Bond markets are pricing the war in Iran. Equity markets are not. That divergence has become a defining feature in the past month. The conflict has now moved beyond the initial shock phase and has entered a regime of repeated escalation, partial de-escalation and unresolved disruption. Oil prices remain elevated, shipping lanes are still disrupted and inflation expectations have moved higher. Yet equities have largely recovered from the initial shock and are no longer reacting mechanically to every geopolitical headline, but require more evidence of macro transmission before possibly repricing risk.

So far, the evidence remains mixed. Bond markets have incorporated higher inflation risk and reduced policy flexibility. Commodity markets continue to reflect supply uncertainty. Equity markets, however, are still anchored by corporate fundamentals, especially in areas where earnings visibility remains strong. This does not mean the shock is benign. It means that the market’s threshold for concern has changed.

Earnings against the noise

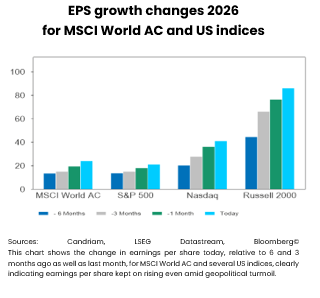

The return of the earnings season has reinforced this shift back towards fundamentals. Q1 has delivered constructive results and guidance, with upward earnings revisions led by Technology, Energy and Basic Materials. In practice, markets are rewarding visibility rather than narratives. Companies able to demonstrate resilient demand, pricing power and cash-flow generation are being treated very differently from those whose long-term models are becoming less certain.

Nowhere is this clearer than in Technology, and more specifically, AI infrastructure. With more than $700bn expected to be invested by hyperscalers in AI infrastructure in 2026, the ecosystem continues to benefit from exceptionally strong demand visibility. Order books remain full, production capacity remains constrained, while earnings revisions are positive and even continue to move higher. Investors increasingly trust tangible infrastructure economics over geopolitical speculation and headline manipulation.

At the same time, the divide within Technology is becoming sharper. The market is no longer treating the sector as a homogeneous growth asset. Infrastructure continues to attract capital; parts of software and IT services are much less doing so. The emergence of increasingly capable AI agents has triggered a reassessment of SaaS and outsourcing business models, particularly where automation threatens pricing power and long-term margins. This explains much of the sector’s relative underperformance this year.

This repricing, however, is becoming more selective. Not all software companies are equally exposed to these risks. Companies linked to cybersecurity, data protection, storage, mission-critical infrastructure and processing appear structurally better positioned, as their products are less easily displaced and may even become more important in a more AI-intensive environment. The market is therefore distinguishing between the companies enabling the AI cycle and those whose business models may be disrupted by it.

Another tension is building beneath the surface. Potential IPOs from major players could mobilise several trillions of US dollars in capital during the second half of the year. Even if issuance is staggered over time, it would absorb liquidity and intensify competition for investor allocation precisely as parts of the software ecosystem are already facing multiple compression.

This helps explain the broader market behaviour. Investors are increasingly distinguishing between geopolitical noise and observable earnings delivery. So far, the latter still dominates.

When does the shock become macro?

The market reaction function has changed. Investors are no longer reacting to the existence of the shock itself, but to its ability to alter economic behaviour.

The conflict has lasted for more than 80 days. A ceasefire has been announced, but no durable agreement has been reached, and the Strait of Hormuz remains only partially functional. Yet despite elevated oil prices and continued disruption to shipping traffic, equities have stabilised and earnings expectations remain broadly intact.

Markets increasingly treat the conflict as a persistent cost rather than an immediate systemic event. The key question is no longer whether escalation occurs, but whether higher energy prices become restrictive enough to impair earnings, investment intentions or policy flexibility. That is the point at which the geopolitical shock might turn into a macro shock.

So far, the macro transmission remains only partial. Energy prices have lifted inflation expectations and pushed bond yields higher, tightening financial conditions. Yet, the deterioration in activity data remains limited, particularly in the US. Corporate earnings guidance has also remained relatively resilient, particularly in sectors benefiting from visible investment cycles. That does not mean the shock is benign. It means markets are demanding harder evidence before repricing lower.

At the same time, the risk has become structurally broader. Damage to Saudi and Qatari infrastructure confirms that the conflict is no longer contained to Iran. Pressure is increasingly visible across other commodities where supply is now being constrained: fertilisers, sulphur and agricultural commodities. This is widening the inflation impulse beyond oil alone. Our base case nevertheless remains one of gradual normalisation rather than renewed escalation. Traffic through Hormuz is expected to recover progressively, allowing oil prices to move back towards USD 75 per barrel by year-end. This would ease inflationary pressure, support risk sentiment and give central banks more room to continue normalising policy. The principal risk remains a slower normalisation scenario in which oil prices stay above USD 100 into 2027. In that case, the shock would become more persistent, more inflationary and more damaging for growth.

Oil inventories can buy time, but they cannot fully offset a sustained disruption. The April configuration showed that re-routing flows from Saudi Arabia and the UAE, combined with strategic reserve releases and commercial stocks, could absorb a large share of lost Iranian exports. By end-May, however, the gap will widen despite similar mitigation efforts: re-routing capacity is plateauing while reliance on inventories is increasing, leaving a more visible residual deficit. Ultimately, only a normalisation of traffic through the Strait of Hormuz can restore balance to global oil supply.

Regional fault lines

The regional consequences are becoming increasingly asymmetric. The United States continues to appear relatively more insulated. Domestic energy production reduces its direct vulnerability to Middle Eastern supply disruptions, while stronger earnings visibility, particularly in AI-related sectors, continues to support equity resilience. Deeper capital markets, stronger balance sheets and the dominance of companies linked to the current investment cycle also help explain why US equities have been more robust.

Europe remains the most exposed developed region. Its dependence on imported energy makes the shock more directly relevant for inflation, margins and growth. Higher energy prices directly tighten financial conditions in an economy where growth momentum was already modest. They also weigh on household purchasing power and on industrial competitiveness. Japan faces similar vulnerabilities through imported energy and yen weakness, both of which amplify inflation pressure.

Emerging markets present a more differentiated picture. Higher imported energy costs, weaker trade and tighter financial conditions remain headwinds, particularly for energy importers. At the same time, selective opportunities persist in economies benefiting from commodity exposure, carry or structural investment flows linked to the AI cycle.

Policy: constrained, not paralysed

Central banks are increasingly constrained. The Federal Reserve is unlikely to react to short-term energy volatility, but further easing now depends on whether higher oil prices feed durably into inflation expectations. The ECB faces a more difficult trade-off given Europe’s direct exposure to imported energy. Meanwhile, the Bank of Japan and the Reserve Bank of Australia remain in tightening mode, reinforcing policy divergence across regions.

The key point is that central banks are no longer reacting primarily to domestic cycles. External energy shocks increasingly shape policy paths and limit room for manoeuvre.

Selective re-risking

Against this backdrop, we have modestly increased risk exposure again, but selectively.

On equities, we upgraded our overall stance to slight overweight, primarily through the United States and Emerging Markets. We upgrade the US because it continues to benefit from stronger earnings visibility and relative energy insulation. Earnings revisions are not only strong, they keep improving even with the ongoing conflict. The main sectors driving EPS growth are Tech, Energy and Materials. Currently, we put our emphasis on the sector with the strongest upward EPS revisions: Technology.

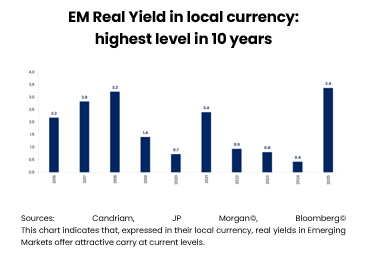

We also upgrade Emerging Markets since here, a similar story is unfolding. Notably Korea and Taiwan offer relatively cheap exposure to the AI cycle.

At the same time, we remain neutral on Europe and Japan, where sensitivity to energy prices remains materially higher. Furthermore, neither region offers a large exposure to AI developments.

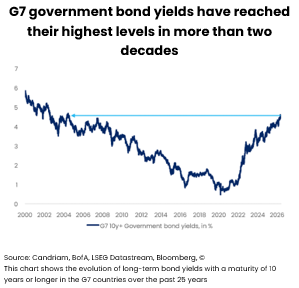

In fixed income, our adjustments also reflect selectivity rather than broad directional conviction. We upgrade exposure to high-quality German government bonds, where AAA quality and liquidity provide resilience in a more uncertain environment, increasing our duration slightly. We also upgrade Emerging Market local currency debt, supported by attractive carry and diversification benefits. Yes, spreads are tight, but real yields are at decade highs, offering an attractive risk/reward proposition. IG credit and HY still require discipline. Spreads remain relatively tight and markets continue to reward quality and visibility over beta.

Managing instability

The defining feature of the current regime is not geopolitical volatility itself, but the market’s changing threshold for concern.

Markets increasingly require evidence that geopolitical stress materially alters earnings, inflation or policy trajectories before repricing risk assets lower. As long as AI capex remains strong, earnings revisions positive and financial conditions manageable, equities can remain supported despite geopolitical instability.

That does not eliminate risk. It changes the conditions under which markets react. In our view, the coming months will depend less on headlines themselves than on whether those headlines begin to alter corporate behaviour, consumer confidence and central bank policy. Until then, managing instability – not predicting the next escalation – remains the central investment challenge.

Candriam House View & Convictions

The table below is an indicator of the main exposures and movements within a balanced diversified model portfolio.

Legend

-

Strongly Positive

-

Positive

-

Neutral

-

Negative

- Strongly Negative

- No Change

- Decreased Exposure

- Increased Exposure

| Current view | Change | |

|---|---|---|

| Global Equities |

|

|

| United States |

|

|

| EMU |

|

|

| Europe ex-EMU |

|

|

| Japan |

|

|

| Emerging Markets |

|

|

| Bonds |

|

|

| Europe |

|

|

| Core Europe |

|

|

| Peripheral Europe |

|

|

| Europe Investment Grade |

|

|

| Europe High Yield |

|

|

| United States |

|

|

| United States |

|

|

| United States IG |

|

|

| United States HY |

|

|

| Emerging Markets |

|

|

| Government Debt HC |

|

|

| Government Debt LC |

|

|

| Currencies |

|

|

| EUR |

|

|

| USD |

|

|

| GBP |

|

|

| AUD/CAD/NOK |

|

|

| JPY |

|

Monthly Coffee Break

Updated each month, this section provides expert analysis and strategic insights. Stay informed with our latest market perspectives and allocations.

-

Monthly Coffee Break, Alternative Investments

Monthly Coffee Break, Alternative InvestmentsAI Cooled, Alternatives Ruled

June was marked by resilient but narrower global growth, still-elevated price pressures and a renewed focus on energy risk. Global PMIs remained consistent with expansion, but supply-chain tensions and geopolitical uncertainty persisted after the partial reopening of the Strait of Hormuz. -

Monthly Coffee Break, Asset Allocation

Monthly Coffee Break, Asset AllocationKeep calm and carry on

The global cycle is still catching its breath. World PMI edged up only marginally in June, still consistent with instant growth close to 2.5% in Q2. -

Monthly Coffee Break, Fixed Income

Monthly Coffee Break, Fixed IncomePositive on euro investment grade

We move US nominal duration back to neutral after the front-end overweight implemented last month. The main reason is the first FOMC meeting under Kevin Warsh and the market reaction that followed. -

Monthly Coffee Break, Equities

Monthly Coffee Break, EquitiesSector leadership is broadening beyond technology

Since the last equity committee in June, European equities have continued to advance, surpassing historic levels at the end of June, following the signing of the Memorandum of Understanding (MoU) between the United States and Iran.