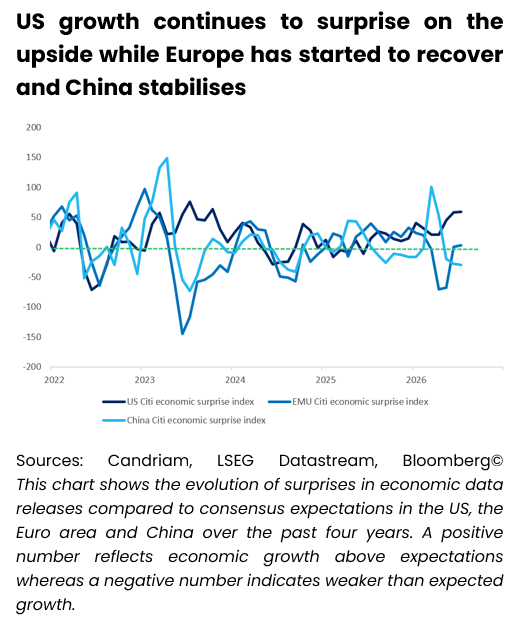

The global cycle is still catching its breath. World PMI edged up only marginally in June, still consistent with instant growth close to 2.5% in Q2, down from just above 3% before the Iran war. Underneath that soft headline, a rotation is taking shape: services are recovering from a weak base, just as manufacturing loses some momentum as restocking needs fade. Company leaders read this shift cautiously. Order books are firmer, yet production and hiring plans stay guarded, and with the global labour market close to stalling, household confidence remains poor.

Growth Catches Its Breath

Geopolitics still sits at the centre of the story. US-Iran negotiations continue in a chaotic and drawn-out manner, as expected, but recent tensions have not derailed the process yet. That relative stability should let oil settle a bit above $70 by year-end, an easing that filters through the same channels weighing on the cycle today: supporting household purchasing power and helping restore purchasing manager confidence. On that basis, growth should recover moderately in H2, returning to around 3%+ by the turn of 2026/27. Inflation tells a parallel story of gradual relief. Global inflation, at 3.5% in June, has likely peaked, and second-round effects should stay contained given weak growth, limited corporate pricing power and reduced wage bargaining strength. That backdrop already frames how central banks are behaving. Several, including the ECB, have started raising policy rates again, but the scale of tightening should remain limited.

The regional picture adds texture to this global average. The US spent H1 absorbing a petrol price shock that ate into household purchasing power, even as corporate investment held up well. That divergence is now starting to close: jobs are turning up again and cheaper gasoline should restore some consumer spending power, while high margins, compounding productivity gains and Tech capex keep working as a structural tailwind. We expect 2026 US growth at 2.2% and 2027 at 2.1% in our central scenario.

Europe's story runs the other way, from weakness toward repair. The region is emerging from a technical recession, with H1 growth close to flat, but confidence indicators turned up in June from a low base. Cheaper energy should ease pressure on households just as it does in the US, and on the policy side, the ECB's June hike is behind us, with the central bank having since softened its tone. We expect 2026 growth at 0.5%, rising to 1.3% in 2027 as investment and a consumption rebound both contribute.

China, meanwhile, slowed in Q2 as domestic demand and public spending lost momentum. Yet the underlying signals hold up better than that deceleration suggests: the electronics cycle stays resilient and property prices are stabilizing. We nonetheless expect 2026 growth at 4.5%, in line with consensus. Across all three regions, inflation is easing, and that shared relief is what ultimately gives the Fed, the ECB and the PBoC room to stay patient rather than react.

The Market's Own Agenda

Against this backdrop of moderating inflation and modest growth recovery, markets have already started looking past the macro story toward their own dynamics. Equities entered a more idiosyncratic phase. Renewed strikes around Iran triggered a bout of risk-off, a reminder that the ceasefire stays fragile, even if we still expect it to hold for now. Momentum names, which had lagged since the US-Iran memorandum, bounced back. The correction in Tech and Semis removed some of the froth built up earlier in the year. Index volatility stayed low, but dispersion across stocks and factors spiked. Positioning remains elevated, so the summer could still bring further jitters.

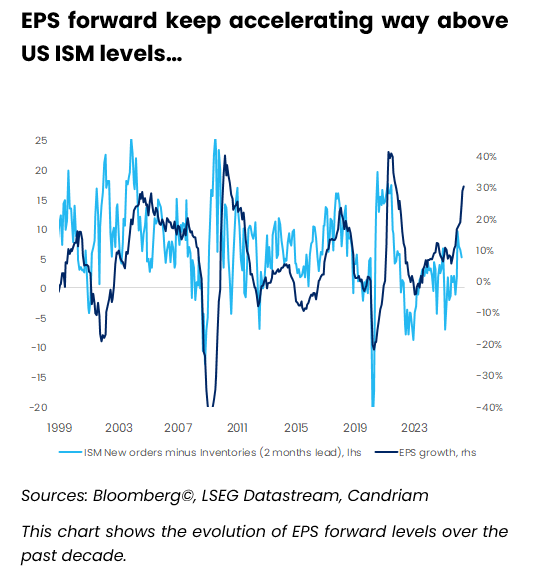

From here, earnings carry the burden of proof. Q2 results will test whether the AI capex cycle can keep justifying current valuations. AI infrastructure names alone are expected to drive around 60% of S&P 500 EPS growth. The "Heavy Assets Low Obsolescence" trade has already delivered its first leg, closing much of the valuation gap between capital-intensive and capital-light winners. The next leg should depend more on earnings delivery and less on re-rating, favouring dispersion within the theme over a broad continuation. Equity supply is rising too, through mega-cap IPOs and European issuance, but buybacks and M&A, backed by strong balance sheets, should keep absorbing it.

Rates markets are working through their own adjustment. The ECB has already raised policy rates again and the Fed has hardened its tone, though the scale of tightening should stay limited if disinflation keeps going. Long yields show little room to fall but also little room to rise, a balance already reflected in pricing. Term premium concerns persist against heavy fiscal issuance across the US, Europe and Japan, keeping duration positioning selective. Carry remains the main source of return in fixed income for now. Credit spreads sit a touch above pre-Iran-war levels, leaving some room for compression, while core European sovereign debt benefits from a comparatively better growth and inflation mix than the US.

Commodities complete the picture. Oil has swung back up on renewed Gulf tensions after falling sharply from its May highs, and should keep embedding a geopolitical risk premium as negotiations stay chaotic and drawn out. Gold has pulled back from its highs but should continue to add robustness to portfolios over the longer term.

Cross-Asset Strategy

The second half asks markets to hold two timeframes at once. Negotiations stay chaotic, earnings still need to deliver, and volatility will test conviction along the way. But capital has already made its choice. It keeps flowing into the assets that scarcity and rivalry both demand, and that patience, more than any single data point, is what should carry portfolios through the noise ahead.

Equities

We enter the second half slight overweight on equities, expressed through Japan and Emerging Markets rather than the US, which we hold at neutral.

That neutral stance reflects our view on US Technology, a sector carrying roughly half the weight of the broad US market, and with few catalysts likely before Q2 earnings season closes out in late July, we see limited reason to chase the sector for now. Japan is where we look for equity leadership: a prudent BoJ and supportive government initiatives should keep the backdrop favourable through H2, while the market offers concentrated exposure to AI winners across semiconductors, data centre infrastructure and automation, backed by world-leading franchises in robotics and industrial equipment that leave it well placed to capture the next phase of AI-driven productivity gains. Emerging Markets keep their slight overweight for H2 too, with selectivity remaining the key discipline since strong Tech exposure underpins the region. Europe, by contrast, stays neutral going into H2: lower energy prices should provide some support, but the region's sector composition leaves it less geared to the themes we expect to dominate markets over the coming months, even as German fiscal spending should build momentum as the year progresses, a trend worth monitoring into year-end.

Across factors and sectors, our H2 preference goes to beneficiaries of investment cycles, whether driven by AI or by government spending. We keep constructive exposure to Healthcare, alongside EU and US mid-caps and industrials, which should stay somewhat insulated from swings in expansionary budgets and deregulation through the second half.

Sovereign Bonds

In government bonds, we go into H2 long European core duration. The Iran war drove an inflation-driven repricing through markets earlier this year, lifting inflation expectations on the back of energy and supply disruptions. ECB easing expectations, which had run far at the start of the year, have since reversed, and we think that move has gone too far heading into H2. We keep our focus on high-quality, core-European AAA sovereign debt, where fiscal and central bank credibility both hold. US Treasuries sit on the other side of the trade for H2. Strong growth, AI capex and an inflationary impulse, combined with deficit concerns, should keep upward pressure on US rates, so we stay slightly short.

Credit

Credit heads into H2 on a more cautious footing. European Investment Grade spreads have barely moved, not enough to open a broad valuation opportunity while macro uncertainty stays elevated. Fundamentals remain solid, but sensitivity to higher rates argues for neutrality over an outright overweight for the second half, so we favour selectivity. We hold Investment Grade at neutral in both the US and Europe. High Yield looks more fragile heading into H2: outflows and rising supply are weighing on technicals, leaving us neutral on Europe and negative on the US.

Emerging Market debt is where we see the more constructive H2 credit story. Sovereign local currency debt benefits from a spread tightening trend that is unfolding again, with room for further compression through year-end. EM FX looks well placed to benefit from renewed dollar weakness, and a yield-to-maturity near 7% gives the position an attractive carry as a diversifier into H2.

Alternatives

Alternatives complete our H2 positioning. Diversification also deserves a broader definition: Gold and strategic metals remain valuable portfolio components, notably as beneficiaries of the structural investment cycle discussed above.

Currencies

Currencies follow the same logic as commodities heading into H2. The current regime favours currencies tied to hard assets, so we hold long positions in AUD, NOK and BRL. We also hold a long JPY position into the second half.

Candriam House View & Convictions

The table below is an indicator of the main exposures and movements within a balanced diversified model portfolio.

Legend

-

Strongly Positive

-

Positive

-

Neutral

-

Negative

- Strongly Negative

- No Change

- Decreased Exposure

- Increased Exposure

| Current view | Change | |

|---|---|---|

| Global Equities |

|

|

| United States |

|

|

| EMU |

|

|

| Europe ex-EMU |

|

|

| Japan |

|

|

| Emerging Markets |

|

|

| Bonds |

|

|

| Europe |

|

|

| Core Europe |

|

|

| Peripheral Europe |

|

|

| Europe Investment Grade |

|

|

| Europe High Yield |

|

|

| United States |

|

|

| United States |

|

|

| United States IG |

|

|

| United States HY |

|

|

| Emerging Markets |

|

|

| Government Debt HC |

|

|

| Government Debt LC |

|

|

| Currencies |

|

|

| EUR |

|

|

| USD |

|

|

| GBP |

|

|

| AUD/CAD/NOK |

|

|

| JPY |

|

Monthly Coffee Break

Updated each month, this section provides expert analysis and strategic insights. Stay informed with our latest market perspectives and allocations.

-

Monthly Coffee Break, Alternative Investments

Monthly Coffee Break, Alternative InvestmentsAI Cooled, Alternatives Ruled

June was marked by resilient but narrower global growth, still-elevated price pressures and a renewed focus on energy risk. Global PMIs remained consistent with expansion, but supply-chain tensions and geopolitical uncertainty persisted after the partial reopening of the Strait of Hormuz. -

Monthly Coffee Break, Asset Allocation

Monthly Coffee Break, Asset AllocationKeep calm and carry on

The global cycle is still catching its breath. World PMI edged up only marginally in June, still consistent with instant growth close to 2.5% in Q2. -

Monthly Coffee Break, Fixed Income

Monthly Coffee Break, Fixed IncomePositive on euro investment grade

We move US nominal duration back to neutral after the front-end overweight implemented last month. The main reason is the first FOMC meeting under Kevin Warsh and the market reaction that followed. -

Monthly Coffee Break, Equities

Monthly Coffee Break, EquitiesSector leadership is broadening beyond technology

Since the last equity committee in June, European equities have continued to advance, surpassing historic levels at the end of June, following the signing of the Memorandum of Understanding (MoU) between the United States and Iran.