June was marked by resilient but narrower global growth, still-elevated price pressures and a renewed focus on energy risk. Global PMIs remained consistent with expansion, but supply-chain tensions and geopolitical uncertainty persisted after the partial reopening of the Strait of Hormuz. In the eurozone, the energy shock began to fade as oil prices receded, supporting a gradual improvement in PMIs, especially services, although growth indicators still pointed to only moderate Q2 activity. The ECB raised rates by 25 bps in June, citing Middle East-related inflation pressures and its 2% target mandate. In the US, domestic demand remained resilient but increasingly dependent on AI-related investment, while consumption was constrained by stagnant real disposable income. China’s activity softened in Q2, with weak domestic demand and property investment only partly offset by high-tech manufacturing and AI-linked exports.

Risk assets diverged sharply in June. European equities outperformed the US. Japan was strong, while China/Hong Kong was mixed. Sector performance showed a clear rotation: European IT, financials and utilities rose while European energy and telecoms fell. In commodities, energy reversed sharply; precious metals also weakened, with gold and silver down heavily. Overall, credit markets remained resilient, supported by steady equity risk appetite, lower oil prices into month-end and no material deterioration in default risk pricing.

The HFRX Global Hedge Fund EUR Index was up 0.49% over the month.

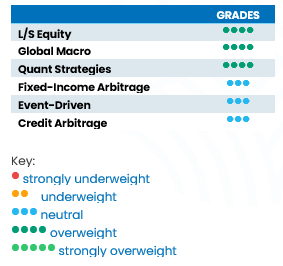

L/S Equity

Long-short equity strategies generally benefited from strong dispersion and sector rotation in June. HFR reported Equity Hedge up 1.70%, supported by fundamental growth, value and market-neutral strategies. Morgan Stanley Prime Brokerage data showed hedge funds continued to reduce crowded AI/technology winners, especially AI beneficiaries and tech hardware, while buying selected software, discretionary and industrial names. Americas L/S funds gained 2.4% in June, while Europe-based L/S funds were weaker, down 0.4%. The short-term outlook remains constructive but more selective, with alpha likely driven by earnings dispersion rather than broad beta.

Global Macro

Global macro strategies had a difficult June, as several major asset trends reversed or became less directional. HFR reported Macro down 0.9%, with systematic macro particularly weak, losing 1.4%. The main performance drag came from sharp commodity reversals, notably the fall in Brent and WTI, alongside weakness in precious metals and renewed US dollar strength. Discretionary macro managers found better opportunities in relative-rate and FX trades, but broad directional conviction was harder to sustain, as markets reassessed inflation, central bank timing and geopolitical risk. The outlook remains mixed: higher cross-asset volatility creates opportunities, but macro funds may need more persistent trends in rates, currencies or commodities to rebuild momentum.

Quant Strategies

Quantitative strategies were supported by a market environment characterised by elevated dispersion, lower correlations and sharp factor rotation. Equity market-neutral approaches performed well, with HFRX Equity Market Neutral up 1.8%, as stock-specific moves and sector dispersion created a favourable backdrop for statistical arbitrage, factor and relative-value models. Momentum signals were more challenged late in the month, as crowded AI and technology winners were reduced, while capital rotated towards healthcare, financials, industrials and selected software. CTA and systematic macro strategies were more mixed, with several established trends in commodities and FX reversing during June, but the environment still offered opportunities for models able to adapt across time horizons. Looking ahead, dispersion should remain supportive for Equity Quant strategies, while trend strategies may depend on clearer direction in rates, currencies and commodities.

Fixed Income

Fixed income arbitrage and relative-value strategies were modestly positive. HFRX Relative Value rose 0.30%, supported by a rate environment where short-dated interest rates rose and longer-dated yields were broadly stable. This backdrop favoured curve, carry and financing-sensitive trades, although volatility around central bank expectations remained a constraint. The short-term outlook is constructive for relative-value carry, but leverage discipline remains important as policy uncertainty persists.

Event Driven

Event-driven strategies were positive but uneven. HFRX Event Driven gained 0.6%, driven by special situations, while merger arbitrage declined 0.4% as deal spreads faced mixed equity markets and execution uncertainty. The broader backdrop was supportive: equities remained resilient outside crowded US technology, and capital market activity improved, with stronger M&A and IPO conditions. However, geopolitical risk and shifting rate expectations kept managers selective. The outlook is cautiously positive, particularly for special situations and balance sheet catalysts, while merger arbitrage remains dependent on regulatory clarity and financing conditions.

Credit Arbitrage

Credit arbitrage strategies benefited from stable risk appetite and contained spread volatility. HFRX Relative Value’s positive return and gains in convertible arbitrage suggest supportive conditions for spread, carry and volatility-sensitive credit trades. The near-term outlook is balanced: carry remains attractive, but tight spreads leave less cushion if growth slows, oil volatility returns or refinancing conditions deteriorate.

Performance data source: HFR (or other relevant source used). Past performance of a given financial instrument or index or an investment service or strategy does not predict future returns.