May was defined by resilient global activity but rising macro uncertainty. Manufacturing PMIs held up better than services, while inflation risks re-emerged, as Middle East tensions disrupted traffic through the Strait of Hormuz and kept energy-related risks central to the outlook. In the eurozone, the earlier recovery lost momentum, with first-quarter growth slowing in most countries, services weakening, consumer confidence deteriorating and higher energy prices beginning to weigh on household purchasing power. The ECB’s position became less comfortable, with upside inflation risks limiting scope for policy easing despite weaker demand. In the US, private domestic demand remained firm, supported by AI-related investment, but consumption relied increasingly on lower savings amid slowing real income growth and higher gasoline prices.

May was defined by resilient global activity but rising macro uncertainty. Manufacturing PMIs held up better than services, while inflation risks re-emerged, as Middle East tensions disrupted traffic through the Strait of Hormuz and kept energy-related risks central to the outlook. In the eurozone, the earlier recovery lost momentum, with first-quarter growth slowing in most countries, services weakening, consumer confidence deteriorating and higher energy prices beginning to weigh on household purchasing power. The ECB’s position became less comfortable, with upside inflation risks limiting scope for policy easing despite weaker demand. In the US, private domestic demand remained firm, supported by AI-related investment, but consumption relied increasingly on lower savings amid slowing real income growth and higher gasoline prices.

Risk assets rallied strongly in May, led by technology and AI-linked markets. US equities generated solid positive returns, but Asian technology-heavy indices outperformed significantly, led by Korean markets and Taiwanese equities. European equities also advanced, albeit more moderately, with low single-digit returns. Sector performance was dispersed. Information Technology dominated returns, while Energy lagged as oil prices fell. Core rates were volatile: lower oil and improved risk appetite supported bonds late in the month, but central bank expectations remained sensitive to sticky inflation, especially in the US and the eurozone.

The HFRX Global Hedge Fund EUR Index was up 1.58% over the month.

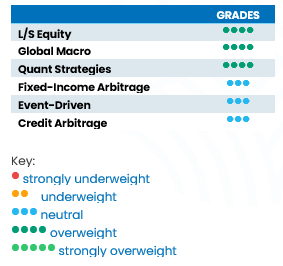

L/S Equity

Long-short equity strategies performed well in May, but returns were highly dependent on exposure to AI, semiconductors and Asia. Returns were dispersed across equity strategies. HFR reported Equity Hedge up 2.7%, led by Technology at 10.6% and Quantitative Directional at 4.0%, while Healthcare declined by 2.04%. Morgan Stanley prime brokerage data showed Global L/S long books producing a positive spread, with APAC the strongest contributor and Japan longs outperforming shorts by around 20%. Positioning remained crowded: global semiconductors and hardware exceeded 35% of global net exposure, while Europe and US ex-AI exposures stayed light. The outlook is constructive but vulnerable to rotation or AI profit-taking.

Global Macro

Global macro delivered modest aggregate gains despite large cross-asset moves. HFR reported Macro up 0.2%, with active trading up 1.7% and discretionary thematic up 1.2%, offset by commodity and systematic CTA losses. Performance drivers included falling oil prices, resilient equity momentum, volatile rate expectations and mixed currency trends. In the near term, managers remain cautious about the risk of a sharp reversal in market sentiment and asset prices, driven by factors such as energy markets, inflation developments and shifting central bank expectations. Over the longer term, however, the opportunity set is becoming increasingly attractive, supported by growing divergence across asset classes, countries’ growth trajectories and policy paths.

Quant Strategies

Quantitative strategies benefited from strong trend and factor dispersion, although results likely varied by model design. HFR’s Equity Hedge Quantitative Directional Index gained 4.0%, supported by equity momentum, technology leadership and regional dispersion. At the same time, systematic diversified CTA strategies struggled, as sharp oil reversals and shifting rate expectations created difficult conditions for medium-term trend models. Morgan Stanley noted elevated single-stock dispersion and historically narrow equity leadership, conditions that can help stock selection models but hurt crowded factor portfolios. The outlook favours adaptive models able to balance momentum in AI with mean-reversion risk and broader sector rotation.

Fixed Income

Fixed income arbitrage and relative-value rates strategies were positive but not dominant in May. Drivers included greater clarity around the Fed leadership transition, volatile curve expectations and opportunities in sovereign-rate relative value as markets repriced the Fed and ECB paths. Candriam macro-economists note the ECB faces a less comfortable inflation-growth trade-off after the energy shock. Positioning from fixed income arbitrageurs is likely to remain cautious, with leverage constrained by rate volatility. The near-term outlook is constructive if curve dispersion persists, but vulnerable to renewed inflation shocks.

Event-Driven

Event-driven strategies performed well during the month of May. The risk-on market dynamic favoured more directional strategies, with Special Situations clearly outperforming pure Merger Arbitrage books. However, since the start of the year, hard-catalyst strategies have performed well, providing resilience versus market volatility and a decent performance. Deal selection and portfolio construction remains a very important element to navigate the current environment. The short-term outlook is balanced: volatility creates entry points, but geopolitical risk might limit upside. However, for the longer term, the opportunity set is expected to improve, with more deals coming to market and helping spreads to stabilise.

Credit Arbitrage

Credit arbitrage strategies produced steady gains, supported by resilient risk appetite and contained credit stress. May’s equity rally, lower oil prices and improving capital market sentiment supported carry and spread compression, while idiosyncratic dispersion created relative-value opportunities. Credit managers also benefited from strong demand for financing around AI infrastructure and data centre investment, although this added concentration risk in technology-linked capital structures. The outlook remains moderately supportive as long as growth holds and default expectations stay contained.