Last week in a nutshell

- ECB policymakers maintained their support for a June interest rate reduction after a confirmed downward trending euro zone CPI.

- In his speech, Fed Chair Jerome Powell emphasised the necessity of maintaining a prolonged restrictive monetary policy, indicating fewer cuts from the Fed this year.

- Despite higher rates, US Consumers kept shopping at a more rapid pace than expected. Retail sales grew much higher than forecasted.

- The few S&P 500 companies that published their Q1 earnings reported, on average, sales, EPS and margins above expectations.

What’s next?

- With the Global flash PMIs out, focus will shift to major economies' growth momentum. European readings, especially Germany's, are closely watched after the lagging performance among euro zone peers last year.

- Consumer and business sentiment will take centre stage with the ECB’s preliminary Consumer Confidence report, Germany’s IFO business climate index, and the US’s final Michigan sentiment readings.

- The US is set to unveil a plethora of economic data including the first Q1 GDP reading, core PCE inflation figures, and new home sales statistics, offering insights into various aspects of economic activity.

- The Bank of Japan is meeting and will publish its Quarterly Outlook Report. The bank faces a challenge with the significantly weakened yen. While this bolsters exports, it also drives up household living costs due to increased import prices.

Investment convictions

Core scenario

- 2024 comes with more visibility as the economic uncertainties decline in the US and in Europe, where the energy crisis was avoided. Uncertainties remain elevated, nonetheless in Germany. In addition, developed Central Banks have rebuilt room for manoeuvre.

- The goldilocks environment characterised by positive growth surprises and negative inflation surprises is spilling into the euro zone. Growth surprises are positive in all major regions while inflation surprises upwards only in the US.

- In China, economic activity has shown some fragile signs of stabilisation while the evolution of prices remain deflationary.

Risks

- An overshooting in the price of oil, US yields or the US dollar are key variables to watch. Geopolitical risks to the outlook for global growth remain tilted to the downside as developments in the Red Sea unfold and the war in Ukraine continues.

- Bond yields are to be monitored especially given the diverging paths taken by the strong US economy and its stabilising European counterpart, which triggers an increasing spread in yields.

- A stickier than expected US inflation could force the Federal reserve bank to reverse course. In our understanding, it would take more than just the bumpy data registered since the start of the year.

- Beyond commercial real estate exposures, financial stability risks could return as a result of the steepest monetary tightening of the past four decades.

Cross asset strategy

- Taking into account the momentum in global manufacturing PMI, we added some beta and cyclicity to the strategy.

- Our strategy reflects the latest development on the euro zone: economic surprises are positive as sentiment and flows may have turned a corner. Investor interest seems to be on the mend, and with a broadly attractive risk premium, the potential for a catch up by laggards is increasing.

- We have the following investment convictions:

- Our equity allocation has become slightly overweight, via a more constructive view on the euro zone equity market where the latest inflation readings are within the European Central Bank’s target lower and upper bounds.

- We have been looking for opportunities in beaten down stocks in small and mid-caps and are now starting to add in this segment.

- In the fixed income allocation:

- We have a positive stance on European duration and aim for the carry in a context of cooling inflation.

- We remain exposed to emerging countries’ debt to benefit from the attractive carry.

- We maintain a neutral stance on US government bonds, looking for a new, more attractive, entry point.

- We have a neutral stance on European Investment Grade credit.

- We hold a long position in the Japanese Yen and have exposure to some commodities, including gold, as both are good hedges in a risk-off environment.

- We expect Alternative investments to perform well as they present some decorrelation from traditional assets.

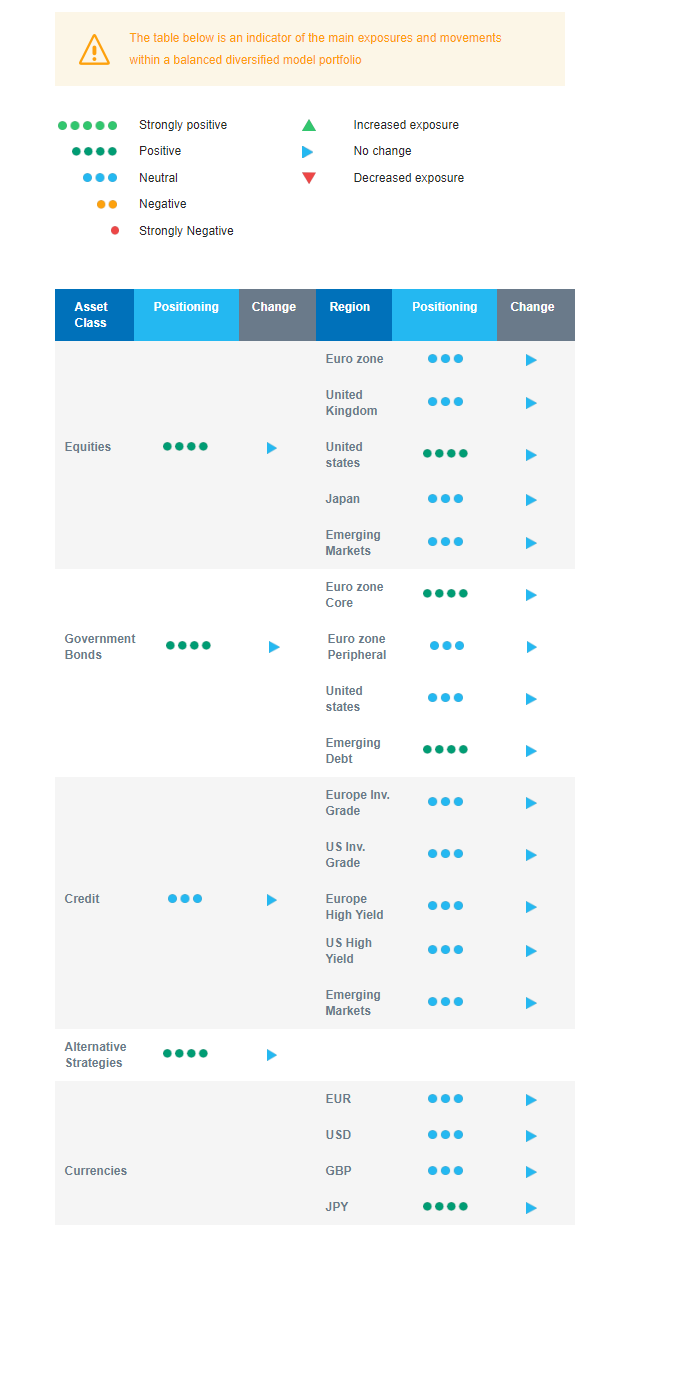

Our Positioning

With the addition of cyclicity to the portfolio, the strategy benefits from a broadening of the goldilocks environment. In Europe in particular, economic surprises are positive, leading to improving sentiment and flows. Investors’ interest is returning, and with the risk premium attractive overall, laggards could perform better in a context of economic improvement and catch up. Beyond the dataflow, we were reassured by the recent central bank meetings and think that the expected upcoming central bank rate cuts are an additional element which should act as support while capping long-term bond yields, underpinning our positive view on duration. We keep a supportive stance on US equities amid a positive EPS momentum and are neutral on Europe, Japan and Emerging markets. We also continue to harvest carry via Emerging Market debt.