Market neutral strategies involve taking both long and short positions on assets, aiming to exploit relative value or price inefficiencies. They target a low net exposure to the equity market, and a low to moderate level of volatility. We have identified two distinct market areas where we strive to extract value while offering regular returns:

- Market events linked to the growth of passive investments and

- Quantitative multifactor investing with an ESG framework.

Taking advantage from a structural trend: The growth of passive investing

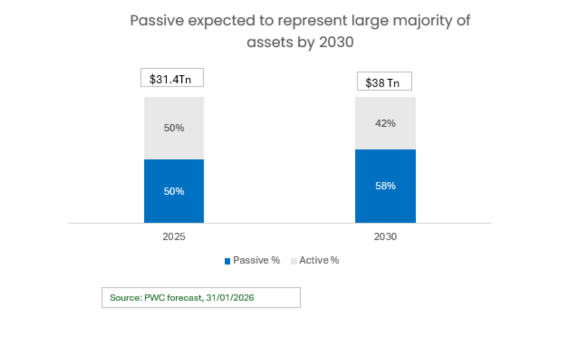

Over the past decades, the financial industry has been profoundly shaped by the steady growth of passive investing. PwC expects that by 2030, passive funds may represent 58% of total US mutual fund/ ETF industry assets[1]. The pricing distortions generated by this phenomenon can be transformed into investment opportunities.

Two complementary performance engines

Candriam’s market neutral strategies draw on two distinct sources of return, each targeting different types of market inefficiencies.

First, index rebalancing events trigger large in- and outflows that may result in temporary price dislocations. Our investment team closely monitors these events with the aim of generating returns through a combination of long and short positions on listed stocks.

Second, relative value opportunities arise from valuation discrepancies between securities. By identifying stocks that appear relatively over- or undervalued, the strategy seeks to capture the normalisation of these spreads over time.

These opportunities are reinforced by the continued growth of passive investing, which can amplify pricing dislocations and expand the overall opportunity set.

Seeking stable return through challenging market environments

Market neutral strategies are designed to reduce reliance on overall market direction by focusing on relative value opportunities. While equity market volatility can vary significantly over time, the strategy seeks to maintain a more stable return profile by capturing pricing inefficiencies rather than broad market movements.

Multifactor quantitative equity: Aiming to drive consistent alpha by combining quantitative financial and ESG analysis

Our ESG market neutral strategy aims to combine long positions in fundamentally sound companies with strong environmental, social and governance (ESG) credentials, with short positions in companies with weaker financials and poor ESG scores. By balancing these positions, we aim to capture the return spread between the two groups, which we expect to be positive over time and largely uncorrelated with traditional asset classes. Our systematic investment process enables us to seamlessly integrate both ESG and financial metrics, with the goal of generating long-term value - an approach we believe is both original and compelling.

While index rebalancing and index-related relative value strategies are usually implemented by multi-strategy funds or proprietary trading houses, we have packaged them through a UCITS fund format with daily liquidity.

Our market neutral strategies come with distinct expected volatility levels to accommodate various investor needs.

Equity long/short strategies can help stabilise portfolio performance when combined with other asset classes such as equities and bonds. Indeed, their historical low correlation with most traditional asset classes, including in downside movements, has a smoothing effect on the portfolio’s fluctuations. They can also help reduce portfolio risk.

Do you want to know more about our market neutral strategies?

Find out more about our publications?

Main risks associated with the strategies

- Risk of loss of capital

- Equity risk

- Derivative risk

- Counterparty Risk

- Arbitrage risk

- Sustainability risk