European equities: Tech-driven rebound amid geopolitical relief

European equities have risen since our last Equity Committee in May, driven by fading Middle East geopolitical risks. This de-escalation led to a significant fall in global crude oil prices, lowering inflation expectations, which provided broad relief to cyclical and consumer sectors. Simultaneously, the global AI boom fuelled a surge in European semiconductor companies. Robust European corporate earnings reports beat expectations and triggered widespread analyst valuation upgrades.

European equities have risen since our last Equity Committee in May, driven by fading Middle East geopolitical risks. This de-escalation led to a significant fall in global crude oil prices, lowering inflation expectations, which provided broad relief to cyclical and consumer sectors. Simultaneously, the global AI boom fuelled a surge in European semiconductor companies. Robust European corporate earnings reports beat expectations and triggered widespread analyst valuation upgrades.

Technology continues to lead

Since the last Committee, Information Technology has led the way, supported by a stellar performance from semiconductor companies, which have continued to benefit fully from the AI theme. As a result, IT has now delivered the strongest performance year-to-date, ahead of the Energy sector.

Cyclical sectors clearly outperformed defensive sectors, as the macroeconomic backdrop shifted rapidly into a risk-on phase, helped by lower geopolitical risks and easing inflation expectations. Among cyclicals, Consumer Discretionary was the best performer, although its rebound has not yet offset the losses incurred since the start of the year. Financials delivered the second strongest performance, driven by banks, which benefited from stronger-than-expected earnings and consolidation discussions. Real Estate was the only cyclical sector to post a negative return, weighed down by expectations of ECB rate hikes.

Defensive sectors lagged, particularly Utilities, which faced profit-taking amid lower electricity prices and higher interest rates. Consumer Staples remained broadly flat over the period, while Healthcare and Energy generated modest positive returns.

Lastly, Communication Services delivered the weakest performance in Europe, negatively impacted by portfolio rotations into high-growth sectors, rising concerns about AI disruption and expectations of higher rates.

In terms of market capitalisation, large caps outperformed mid and small caps, supported by the strong performance of ASML and other semiconductor companies[1].

Positive earnings revisions

European earnings revisions remain on a positive trend, with 52% of MSCI Europe constituents seeing upward revisions to next fiscal year earnings estimates over one month. Earnings revisions were strongest in Utilities, Information Technology and Energy.

European equities are expected to deliver 12-month forward earnings per share growth of 12%, according to Bloomberg data as at 8 June 2026. EPS growth is expected to be highest in the Energy sector (+48%), followed by Consumer Discretionary (+26%), Materials (+24%) and Information Technology (+20%). Conversely, Financials and Consumer Staples are expected to deliver the most limited EPS growth, at +1% and +2% respectively[2].

Since the last Equity Committee, European valuation multiples have slightly decreased, with the 12-month forward P/E ratio now standing at 15.0x (vs 15.3x previously). Information Technology and Industrials remain the most expensive sectors, trading at 32.9x and 22.2x respectively, while Energy and Financials remaining the cheapest, at 9.1x and 10.7x respectively, according to Bloomberg data as at 8 June 2026.

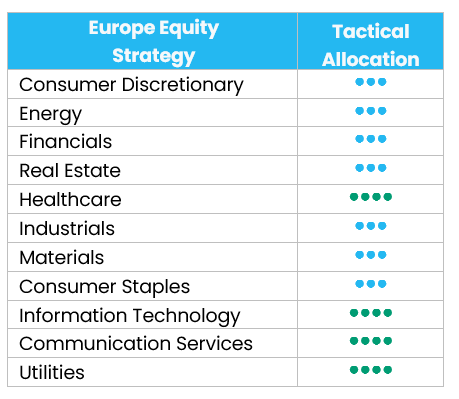

No change in sector grades

We maintain our sector grades.

At level 1, we retain our positive grade (+1) on the following sectors:

- Healthcare: The pharmaceuticals, biotechnology & life sciences subsector should benefit from improved policy visibility, innovation-driven growth, and attractive relative valuations.

- Technology: Semiconductors and hardware & equipment continue to benefit from robust demand driven by AI and data centre expansion. Valuations are not cheap but remain supported by strong earnings momentum and improving visibility.

- Communication Services: Consolidation in the European telecommunications sector should foster a more rational pricing environment over time. Synergies and improved operating leverage are expected to support earnings and cash flow.

- Utilities: The sector continues to benefit from strong structural growth drivers, including electrification and grid connections, while valuations remain reasonable.

US equities: Selective gains, solid earnings

US equities have moderately advanced since early May[3]. Inflation concerns, volatile oil prices and uncertainty around the Federal Reserve moved equity markets during the month, while higher bond yields ultimately limited the broader market gains. Meanwhile, earnings remained resilient and continued AI infrastructure investments supported technology-related market areas.

Visibility trade

US equities have slightly advanced over the past few weeks with improving market participation. Mid and small caps outperformed large caps, and value outperformed growth among large and small caps. With no clear leadership between cyclical and defensive sectors, sector performance remained mixed and investors favoured areas where earnings visibility was stronger, underscoring the importance of selectivity[4].

- Healthcare was the strongest outperformer, benefiting from its defensive characteristics amid a more uncertain macro backdrop, while compelling valuations and improving fundamentals provided support.

- Information Technology also outperformed the broader market, supported by demand linked to AI infrastructure, technology hardware and semiconductors, alongside a selective rebound in some software names.

- Energy and Financials also generated positive relative returns.

- In contrast, Communication Services, Materials, Consumer Discretionary, Consumer Staples and Utilities underperformed the broader market[5].

Earnings remain supportive

Despite a more selective market environment, corporate fundamentals remain supportive. Earnings revisions continue to point to resilient earnings trends, with 63% of MSCI USA constituents seeing upward revisions to next fiscal year earnings estimates over one month[6].

This positive revision backdrop is reflected in constructive earnings growth expectations. US equities are expected to deliver 12-month forward earnings per share growth of 21%. Information Technology remains the main contributor, with forward earnings growth of 41%, supported by continued AI investment[7].

In this context, US equities are trading at less than 20 times 12-month forward price-to-earnings, down from 22 times one month earlier[8]. Valuations remain above historical averages, but the recent derating and strong earnings growth provide a more solid fundamental basis.

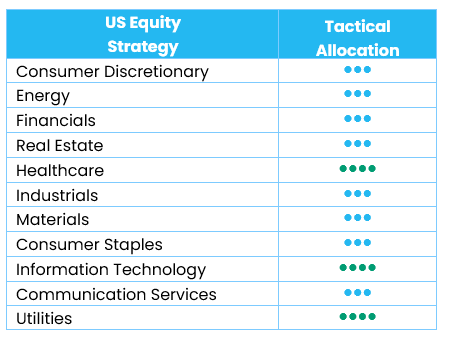

Sector positioning unchanged

We maintain our current sector positioning and remain confident in our core convictions: Healthcare, Utilities and Information Technology.

- Healthcare is supported by improved policy visibility, innovation-driven growth and compelling relative valuations, particularly within pharmaceuticals and biotechnology.

- Utilities benefit from strong visibility on demand growth, supported by structural drivers such as electrification and rising AI-related power consumption. Earnings growth is expected to reach the low double digits over the next 12 months, while valuations remain reasonable.

- In Information Technology, structural demand remains robust, especially in hardware and semiconductors linked to AI infrastructure and digital transformation. Despite the strong price increase of recent months, valuations remain reasonable. Hardware seems a little expensive, but the expected price-to-earnings ratio for semiconductors is still in line with the average of the past five years. We see no reason to reduce our technology exposure for now.

Emerging equities: Powerful recovery

Emerging Markets continued to rise in May[9], with the asset class advancing strongly and continuing to outpace developed markets as global risk appetite remained resilient. Investor concerns around AI monetization faded, while sustained hyperscaler capital expenditure reinforced confidence in the durability of the semiconductor cycle.

Regarding regions, Korea’s rally was particularly powerful[10], supported by exceptional earnings momentum, positive revisions across most sectors and a broadening of enthusiasm beyond the largest semiconductor names into adjacent manufacturing and industrial themes. Taiwan also reached new highs[11], as conviction strengthened around the continuation of cloud service provider capex, although valuations moved to elevated levels. China underperformed[12], as resilient results and continued AI investment commitments from internet companies were offset by weakness in domestic consumption, mixed earnings delivery outside technology, and only limited support from the mid-month US-China summit, which helped reduce near-term escalation risks but did not produce a major trade breakthrough.

At the sector level, Information Technology dominated returns. Energy and Utilities declined, while the Energy sector was pressured by a sharp fall in oil prices[13].

Outlook and drivers

Emerging Markets already recovered sharply in May[14], and are increasingly supported by earnings, cash-flow visibility and an investment cycle that is becoming broader. For the second half of 2026, the geopolitical backdrop is looking at a potential stabilization. The strongest support for a positive EM outlook comes from resilient earnings momentum, still-compelling valuations and global under-exposure to emerging markets.

In Asia, AI-related hardware, memory and semiconductor supply chains continue to deliver excellent operating leverage. Earnings are rising on pricing power, tight supply and multi-quarter demand visibility. AI remains the clearest leadership theme in global equities, and EM has become one of the most direct ways to access the physical infrastructure behind it: advanced chips, high-bandwidth memory, servers, power equipment, thermal management and energy storage. At the same time, the story is no longer only about AI. Recent estimate revisions can reinforce a broader AI-and-commodities narrative. Upgrades are strongest where companies benefit from data-centre investment, electrification, power shortages, energy security and resource scarcity.

Valuation and positioning remain key pillars of the EM equity case. Even after a strong advance, the asset class continues to trade at a sizeable discount to developed markets, particularly the US. With global allocations still light, stronger fundamentals could attract incremental capital, leaving room for rerating if confidence in EM growth continues to broaden over the next several quarters.

Positioning update

No rating change during the period. We remain positive on Asian technology while conducting risk management through profit taking.

Regions

Taiwan & Korea

We maintain an overweight as technology and earnings tailwinds remain powerful, with opportunities still compelling across the technology supply chain. Both countries continue to benefit from strong positioning and robust earnings dynamics, reinforcing our positive view. Meanwhile, we are increasingly attentive to stretched technicals. We are monitoring risk management closely, while keeping the core thesis intact.

Brazil

The market continues to behave as a stock-picker’s environment. Rather than relying on broad beta, the emphasis is on identifying idiosyncratic opportunities with company-specific catalysts, resilient balance sheets and clear earnings visibility. This posture keeps us engaged in Brazil’s opportunity set, while acknowledging that conviction is more selective than directional.

China

The macro picture is still mixed, with consumption staying soft, limiting confidence in a broad-based rebound. Valuations of the leaders in domestic consumption are becoming more interesting. The recent Trump–Xi meeting has helped sentiment at the margin, but it does not change the longer-term reality of a competitive and strategically contested landscape. As such, our stance is best expressed through selectivity.

Sectors

Technology

We remain positive on Technology. Tactical risk management is required as technicals are increasingly stretched and momentum has become crowded as a style factor. In practice, we have taken some profits. Fundamentals remain solid, while upside is more incremental when positioning is tight. The objective is to preserve gains, reduce drawdown sensitivity and retain flexibility to rebuild exposure on more compelling entry points.

Energy

The sector is acutely sensitive to geopolitical outcomes and crude price volatility. News flow continues to point to elevated uncertainty, and the possibility of renewed conflict episodes cannot be dismissed, which keeps risk premia unstable and timing difficult.

[1] Sources: all sector-related performances – Bloomberg, 8 June 2026

[2] Source: Bloomberg, 8 June 2026

[3] 5.3%. Source: S&P 500, 31 May 2026

[4] Source: Bloomberg, 8 June 2026

[5] Sources: all sector-related performances – Bloomberg, 8 June 2026

[6] Source: Bloomberg, 8 June 2026

[7] Source: Bloomberg, 8 June 2026

[8] Source: Bloomberg, 8 June 2026

[9] Source: MSCI Emerging Markets (+9.5%), 31 May 2026

[10] Source: MSCI Korea +34.9%

[11] Source: MSCI Taiwan +16.3%

[12] Source: MSCI China -3.4%

[13] Source: Bloomberg, 8 June 2026

[14] Source: MSCI Emerging Markets (+9.5%), 31 May 2026