Growth is slowing. Consumers are becoming more selective. Yet demand for strategic assets continues to accelerate. Chips, data centres, electricity, copper, defence equipment and energy infrastructure all tell the same story: one part of the economy wants more of everything, at once.

That tension increasingly defines the current market environment. On one side, households in Europe and China remain cautious, while US consumers are becoming more uneven. On the other, hyperscalers continue to commit unprecedented amounts of capital to AI infrastructure, supporting earnings, investment and equity markets. The result is a world where demand appears soft in many places, but remains insatiable in a few critical areas.

For investors, the key question is whether the extraordinary strength of AI-related investment can continue to offset weakness elsewhere.

When demand overwhelms supply

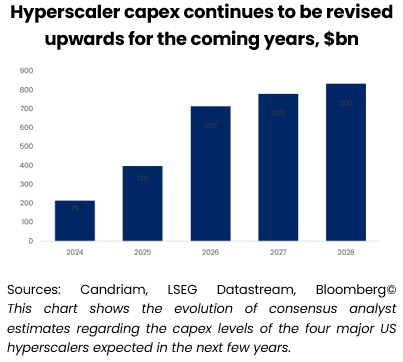

The most striking feature of the current cycle is not just the scale of AI investment, but the growing list of constraints it is creating. Hyperscalers are expected to invest more than USD 700bn in AI infrastructure in 2026. Corporate commentary remains remarkably consistent: order books are full, production capacity remains constrained and earnings revisions continue to move higher across large parts of the infrastructure ecosystem. Demand for semiconductors, networking equipment, data centres and power infrastructure is exceeding available supply.

Increasingly, the bottlenecks are becoming physical. Data centre capacity, electricity generation, grid infrastructure, transformers and strategic metals are all struggling to expand at the pace required. Capital is abundant; capacity is not.

This matters because shortages have consequences. They support pricing power, sustain earnings visibility and create barriers to entry. But they also create inflationary pressure. Unlike the inflation surge that followed the pandemic, the emerging pressure points are less broad-based and more concentrated around infrastructure, commodities and industrial capacity.

The question is no longer whether AI works. It is whether the extraordinary level of spending currently underway can generate returns commensurate with the capital being deployed. As the investment cycle expands, profitability is becoming as important as demand. The debate around AI is therefore evolving. It is no longer simply about productivity gains or software adoption. It is increasingly about whether the physical economy can keep up with the digital one.

The consumer is no longer carrying the cycle

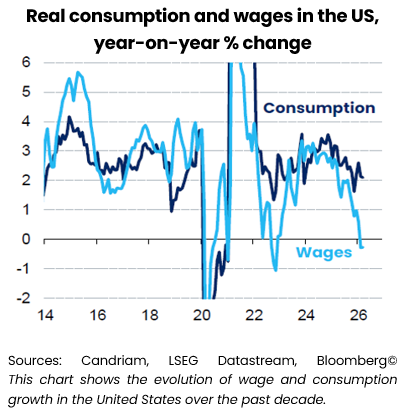

The consumer side of the economy tells a different story. In the United States, aggregate spending remains resilient, but the picture beneath the surface is becoming more uneven. Higher-income households continue to spend, supported by income growth and financial wealth via rising asset prices. Lower-income consumers face increasing pressure from declining wage growth, higher living costs and tighter financial conditions. This divergence helps explain why consumption remains positive even as confidence indicators soften. The US consumer is neither weak nor uniformly strong, but rather is becoming increasingly unbalanced.

Europe presents a less supportive picture. Consumer confidence remains subdued, and higher energy costs continue to weigh on spending intentions. Growth remains positive, but momentum is modest.

China faces similar challenges. Household confidence remains in the doldrums; savings rates keep rising from elevated levels and domestic demand continues to disappoint relative to policy ambitions. Growth increasingly relies on exports, technology and industrial policy rather than a broad-based recovery.

Taken together, these developments suggest that consumption is no longer the primary engine of global growth. Increasingly, that role is being assumed by investment.

Inflation: the banana skin

Inflation remains the principal risk to an otherwise constructive environment. Bond markets remain more sensitive than equities, with higher oil prices and rising inflation expectations contributing to upward pressure on yields, particularly at the long end. After a first wave of tariff-induced price shocks and a second wave linked to the oil shock, AI-related capex and infrastructure bottlenecks increasingly represent a third potential source of inflationary pressure, even if the timing and magnitude remain uncertain.

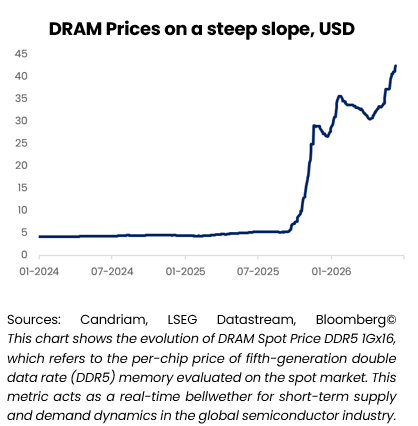

The concern is no longer limited to energy. Commodity markets, electricity infrastructure and industrial bottlenecks are becoming growing sources of inflationary pressure. The very investment cycle that supports growth and earnings also risks creating shortages. Demand for semiconductors, data centres, power generation, grid infrastructure and strategic metals is accelerating, while supply remains constrained.

Inflation risks are also becoming more diversified. Beyond energy and industrial bottlenecks, the emergence of El Niño conditions introduces an additional source of pressure through agricultural and food markets. The strongest impact is likely to be felt next year, but the combination of weather-related disruptions, tight fertiliser markets and existing geopolitical pressures could reinforce inflation persistence across several regions.

This does not mean inflation is set to reaccelerate sharply. It does suggest, however, that disinflation may prove slower and less linear than markets would like. That is particularly relevant for central banks. The Federal Reserve is unlikely to react to short-term energy volatility, but the path towards lower rates becomes more complicated if inflation proves persistent.

In this context, inflation remains the most plausible source of disappointment. It is the banana skin capable of turning an otherwise constructive environment into a more challenging one.

Positioning for selective strength

Our positioning is moderately constructive. We remain slightly overweight equities, expressed primarily through the United States and emerging markets. The United States continues to benefit from superior earnings visibility and AI leadership, while emerging markets offer attractive valuations and improving earnings dynamics, also led by tech companies.

In fixed income, we keep a long duration bias on high-quality German government bonds and hold emerging market debt. The former provides quality in a softening European activity context, while the latter adds diversification and benefits from attractive carry and improving capital flows.

Within credit, we continue to favour Investment Grade over High Yield, where risk premia remain limited and leave little margin for error.

In currencies, we think that commodity-linked currencies continue to benefit from the current environment and keep an underweight in the US dollar, with a preference for the Japanese yen.

Gold and strategic metals remain important portfolio diversifiers in a world increasingly shaped by shortages, policy divergence and real-rate volatility.

Candriam House View & Convictions

The table below is an indicator of the main exposures and movements within a balanced diversified model portfolio.

Legend

-

Strongly Positive

-

Positive

-

Neutral

-

Negative

- Strongly Negative

- No Change

- Decreased Exposure

- Increased Exposure

| Current view | Change | |

|---|---|---|

| Global Equities |

|

|

| United States |

|

|

| EMU |

|

|

| Europe ex-EMU |

|

|

| Japan |

|

|

| Emerging Markets |

|

|

| Bonds |

|

|

| Europe |

|

|

| Core Europe |

|

|

| Peripheral Europe |

|

|

| Europe Investment Grade |

|

|

| Europe High Yield |

|

|

| United States |

|

|

| United States |

|

|

| United States IG |

|

|

| United States HY |

|

|

| Emerging Markets |

|

|

| Government Debt HC |

|

|

| Government Debt LC |

|

|

| Currencies |

|

|

| EUR |

|

|

| USD |

|

|

| GBP |

|

|

| AUD/CAD/NOK |

|

|

| JPY |

|

Monthly Coffee Break

Updated each month, this section provides expert analysis and strategic insights. Stay informed with our latest market perspectives and allocations.

-

Monthly Coffee Break, Alternative Investments

Monthly Coffee Break, Alternative InvestmentsAI Cooled, Alternatives Ruled

June was marked by resilient but narrower global growth, still-elevated price pressures and a renewed focus on energy risk. Global PMIs remained consistent with expansion, but supply-chain tensions and geopolitical uncertainty persisted after the partial reopening of the Strait of Hormuz. -

Monthly Coffee Break, Asset Allocation

Monthly Coffee Break, Asset AllocationKeep calm and carry on

The global cycle is still catching its breath. World PMI edged up only marginally in June, still consistent with instant growth close to 2.5% in Q2. -

Monthly Coffee Break, Fixed Income

Monthly Coffee Break, Fixed IncomePositive on euro investment grade

We move US nominal duration back to neutral after the front-end overweight implemented last month. The main reason is the first FOMC meeting under Kevin Warsh and the market reaction that followed. -

Monthly Coffee Break, Equities

Monthly Coffee Break, EquitiesSector leadership is broadening beyond technology

Since the last equity committee in June, European equities have continued to advance, surpassing historic levels at the end of June, following the signing of the Memorandum of Understanding (MoU) between the United States and Iran.