Circularity: from waste reduction to strategic resilience

Circularity is often associated with recycling, but that is only part of the story. A circular economy also involves product redesign, repair, reuse, material recovery, automated sorting, advanced packaging and more efficient industrial processes. The objective is to reduce dependence on raw materials and keep more value within the economy for longer.

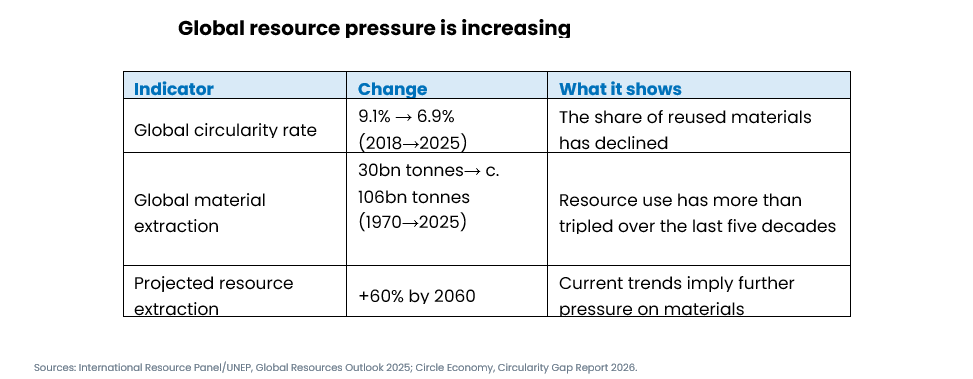

The scale of the opportunity remains significant. The share of materials reused by the global economy has declined in recent years, from 9.1% in 2018 to 6.9% in 2025.[2] In other words, circularity is becoming more widely discussed at precisely the moment when the economy is becoming less circular.

For businesses, this can become a competitiveness issue. Reducing material intensity may help limit exposure to commodity volatility, supply disruption and regulatory pressure. Improving recovery and reuse can also support more resilient industrial models.

For investors, the opportunity is not limited to traditional waste management. It may extend to companies supplying industrial automation, material-recovery systems, sensors, software, recycling equipment and advanced manufacturing technologies. These are the systems that can help turn circularity into practical circular industrial solutions.

Water is becoming an industrial issue

Water is often discussed as a social and environmental challenge. Increasingly, it is also becoming an economic one.

More than 2 billion people still lack safely managed drinking water, while around 3.5 billion lack safely managed sanitation.[3] At the same time, water scarcity is increasingly relevant for industrial capacity, infrastructure planning and supply-chain resilience. The World Bank has estimated that water scarcity could cost some regions up to 6% of GDP by 2050.[4]

The investment implications are broad:

- Ageing networks need to be upgraded;

- Leakage needs to be reduced;

- Treatment and reuse capacity need to expand.

Industrial users need systems that allow them to recycle water, reduce consumption and operate more reliably in water-stressed regions.

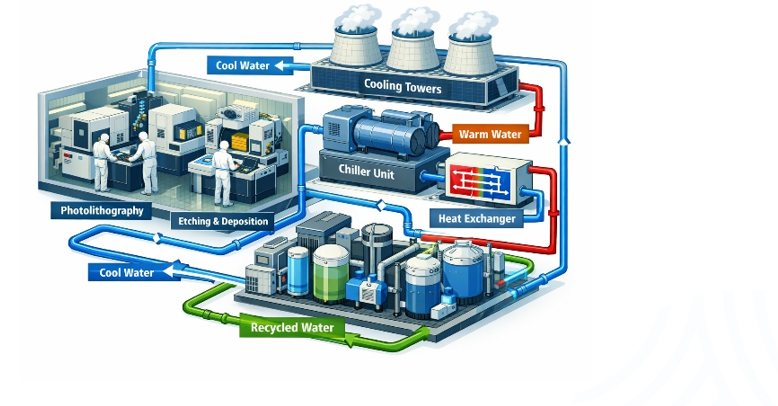

Semiconductors offer a useful example. Advanced chip manufacturing depends on highly controlled environments, stable cooling and large volumes of ultra-pure water. Efficient cooling, heat exchange, treatment and recycling are not peripheral sustainability measures. They can be central to productivity, reliability and cost control.