The new engines of emerging market growth

China remains too important to ignore, but it should no longer dominate the emerging market conversation. Its recovery remains uneven, with investor attention concentrated in AI and semiconductor-related technology and selected industrial areas. Property remains fragile despite stabilisation, while consumer recovery is gradual and earnings pressure is still visible in areas such as e-commerce and food delivery.

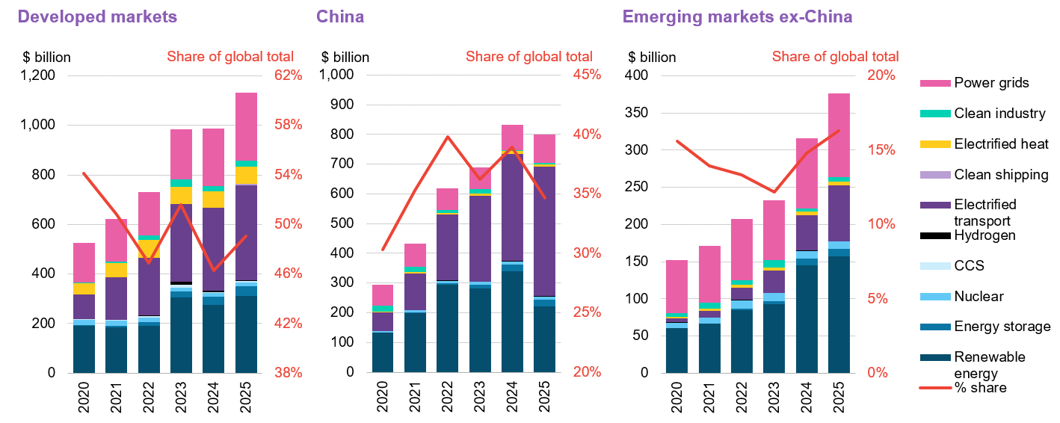

That does not remove the opportunity. It changes the way investors should approach it. While China faces well-documented challenges in property and consumer demand, it continues to invest heavily in areas aligned with long-term national priorities, including semiconductors, automation, renewable energy and advanced manufacturing. These sectors remain important drivers of innovation and industrial upgrading.

Looking beyond China brings two structural stories into sharper focus. The first is technology: Taiwan and South Korea represent the semiconductor and hardware infrastructure on which AI and digital transformation depend.

The second is demographics. India and parts of south-east Asia benefit from significantly younger populations than most developed economies, supporting labour force growth, rising incomes and expanding domestic consumption. These demographic advantages manifest themselves in different ways across the region, creating opportunities in manufacturing, infrastructure, financial inclusion and consumer-led growth.

The opportunity is not limited to Asia. Mexico has a clear link to nearshoring, as companies seek to reduce dependence on single-country supply chains. Brazil offers exposure to financials, utilities, commodities and renewable energy. In Latin America, financial inclusion remains an important theme, supported by underpenetrated banking systems and growing digital adoption. In EMEA, selected opportunities are linked to renewables, infrastructure and financial convergence.

Together, these markets reduce reliance on a single country, a single sector or the global technology cycle.