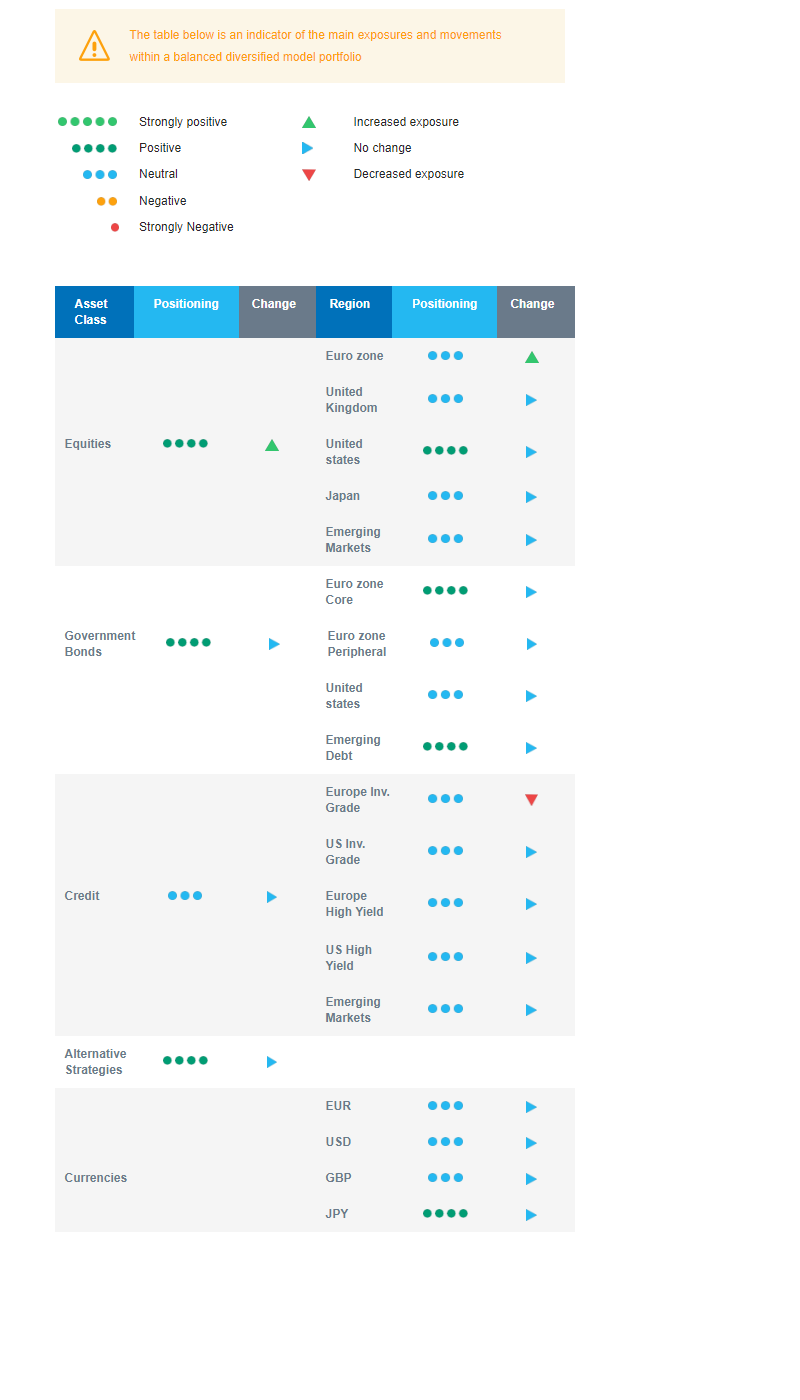

Cross asset strategy

- Our strategy increasingly reflects the latest development on the euro zone: economic surprises are now positive as sentiment and flows may have turned a corner. Investor interest seems to be on the mend, and with a broadly attractive risk premium, the potential for a catch up by laggards is increasing. We are willing to add some beta and cyclicity to the strategy to benefit from increasingly supportive central banks rhetoric on pending rate cuts.

- We have the following investment convictions:

- Our equity allocation has become slightly overweight, via a more constructive view on the euro zone equity market.

- In addition, we remain buyers of Health Care. We have been looking for opportunities in beaten down stocks in small and mid-caps and are now starting to add in this segment.

- In the fixed income allocation:

- We have a positive stance on European duration and aim for the carry in a context of cooling inflation.

- We remain exposed to emerging countries’ debt to benefit from the attractive carry.

- We maintain a neutral stance on US government bonds, looking for a new, more attractive, entry point.

- We downgrade our views on European Investment Grade credit to make room for the added beta on the equities side.

- We hold a long position in the Japanese Yen and have exposure to some commodities, including gold, as both are good hedges in a risk-off environment.

- We expect Alternative investments to perform well as they present some decorrelation from traditional assets.

Our Positioning

In our opinion, it is time to add some beta and cyclicity to the portfolio to benefit from a broadening of the goldilocks environment. In Europe in particular, economic surprises are now positive, leading to improving sentiment and flows. We note that investor interest is returning somewhat, and with the risk premium attractive overall, laggards could perform better in a context of economic improvement. We were reassured by the central bank meetings in March and think that the expected upcoming central bank rate cuts are an additional element which should act as support while capping long-term bond yields, underpinning our positive view on duration. We keep a supportive stance on US equities and are neutral on Europe, Japan and Emerging markets. We also continue to harvest carry via Emerging Market debt.