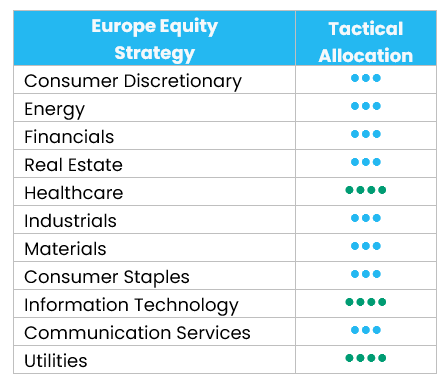

European equities: New All-Time highs

Since the last equity committee in June, European equities have continued to advance, surpassing historic levels at the end of June, following the signing of the Memorandum of Understanding (MoU) between the United States and Iran. Investors gained further confidence from a softening macroeconomic environment, supported by lower-than-expected eurozone inflation and balanced economic commentary from the European Central Bank (ECB).

Since the last equity committee in June, European equities have continued to advance, surpassing historic levels at the end of June, following the signing of the Memorandum of Understanding (MoU) between the United States and Iran. Investors gained further confidence from a softening macroeconomic environment, supported by lower-than-expected eurozone inflation and balanced economic commentary from the European Central Bank (ECB).

Wide sector performance dispersion

Beyond this broad European market improvement, gains were concentrated in some sectors (financials, real estate, industrials, consumer staples and healthcare), while others remained flat (information technology, materials) or landed in negative territory (energy, communication services).

Financials outperformed during the period thanks to the ECB's 25 basis point rate hike, which is expected to boost bank profitability. Within cyclical sectors, real estate and industrials also performed well as both of them benefited from geopolitical relief and an improved macroeconomic outlook. Consumer discretionary posted more modest gains, as European automakers suffered from BMW’s unexpected profit warning. Meanwhile, materials remained broadly flat, as the reopening of the Strait of Hormuz triggered a downward correction in the valuations of bulk material, chemical and mining stocks.

Most defensive sectors also landed in positive territory[1], with the exception of energy which was weighed down by a sharp drop in crude oil prices. Utilities proved more resilient due to an intense early summer heatwave that triggered a surge in short-term power prices and energy demand across the continent. Consumer staples and healthcare were the best-performing defensive sectors, beginning to benefit from a rotation as capital started to shift away from technology stocks[2].

Information technology as a whole remained flat during the period, showcasing the same divergence seen in previous months: semiconductors still benefited from the AI theme, while software continued to suffer from AI disruption risks. Lastly, communication services were down on technological disruption fears, prompted by SpaceX’s IPO.

In terms of market capitalisation, large caps outperformed small caps, buoyed by the strong performance of banks, semiconductors and aerospace & defence stocks.

Positive earnings revisions and higher valuation multiples

European earnings revisions remain well oriented, with 53% of MSCI Europe constituents seeing upward revisions to next fiscal year earnings estimates over one month[3]. Earnings revisions were strongest in industrials, consumer staples and energy.

European equities are expected to deliver 12-month forward earnings per share growth of 11%, according to Bloomberg data on 6 July 2026. EPS growth is expected to be highest in the energy sector (+45%), followed by materials (+28%), information technology (+23%) and consumer discretionary (+22%). Conversely, financials and consumer staples are expected to deliver the most limited EPS growth, at +1% and +2%, respectively[4].

Since the last equity committee, European valuation multiples have increased, with the 12-month forward P/E ratio now standing at 15.6x (vs 15.0x before). Information technology and industrials remain the most expensive sectors, trading at 32.7x and 23.0x, respectively, while energy and financials remaining the cheapest, at 8.2x and 11.6x, respectively, according to Bloomberg data on 6 July 2026.

European communication services downgraded to neutral

We decided to downgrade European telecom services (Level 2) to neutral from +1 for the following reasons:

- After a record year in 2025, European telecoms have delivered a more mixed YTD performance, while still playing their defensive role during the period of geopolitical tension.

- With the US-Iran de-escalation process progressing, particularly after the preliminary MoU signed in mid-June, we see the sector increasingly as a source of funding for more cyclical areas.

- SpaceX's IPO on June 12 has also triggered renewed news flow around Starlink's ambitions in telecoms. While we do not expect satellite communication to replace terrestrial mobile networks, given technical and economic constraints, it is likely to become a complementary service and could weigh on sector sentiment through the perception of rising competition.

We also downgraded European communication services (Level 1) to neutral from +1 as Telecom Services account for 68% of the European Communication Services sector[5].

We maintain our positive stance on European technology, as we remain fundamentally positive on ASML, which accounts for 53% of Europe IT[6]. Indeed, ASML is a direct beneficiary of semiconductor manufacturing capacity additions, which should support positive EPS revisions over the coming quarters. We also see meaningful upside to ASML’s 2030 mid-term guidance, which was set before the AI boom and assumed a semiconductor market of USD 1 trillion by 2030. Lastly, ASML’s historical valuation premium compared to US peers has disappeared.

We also keep our positive convictions on European healthcare and utilities. Within healthcare, the pharmaceuticals, biotechnology & life sciences sub-sector should benefit from improved policy visibility, innovation-driven growth, and compelling relative valuations. Regarding the utilities sector, it continues to benefit from strong structural growth drivers, including electrification and grid connections, while valuations remain reasonable.

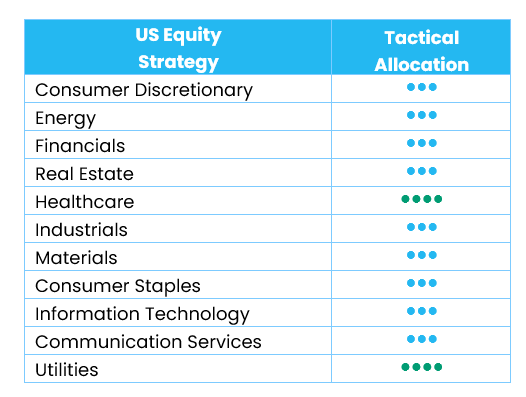

US equities: Resilient US market despite increased volatility

The past few weeks have marked a transition for US equities. Volatility increased amid evolving geopolitical tensions in the Middle East, easing oil price pressures, renewed inflation concerns and cautious central banks. Against this backdrop, US equities continued to advance, while sector leadership broadened beyond technology.

Leadership broadening beyond mega-cap technology

Despite continued uncertainty surrounding the macroeconomic backdrop, investor participation broadened. At the same time, investors became increasingly selective, favouring companies with stronger earnings visibility and more resilient fundamentals.

US equities advanced, with technology continuing to outperform despite periods of volatility. Market leadership broadened, however, as financials, industrials and healthcare also delivered strong relative performance. Consumer-related sectors remained under pressure, while energy was the weakest performer following the fall in oil prices.

From a style perspective, mid-caps and small caps outperformed large caps, while value outpaced growth among large caps and mid-caps.[7]

Upcoming earnings season

In the meantime, corporate fundamentals are still supportive just ahead of the Q2 earnings season. Earnings expectations continue to be revised upward, and consensus now expects 12-month forward earnings growth of 22%. Information technology remains the largest contributor, with forward earnings growth of 43%, underpinned by sustained AI investment.

The upcoming earnings season will therefore be an important test for the market. Expectations are relatively high, particularly in technology-related areas, where investors will look for confirmation that earnings momentum, AI-related investment and margins are strong enough to justify current valuations[8].

In this context, US equities currently trade at 20 times 12-month forward earnings[9]. Valuations remain above historical averages, making earnings delivery key to continued market performance.

Tactical changes in sector allocation

Over the past few weeks, we decided to fine-tune our US sector allocation through several tactical changes.

Technology Downgraded to Neutral

We tactically neutralised Information technology from +1. At sub-sector level, semiconductors and technology hardware were lowered to neutral from +1. The downgrade reflects a less favourable near-term risk-reward after strong performance since early May.

This is a tactical change, not a structural call. AI infrastructure spending, company results and earnings revisions remain supportive, so we stay strategically constructive on semiconductors and hardware.

Food, Beverage & Tobacco Downgraded to -1 from Neutral

Within consumer staples, we downgraded food, beverage & tobacco to -1 from neutral. The sector faces structural volume pressure from GLP-1 adoption, rising private-label penetration and weaker post-COVID volume trends. Rebuilding demand is likely to require price investment and higher brand spending, which could weigh on margins before volumes recover. Our neutral stance on the overall consumer staples sector remains unchanged.

Automobiles & Components Downgraded to -1 from Neutral

Within consumer discretionary, we downgraded automobiles & components to -1 from neutral. The industry group remains heavily driven by Tesla, where valuation leaves little room for disappointment, while competition in electric vehicles and autonomous driving continues to intensify. Our neutral stance on the overall consumer discretionary sector remains unchanged.

Retailing Upgraded to +1 from Neutral

We upgraded consumer retailing to +1 from neutral, mainly driven by Amazon’s exposure to three supportive growth engines: accelerating cloud demand, structurally higher e-commerce margins and ongoing advertising growth. The sub-sector also benefits from off-price retailers, which continue to capture trade-down demand. Home improvement offers inexpensive optionality if housing activity improves. The upgrade does not change our neutral stance on the broader consumer discretionary sector.

Separately, we maintain our positive grade on healthcare and utilities. In healthcare, better policy visibility, ongoing innovation and relative valuation support continue to favour biotechnology. Utilities retain a clear demand-growth profile, underpinned by electrification and AI-related power needs, with valuations still reasonable.

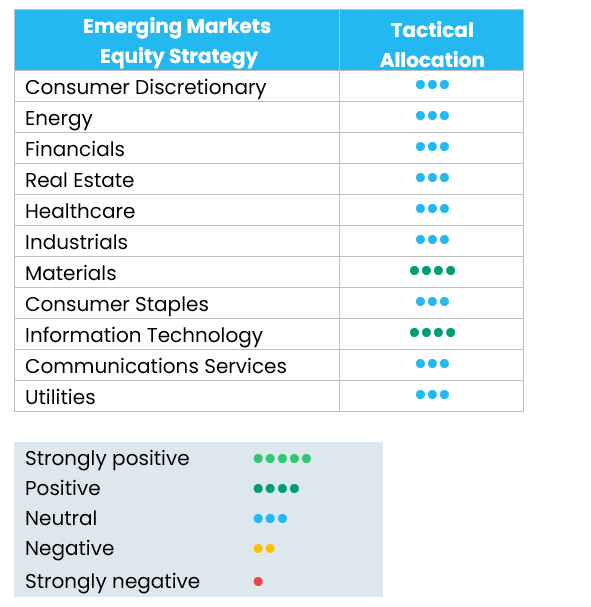

Emerging equities: Fundamentals remain supportive

Emerging market equities consolidated[10] in June after a very strong prior advance. The market remained anchored by the AI and technology themes. Geopolitical risk eased after the US-Iran ceasefire extension and the reopening of the Strait of Hormuz reduced the most acute energy-supply tail risk, triggering a sharp fall in oil prices and weighing heavily on energy and commodity-linked exposures.

Regional performance was uneven[11]. EM Asia proved relatively resilient. Fundamentals remained more constructive than headline returns suggested. Consensus earnings expectations for emerging markets continued to be revised higher, led by Taiwan and Korea, and supported by further upgrades in AI-linked markets. China was a major drag on index performance, as offshore equities weakened sharply and market leadership narrowed further around AI-related opportunities, while domestic activity softened and non-technology segments lost fundamental support. India outperformed, helped by the collapse in oil prices, resilient currency dynamics and policy measures aimed at attracting foreign capital.

US yields finished the month at 4.44%. As for commodities, Brent crude dropped -20.8% during the month, and gold fell -11.7%.[12].

Outlook and drivers

The Strait of Hormuz remains the key geopolitical focal point for markets. The ceasefire has reduced left-tail risk, but the situation remains fragile with continued attacks. Shipping flows have resumed in limited form, and operators are still relying on temporary workarounds. Further negotiations between Iran, the US and other stakeholders will therefore remain central to the evolution.

The technology sector in the Emerging Markets is now increasingly backed by earnings. Semiconductor demand remains strong, with global chip sales in recent months up sharply year-on-year and industry forecasts lifted on the back of AI infrastructure, accelerated computing, and high-bandwidth memory. The AI theme is also broadening beyond chips. It is becoming a physical infrastructure cycle, touching servers, power equipment, cooling, grid investment, energy storage and copper-intensive electrification. This creates a wider opportunity set across hardware, selected industrials, power-chain suppliers and resource-linked beneficiaries.

Fundamentals remain supportive for the Emerging Markets. Earnings momentum is increasingly solid, underpinned by resilient growth and improving profitability. At the same time, with global allocations still light, stronger fundamentals could attract incremental capital, leaving room for rerating if confidence in the Emerging Markets growth continues to broaden in the coming quarters.

Positioning update

Sector wise, we upgraded materials from neutral to overweight. The sector has lagged yet with solid fundamentals.

China

We remain neutral on China overall, but the internal picture is evolving. Hong Kong-listed China equities have started to recover and are now outperforming A-shares, suggesting a shift in investor appetite toward the more beaten-down and internationally owned parts of the market. Macro wise, the consumption remains fragile.

India, Southeast Asia, and Emerging Europe

We observed recovering signs for the previous laggards, including India, Southeast Asia, and part of Emerging Europe (Czech Republic, Hungary, and Greece). We are adding exposure to these regions.

Sectors

Technology

We remain positive on technology, but the sector is now entering an early consolidation phase. We have been adjusting portfolios accordingly, taking profits and reducing risk into the summer.

The semiconductor complex continues to deliver strong fundamental news, but the market’s reaction shows how demanding expectations have become. Samsung Electronics reported operating profit up almost 20 times year-on-year[13], broadly in line with expectations, yet the stock declined, while SK Hynix also declined and TSMC was relatively flat. This illustrates that the earnings bar is now extremely high: strong results alone may no longer be enough to drive further upside if investors have already priced in exceptional delivery.

Taiwan remains supported by powerful structural themes around AI, semiconductors, and the broader technology supply chain. However, many AI-related stocks in Taiwan have corrected by 15–20%[14], reflecting profit-taking in crowded longs rather than a fundamental deterioration. The long-term case remains intact, while the near-term setup is more fragile because positioning had become too concentrated. We continue to see compelling opportunities in Taiwan technology, but implementation needs to be more selective and valuation-aware.

China technology is also consolidating, particularly across domestic semiconductor and AI-related names such as Naura, AMEC, Iluvatar, Montage, and Cambricon. The move reflects both profit-taking after a strong run and the market’s reassessment of expectations around domestic technology self-sufficiency. Developments around CXMT and the potential IPO remain important catalysts, as does continued interest in China’s AI and semiconductor ecosystem. We remain selective: the structural story is convincing, but the trade has become more tactical after recent strength.

Materials upgraded from neutral to overweight

We upgrade materials from neutral to overweight after sharp one-month and three-month underperformance, driven mainly by a stronger US dollar and higher bond yields weighing on commodity-related equities.

Precious-metals exposure has become more interesting after the recent correction. The recent underperformance has left several names oversold, improving the potential for a rebound if rates, the dollar, or geopolitical risk premia turn more supportive.

For industrial metals such as copper, aluminium, zinc, and lithium, fundamentals remain constructive, where supply-demand dynamics continue to be supported by electrification, infrastructure, energy transition, and selective supply constraints. If the market starts to look through near-term macro pressure, these metals can provide a stronger earnings base for the sector. A potential progress toward a Middle East agreement could also add a further tailwind by improving global risk appetite and reducing macro uncertainty.

[1] Source: Bloomberg, 7 July 2026

[2] Source: Bloomberg, 7 July 2026

[3] Source: Bloomberg, 6 July 2026

[4] Source: Bloomberg, 6 July 202

[5] Source: Bloomberg, 7 July 2026

[6] Source: Bloomberg, 7 July 2026

[7] Source: Bloomberg, 7 July 2026

[8] Source: Bloomberg, 7 July 2026

[9] Source: Bloomberg, 7 July 2026

[10] Source: Bloomberg, 7 July 2026

[11] Source: Bloomberg, 7 July 2026

[12] Source: Bloomberg, 7 July 2026

[13] Source: Bloomberg, 7 July 2026

[14] Source: Bloomberg, 7 July 2026